|

|

|

|

|||||

|

|

|

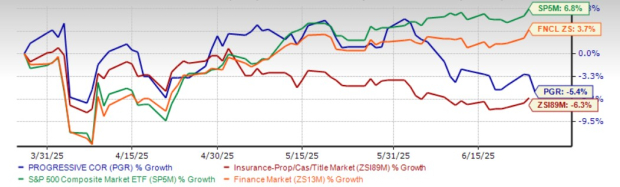

Shares of The Progressive Corporation PGR have lost 5.4% in the past three months, outperforming the industry’s decline of 6.3%. However, the stock has underperformed the Finance sector’s increase of 3.7% and the Zacks S&P 500 composite’s increase of 6.8% in the said time frame.

PGR is now trending below its 50-day simple moving average (SMA), indicating the possibility of a downside ahead.

PGR is one of the country’s largest auto insurance groups, the largest seller of motorcycle and boat policies, the market leader in commercial auto insurance and one of the top 15 homeowners carriers based on premiums written.

Shares of Allstate Corporation ALL and Travelers Companies TRV, two other auto insurers, have lost 8.3% and 0.4%, respectively, in the said time frame.

Travelers holds a leading position in the U.S. auto, homeowners, and commercial property-casualty insurance markets. Its solid market standing and well-executed growth strategies are set to support ongoing expansion across both personal and commercial segments. The company is well-positioned for long-term growth, driven by high customer retention, strategic pricing improvements, rising new business volumes, and positive momentum in renewal premiums.

Allstate is refining its strategy by focusing on its core strengths and exiting underperforming segments. The company projects growth in total Property-Liability policies in force this year, supported by higher auto insurance renewal rates and steady increases in new business. Backed by rising premium income, a growing protection services division, and continued operational streamlining, Allstate is well-positioned to achieve sustained long-term growth.

PGR is currently expensive. It is trading at a P/B multiple of 5.26, higher than the industry average of 1.57.

Shares of Allstate and Travelers are also trading at a premium to the industry.

Progressive is strategically positioned for sustained growth, supported by initiatives such as promoting bundled auto insurance, reducing exposure to high-risk properties, and enhancing segmentation through innovative product launches. Its robust product suite and disciplined underwriting have driven a strong volume of policies in force, while high retention rates continue to support premium growth. Policy Life Expectancy (PLE) — a critical measure of customer retention — has shown consistent improvement across all business lines, with innovative offerings and competitive pricing expected to drive further gains.

Aligning with broader industry trends, Progressive has embraced digital transformation, notably through the integration of artificial intelligence. The company has maintained an average combined ratio below 93% over the past decade — much better than the industry average of over 100% — reflecting effective underwriting and favorable reserve development that continue to fuel performance.

A well-structured reinsurance program provides substantial protection against catastrophic events and severe weather, reinforcing the company’s financial stability. Strong cash flow generation supports ongoing investment in growth-focused initiatives, especially digital technologies that enhance efficiency and margin expansion. Meanwhile, Progressive has consistently increased its book value and made strides in lowering its leverage.

While leverage remains slightly above the industry norm, Progressive’s superior times interest earned ratio highlights its solid financial health and operational strength.

Seven analysts have raised earnings estimates for 2025 and four have raised the same for 2026 in the past seven days. The Zacks Consensus Estimate for 2025 and 2026 earnings has moved 1.1% and 0.4% north, respectively, in the same time frame.

The Zacks Consensus Estimate for Progressive’s 2025 earnings per share indicates an increase of 17.6% on 16.7% higher revenues. The consensus estimate for 2026 earnings per share indicates a 2.4% decline but a 10.5% increase in revenues. The long-term earnings growth rate is pegged at 9.8%, better than the industry average of 6.8%. PGR has a Growth Score of A.

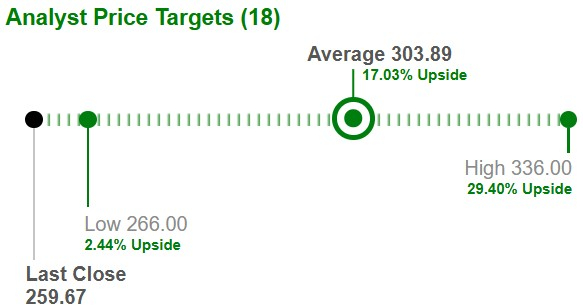

Based on short-term price targets offered by 18 analysts, the Zacks average price target is $303.89 per share. The average suggests a potential 17% upside from the last closing price.

Return on equity for the trailing 12 months was 33.5%, comparing favorably with the industry’s 7.8%. This reflects its efficiency in utilizing shareholders’ funds.

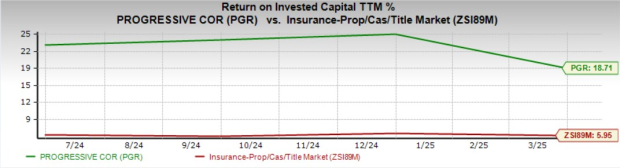

Also, return on invested capital (ROIC) has been increasing over the last few quarters as the company raised its capital investment over the same time frame. This reflects PGR’s efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 18.7%, better than the industry average of 6%.

Progressive boasts a robust market presence, a diverse range of products and services, and strong underwriting and operational capabilities. Favorable analyst sentiment, a consistent dividend history and a VGM Score of A further strengthen investor confidence in PGR.

However, rising repair costs weigh on auto insurance margins. Given its premium valuation, it is better to adopt a wait-and-see approach for this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite