|

|

|

|

|||||

|

|

|

Super Micro Computer’s SMCI top line is rapidly expanding on the back of its innovative product portfolio. Its direct liquid cooling (DLC) and server offerings have been experiencing robust traction from hyperscalers, high-performance computing and artificial intelligence (AI) customers. Nonetheless, SMCI’s gross margin has been moving inconsistently for the past several quarters, with a declining trend.

In the third quarter of fiscal 2025, Super Micro’s non-GAAP gross margin contracted 590 basis points year over year and 220 basis points sequentially to 9.7%. SMCI had to bear the growing costs associated with its latest products that are facing high traction. Furthermore, SMCI’s margins are facing pressure from high inventory reserves for older-generation products.

In the previous quarters, SMCI attributed unfavourable product and customer mix to its margin contraction. As Super Micro Computer continues to focus on winning new clients with competitive pricing and increasing its DLC AI GPU cluster capability, the costs have shot up, resulting in margin contraction.

Higher upfront costs associated with ramping up production for its DLC technology are weighing on Super Micro Computer’s gross margin. While this challenge might seem unfavorable in the near term, once SMCI scales up, it might prove to give the company an edge in the AI datacenter market.

Super Micro Computer is also ramping up its production capacity in Malaysia and Taiwan, which will further lower the manufacturing costs of its products due to economies of scale in the long term. SMCI is also expanding its production capacity in California, hence supporting the current U.S. government’s efforts to bring manufacturing to the United States. These factors will have a long-term positive impact on the company’s gross margin.

The server and liquid cooling space comprises large players, including Hewlett Packard Enterprise HPE and Dell Technologies DELL. In its first-quarter fiscal 2026, Dell tagged the AI server business as lumpy and non-linear. It stated that product deployments in this space are large, complex, and schedule-bound.

The AI server space faces irregularities as big contracts might land in one quarter but ship in another, depending on external factors. However, this has not deterred Dell from accumulating $14.4 billion in AI backlogs.

Hewlett Packard Enterprise offers a range of servers, including HPE ProLiant, HPE Synergy, HPE BladeSystem and HPE Moonshot servers. In the second quarter of fiscal 2025, Hewlett Packard Enterprise’s server segment sales grew 6% year over year due to strong demand for its AI servers.

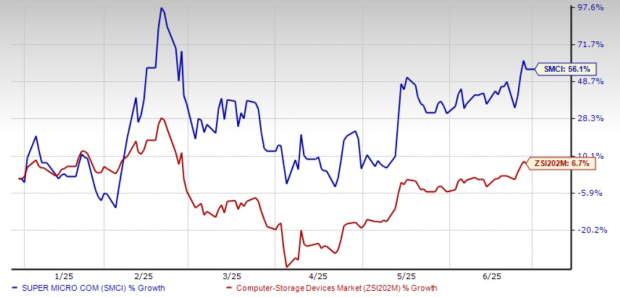

Shares of SMCI have gained 56.1% year to date compared with the Zacks Computer- Storage Devices industry’s growth of 6.7%.

From a valuation standpoint, SMCI trades at a forward price-to-sales ratio of 0.96X, lower than the industry’s average of 1.76X.

The Zacks Consensus Estimate for SMCI’s fiscal 2025 earnings implies a year-over-year decline of 6.33%, while the same for fiscal 2026 indicates growth of 27.54%. The estimates for fiscal 2025 and 2026 have been revised downward in the past 60 days.

SMCI currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 |

A Memory-Chip Shortage Is Squeezing Consumer Techand Its Set to Get Worse

DELL -9.13%

The Wall Street Journal

|

| Feb-12 | |

| Feb-12 |

Top Trump antitrust official leaves post following disputes over big mergers

HPE -6.76%

Associated Press Finance

|

| Feb-12 |

Cisco Memory Chip Warning Sends Down Dell, HPE, Arista, NetApp Shares

DELL -9.13% HPE -6.76%

Investor's Business Daily

|

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite