|

|

|

|

|||||

|

|

|

UnitedHealth Group Incorporated UNH was recently dropped from several Russell growth-style indices including the Russell Top 200 Growth, Russell 1000 Growth, and Russell 3000 Growth, effective June 30, 2025, according to Simply Wall St. The decision reflects both a sharp decline in UNH’s stock price and a shift away from traditional growth metrics.

Earlier, Mizuho had warned that UnitedHealth’s surging volatility and deep market value erosion might even jeopardize its place in the Dow Jones Industrial Average, although that removal has not occurred.

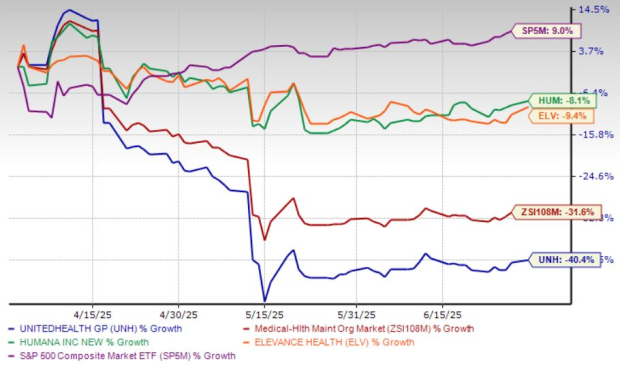

Shares of UnitedHealth plunged 40.4% in the past three months due to simultaneous pressures across multiple business lines. At one point in time, it had even lost more than $300 billion in market cap. This drop far outpaced the broader industry decline of 31.6%, while the S&P 500 has gained 9% during the same period.

Among its peers, Humana Inc. HUM fell only 8.1%, and Elevance Health, Inc. ELV lost 9.4%, highlighting the uniquely steep deterioration in UNH’s stock.

The company’s recent financial performance has also disappointed. UnitedHealth missed both earnings and revenue expectations in the first quarter and withdrew its full-year 2025 financial guidance. Rising medical costs, especially in the Medicare Advantage segment, are compressing margins, while a surge in high-acuity patient volumes is adding to cost pressures. Both Humana and Elevance Health have also faced cost pressures, but to a lesser extent and under more effective control.

UNH’s operational headwinds have been compounded by leadership uncertainty. CEO Andrew Witty stepped down unexpectedly, and the former longtime executive Stephen Hemsley returned to the helm. Soon after, the Wall Street Journal reported that the company was under criminal investigation for alleged Medicare fraud. Adding to this were expanded Medicare Advantage audits by the Centers for Medicare and Medicaid Services, increasing the likelihood of penalties and reimbursement clawbacks.

Further reputational damage came from allegations that UnitedHealth secretly incentivized nursing homes to avoid hospital transfers. Although the Department of Justice ultimately declined to pursue charges due to insufficient evidence, the incident nonetheless harmed the company’s public image.

The recent shift in investor perception from viewing UnitedHealth as a growth stock carries significant implications. The stock may now experience temporary selling pressure as index-tracking growth funds are forced to exit their positions. However, it could begin to gain more weight in value-focused funds, potentially helping to offset some of the capital outflows from growth-oriented strategies.

At the same time, the company’s business model faces real threats from regulatory risks. Optum Rx, UnitedHealth’s pharmacy benefit manager (PBM), may face mounting headwinds from ongoing regulatory scrutiny targeting the pricing power of PBMs. President Trump’s “most-favored nation” executive order could further challenge the role of middlemen like PBMs by encouraging more direct drug pricing for consumers. This remains an evolving regulatory situation.

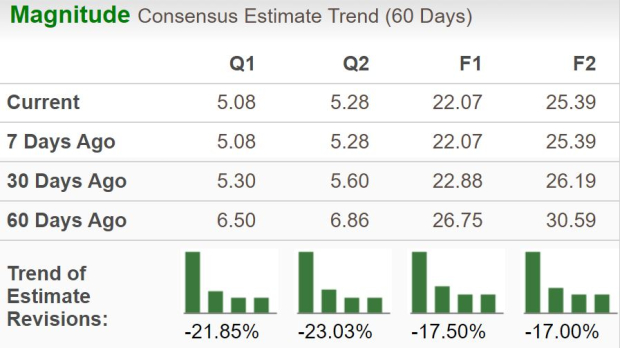

The Zacks Consensus Estimate for UNH’s 2025 EPS has seen 13 downward revisions in the past 60 days, while the 2026 EPS estimate has seen 11, without a single upward revision. Earnings for 2025 are now projected to decline by 20.2%, even as revenues are still expected to climb 12.3% year over year. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

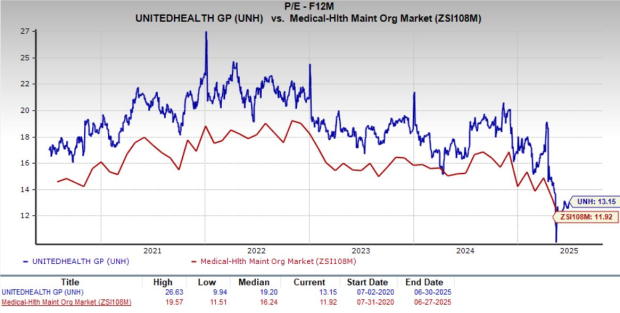

At first glance, UnitedHealth might seem attractively priced, trading at a forward P/E of 13.15X, well below its five-year median of 19.20X. However, that multiple still stands above the industry average of 11.92X. In comparison, Humana trades at 16.10X and Elevance at 10.58X, placing UnitedHealth somewhere in the middle of the pack despite its recent selloff.

Still, not all hope is lost. UnitedHealth continues to invest heavily in technology and analytics, particularly in value-based care and predictive health models. These initiatives could eventually help stabilize and rebuild earnings power. Despite the recent turmoil and loss of growth-stock status, the company’s vertically integrated structure, scale, and expanding digital capabilities provide strategic advantages. Upcoming Medicare Advantage rate increases, scheduled for 2026, may also offer some margin relief and support future growth.

As of March 31, 2025, UnitedHealthcare served 50.1 million members, up 1.9% year over year, driven largely by growth in self-funded commercial plans. Long-term demographic trends, including an aging population and rising rates of chronic disease, remain favorable for UnitedHealth’s business model.

Financially, the company remains well capitalized. It generated $5.5 billion in operating cash flow in the first quarter, a sharp increase from $1.1 billion in the prior-year period. It also ended the quarter with $34.3 billion in cash and short-term investments. The company recently raised $3 billion through the issuance of various notes, in part to strengthen its balance sheet amid ongoing legal settlements.

UnitedHealth returned more than $5 billion to shareholders in the first quarter through dividends and stock repurchases. In addition to fortifying its liquidity, the company recently raised its quarterly dividend by 5.2% to $2.21 per share from $2.10, bringing its dividend yield to 1.76%, well above the industry average of 1.31%. While the near-term outlook remains clouded by regulatory and operational challenges, UnitedHealth’s core strengths and strategic pivots could position it for recovery in the longer term.

Given the breadth and severity of UnitedHealth’s current headwinds, including its removal from key growth indices, sharp underperformance relative to peers, margin pressures, regulatory investigations, and negative estimate revisions, investors should strongly consider exiting their positions.

The stock's recent collapse may not be just a temporary dislocation but reflects fundamental deterioration in growth visibility and investor confidence. In the short run, this is a stock to dump, not weather through. It currently has a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-29 | |

| Mar-26 | |

| Mar-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite