|

|

|

|

|||||

|

|

|

Disney DIS generates a substantial portion of its revenues from the Entertainment segment (45.2% in second-quarter fiscal 2025), which includes Linear Networks (22.7% of Entertainment revenues), Direct-to-Consumer (57.3%), and Content sales/Licensing and other (20%) businesses.

Direct-to-Consumer (“DTC”) business, which offers Disney+ and Hulu, has been prolific in driving Disney’s prospects, thanks to a strong content portfolio. At the end of the fiscal second quarter, Disney+ had 126 million subscribers, while Hulu reported 54.7 million viewers.

Disney has been unrelenting in its efforts to expand its content portfolio globally. Its exciting pipeline includes Miley Cyrus: Something Beautiful, Lilo & Stitch, Pixar’s Elio, Marvel’s The Fantastic Four: First Steps, Freakier Friday, Zootopia 2 and others.

Disney’s strategy to scale the DTC business by offering Disney+ and Hulu drives user experience. Its initiatives to improve the user interface through enhanced personalisation and customization features are noteworthy. The company’s plan to increase investments in local content outside the United States is another major growth driver.

Disney is set to launch “ESPN,” expanding its DTC service. The new platform will streamline access to every live event and studio show across ESPN’s network and ESPN+ content. It will also provide an opportunity to bundle the service with Disney+ and Hulu’s streaming services, thereby creating a major new revenue stream.

Disney wrestles with Netflix NFLX and Comcast CMCSA in the streaming space.

Netflix is benefiting from a growing subscriber base, fueled by a robust portfolio of localized and foreign-language content, and healthy engagement, with about two hours of viewing per member per day, indicating strong member retention. NFLX's advertising tier now accounts for more than 55% of new sign-ups in available markets. The 2025 content slate, with returning hit shows like Squid Game, Wednesday and Stranger Things, holds promise.

Comcast’s streaming business, led by Peacock, is benefiting from a content strategy that centers around a wide mix of programming. This includes NBCUniversal originals, next-day NBC and Bravo shows, Pay-One movies like Wicked, and a strong lineup of live sports — all aimed at appealing to a broad audience and driving consistent streaming engagement across different user groups.

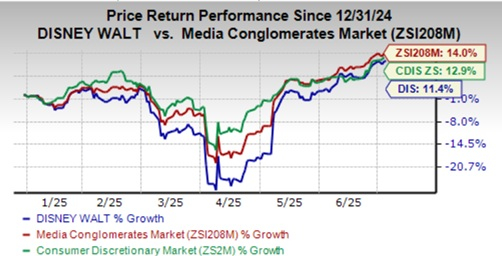

DIS shares have appreciated 11.4% in the year-to-date period, underperforming both the Zacks Consumer Discretionary sector’s return of 12.9% and the Zacks Media Conglomerates industry’s appreciation of 14.0%.

From a valuation standpoint, DIS stock is currently trading at a trailing 12-month Price/Earnings ratio of 21.60X compared with the industry’s 24.40X. DIS has a Value Score of B.

The Zacks Consensus Estimate for Disney’s 2025 earnings is pegged at $5.78 per share, up by a couple of cents over the past 7 days. This indicates a 16.3% increase from the figure reported in the year-ago quarter.

The Walt Disney Company price-consensus-chart | The Walt Disney Company Quote

DIS currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 32 min | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours |

Netflix Gives Paramount One Last Chance In Warner Bros. Bidding War. All Three Stocks Climb.

NFLX

Investor's Business Daily

|

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 9 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite