|

|

|

|

|||||

|

|

|

OneMain Holdings, Inc. OMF shares touched a 52-week high of $60.08 in last day’s trading session. Over the past three months, the stock has gained 47.8%, outperforming the industry’s rise of 38.9% and the S&P 500 Index’s 26% growth.

Moreover, the stock has performed better than its peers, Ally Financial ALLY and Navient Corporation NAVI. The ALLY stock has moved up 34.8%, whereas shares of Navient have rallied 37.7% in the same time frame.

Does the OMF stock have more upside left despite touching its 52-week high? Let us find out.

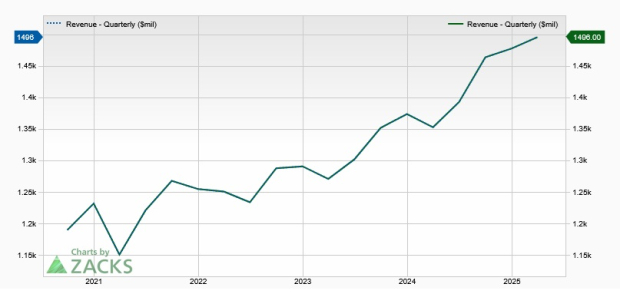

Diversified Product Base & Revenue Strength: Driven by growth in net interest income (NII), OneMain Holdings’ revenues have witnessed a five-year (2019-2024) compound annual growth rate (CAGR) of 3.6%, with the upward momentum continuing in the first quarter of 2025. Supported by its loan mix of Front Book and Back Book, the company aims for revenue sustainability while maintaining upside potential in a rapidly changing macroeconomic environment.

In order to increase its margins, OMF aims to reduce Back Book over time. The company’s auto finance capabilities have strengthened with the acquisition of Foursight. Thus, OMF is expected to witness continued growth in the top line, given its efforts to grow credit cards and auto finance businesses, along with its diversified product base.

Decent Balance Sheet Position: As of March 31, 2025, OneMain Holdings had total debt (comprising long-term debt and other liabilities) of $22.2 billion, and cash and cash equivalents of $1.4 billion. The company has multiple revolving secured lines of credit facilities and credit card revolving VFN facilities. Thus, despite a high debt burden, OMF will be able to address its near-term debt obligations even if the economic scenario worsens.

Given its relationship-driven business model and a decent balance sheet and capital position, the company has been able to boost investor confidence with efficient capital deployment activities. In 2019, OMF announced a dividend for the first time. Since then, it has hiked its dividend seven times, with the latest hike of 4% announced in April 2024.

In 2022, the company authorized a share repurchase program worth $1 billion, for which the expiry has been extended to Dec. 31, 2026. As of March 31, 2025, the company had $609.8 million worth of shares remaining under the authorization.

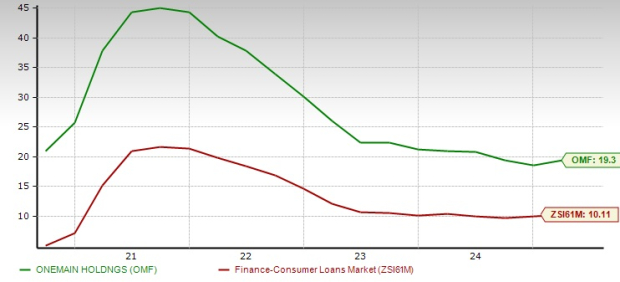

Attractive Return on Equity (ROE): OneMain Holdings’ profitability metrics compare favorably to those of its peers. The company’s trailing 12-month return on equity stands at 19.30%, outpacing the industry average of 10.11%.

In comparison, Ally Financial has an ROE of 9.53%, while Navient’s ROE stands at 5.20%. The higher ROE is a testament to OMF’s ability to deploy capital efficiently and underscores its long-term value creation potential for investors.

Rising Expense Base: OneMain Holdings has been witnessing a continuous increase in expenses. Total other expenses witnessed a CAGR of 3% over the last five years (2019-2024), with the uptrend persisting during the first three months of 2025. The increase has been mainly due to a rise in salaries and benefits and other operating expenses.

Overall expenses are likely to remain elevated in the near term owing to the company’s continued efforts to invest in new products and capabilities to enhance customer experience and strengthen its competitive positioning.

Weak Asset Quality: OneMain Holdings’ provision for finance receivable losses witnessed a CAGR of 9.1% over the five years ended 2024, outpacing the net finance receivable CAGR of 5.4% over the same period. This indicates underwriting concerns for the company.

Also, the company’s allowance ratio has consistently increased over the past five years, except in 2021 and 2024. Provisions rose in the first quarter of 2025 on a year-over-year basis. Given the rise in loan balances amid a challenging macroeconomic environment, provisions and allowance ratios are expected to remain elevated in the near term, hurting growth.

OneMain Holdings is well-positioned for top-line expansion, supported by a diverse product base, its efforts to grow credit card and auto finance businesses, along with decent loan demand. A higher ROE compared with the industry signifies that the company utilizes cash more efficiently than its peers.

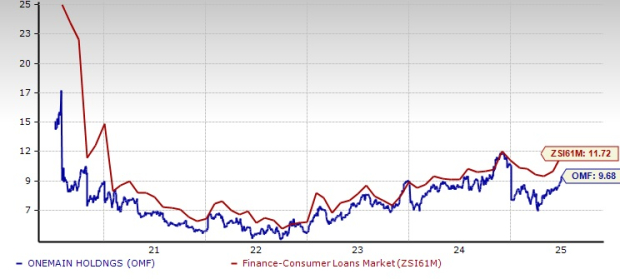

In terms of its valuation, the OMF stock appears inexpensive compared with the industry. It has a P/E (F1) ratio of 9.68, which is below the industry’s 11.72.

However, increasing expenses because of the company’s investments in new products and capabilities will likely hurt the bottom line to an extent. Also, poor asset quality may hamper growth.

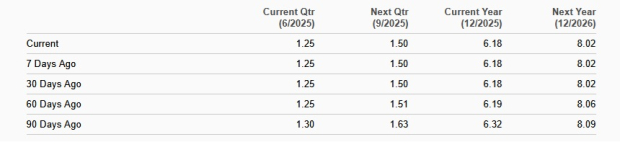

Analysts also do not seem very optimistic regarding the company’s earnings growth potential. Over the past 60 days, the Zacks Consensus Estimate for OMF’s 2025 and 2026 earnings has been revised lower.

Thus, while the OMF stock is trading at a discount, investors should not rush to buy the stock now, given its not-so-impressive earnings outlook and expense concerns. Those who already own the stock in their portfolios can hold on to it because it is less likely to disappoint over the long term.

Currently, OneMain Holdings carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-13 | |

| Jul-08 | |

| Jul-02 | |

| Jun-18 | |

| May-21 | |

| May-20 | |

| May-19 | |

| May-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite