|

|

|

|

|||||

|

|

|

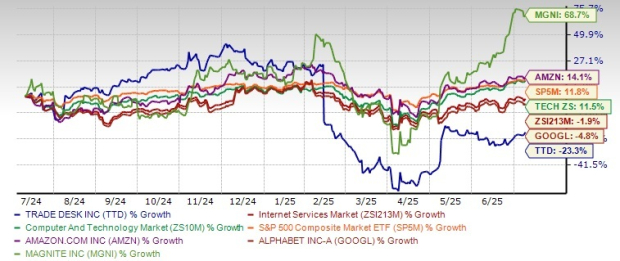

The Trade Desk TTD, a well-known name in the programmatic advertising space, has seen its stock take a significant hit. The stock price has declined 23.3% over the past year, underperforming the Zacks Internet Services industry’s decline of 1.9%. Investors are now wondering whether this is a temporary glitch or a sign of deeper cracks in the company’s business model.

Earlier in the year, tariff troubles led to a massive sell-off across indices. However, broader indices have recovered despite macroeconomic volatility. For context, the broader Computer & Technology sector and the S&P 500 Composite have gained 11.5% and 11.8% over the same time frame, respectively. TTD’s sharp decline appears to be driven more by company-specific challenges than broader market trends.

TTD is trading nearly 47% below its 52-week high, which puts the stock in a highly distressed territory. With macroeconomic uncertainty and intense industry competition, spooked investors are left wondering: Does TTD still deserve a spot in the portfolio?

Let’s unpack the issues behind the recent price slump and evaluate whether holding onto the stock is a smart move.

Macroeconomic uncertainty is likely to weigh on advertising budgets. TTD highlighted the impact of the volatile macro backdrop, particularly on the large global brands. If macro headwinds worsen or persist into the second half of 2025, revenue growth may face further pressure due to reduced programmatic demand.

The Trade Desk price-consensus-eps-surprise-chart | The Trade Desk Quote

The intensely competitive nature of the digital advertising industry, dominated by industry giants like Alphabet GOOGL and Amazon AMZN, as well as other smaller players like Magnite MGNI, continues to put pressure on TTD’s market positioning.

Walled gardens like Google and Amazon dominate this space as they control their inventory and first-party user data, allowing for highly targeted ad campaigns.

While CTV remains a strong revenue driver, this market is also increasingly becoming competitive. Heavy reliance on CTV for growth is a concern, as any adverse impact on this segment could weigh heavily on the overall performance.

Growing regulatory scrutiny around data privacy and evolving consumer data practices also threaten to disrupt the established audience-targeting methods.

Higher expenses are likely to weigh on profitability. In the last reported quarter, total operating costs surged 21.4% year over year to $561.6 million. Expenses soared on account of continued investments in boosting platform capabilities, particularly platform operations. Higher costs can prove a drag on margins, especially if revenue growth does not keep pace.

TTD derived 88% of its revenues from North America in the first quarter of 2025, while only 12% came from international markets. A weak international footprint limits TTD’s total addressable market expansion potential. Though TTD is focusing on geographic expansion, executing well across disparate markets can be complex and risky.

Given all these factors, analysts remain bearish on the stock, as evident from the downward estimate revision for the current year in the past 60 days.

The company has also underperformed its digital advertising peers, including Alphabet, Amazon and Magnite. Amazon shares have gained 14.1% while Magnite skyrocketed 68.7%. GOOGL is down 4.8%.

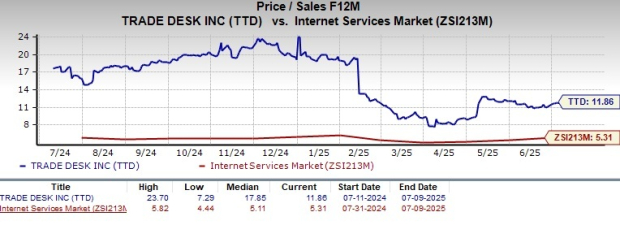

TTD stock is also not so cheap, as its Value Style Score of F suggests a stretched valuation at this moment. The stock is trading at a premium with a forward 12-month price/sales of 11.86X compared with the industry’s 5.31X.

The Trade Desk is grappling with several challenges, including macroeconomic volatility, escalating costs, and fierce competitive pressure. Its heavy reliance on CTV and the North American markets restricts its growth diversification. Additionally, the sharp decline in its stock price and a stretched valuation add to investor concerns.

With a Zacks Rank #4 (Sell), investors would be better off if they offloaded this stock from their portfolios.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 16 min | |

| 25 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

Globalstar Stock Jumps After Report Amazon Is In Talks To Acquire Satellite Firm

AMZN

Investor's Business Daily

|

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 6 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite