|

|

|

|

|||||

|

|

|

What a brutal six months it’s been for Nextdoor. The stock has dropped 26.9% and now trades at $1.74, rattling many shareholders. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Nextdoor, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even though the stock has become cheaper, we're cautious about Nextdoor. Here are three reasons why we avoid KIND and a stock we'd rather own.

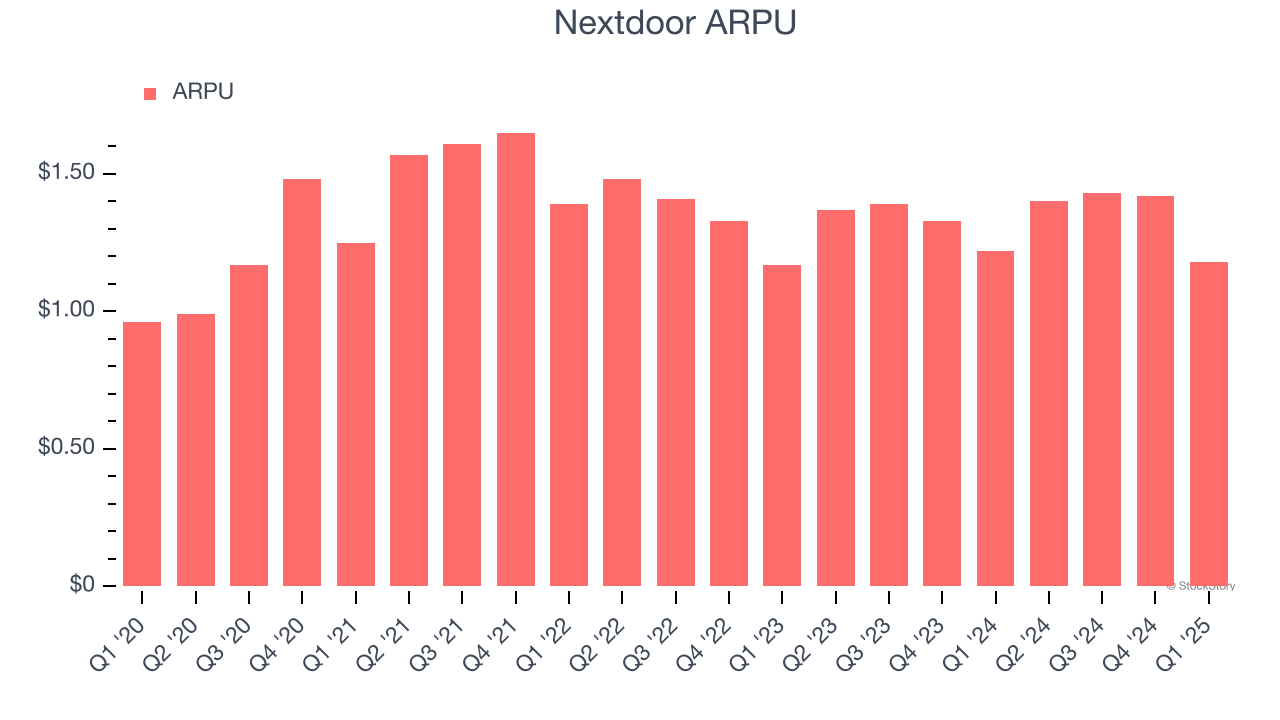

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Nextdoor’s audience and its ad-targeting capabilities.

Nextdoor’s ARPU has been roughly flat over the last two years. This isn’t great, but the increase in weekly active users is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Nextdoor tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

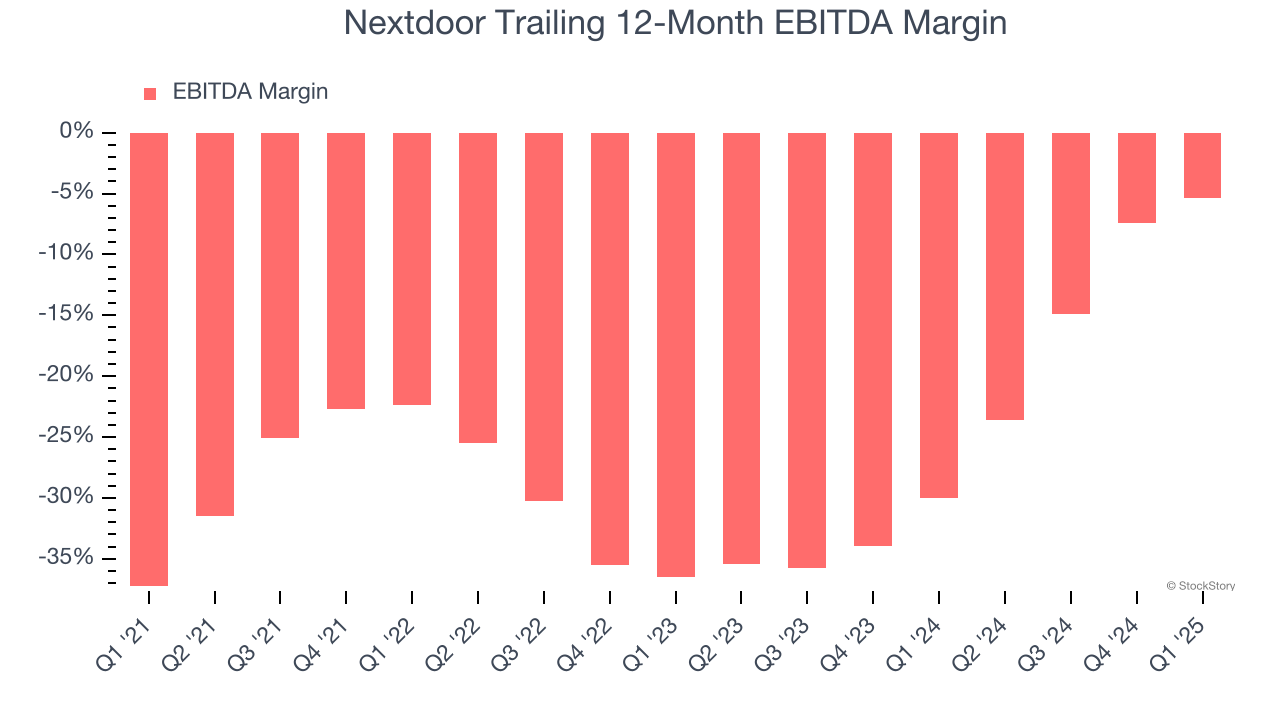

Operating income is often evaluated to assess a company’s underlying profitability. In a similar vein, EBITDA is used to analyze consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a clearer view of the business’s profit potential.

Nextdoor’s expensive cost structure has contributed to an average EBITDA margin of negative 17% over the last two years. Unprofitable consumer internet companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Nextdoor reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

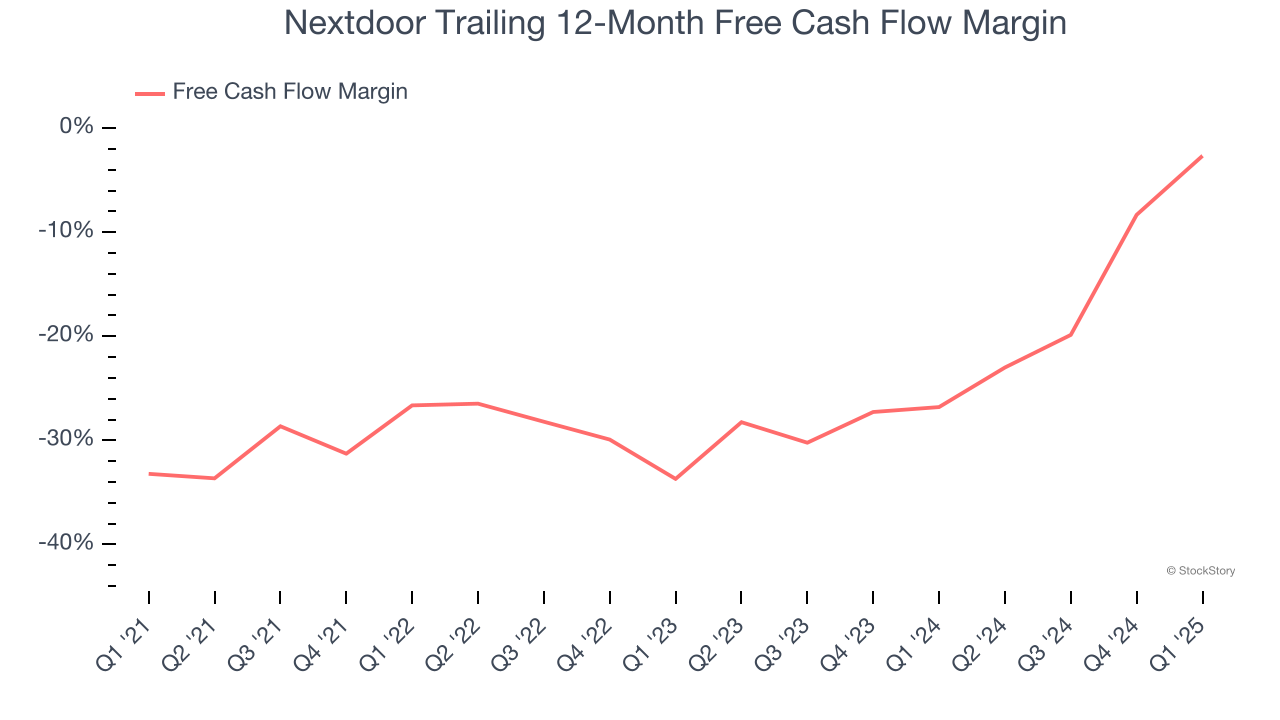

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Nextdoor’s free cash flow broke even this quarter, the broader story hasn’t been so clean. Nextdoor’s demanding reinvestments have drained its resources over the last two years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 14%, meaning it lit $14.05 of cash on fire for every $100 in revenue.

Nextdoor isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 3× forward price-to-gross profit (or $1.74 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-21 |

Why Nextdoor is having a founder-led re-founding moment

Yahoo Finance Video

|

| Jul-15 |

Why Nextdoor (KIND) Stock Is Up Today

StockStory

|

| Jul-15 |

MEET THE NEW NEXTDOOR

PR Newswire

|

| Jul-14 | |

| Jul-14 |

Nextdoor (KIND) Stock Trades Up, Here Is Why

StockStory

|

| Jul-14 | |

| Jul-11 |

Nextdoor Changing Stock Symbol Amid Product Redesign

Investopedia

|

| Jul-11 | |

| Jul-08 | |

| Jul-07 | |

| Jun-25 | |

| Jun-18 | |

| Jun-17 | |

| Jun-17 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite