|

|

|

|

|||||

|

|

|

Costco Wholesale Corporation COST sustained its steady comparable sales growth in June, reflecting its ongoing strength with value-conscious consumers. The company’s competitive pricing and quality merchandise — available both in-store and through its expanding e-commerce platform — continue to resonate with shoppers navigating inflationary pressures.

For the five weeks ended July 6, 2025, Costco reported a 5.8% year-over-year increase in total company comparable sales. Regionally, comparable sales rose 4.7% in the United States, 6.7% in Canada and 10.9% in Other International markets. This follows total comparable sales growth of 4.3% in May and 4.4% in April, signaling consistent momentum.

On an adjusted basis, excluding the impacts of gasoline price fluctuations and foreign exchange, comparable sales were even more robust. U.S. comps climbed 5.5%, while Canada and Other International markets posted increases of 7.9% and 8.2%, respectively. Overall, total company comps, excluding these factors, grew 6.2%, following strong rises of 6% in May and 6.7% in April.

E-commerce also remained a bright spot, with comparable sales surging 11.5% or 11.2% when adjusted for fuel and currency headwinds. This builds on gains of 11.6% in May and 12.6% in April, reflecting sustained strength in Costco’s online channel.

As a result, Costco's net sales for June increased 8% to $26.44 billion, up from $24.48 billion in the same period last year. This follows a sales improvement of 6.8% and 7% reported in May and April, respectively.

Costco’s resilient business model, centered around a membership-based structure, continues to be a major growth driver. The company’s high membership renewal rates, coupled with its efficient supply-chain management and bulk purchasing power, ensure competitive pricing and customer loyalty.

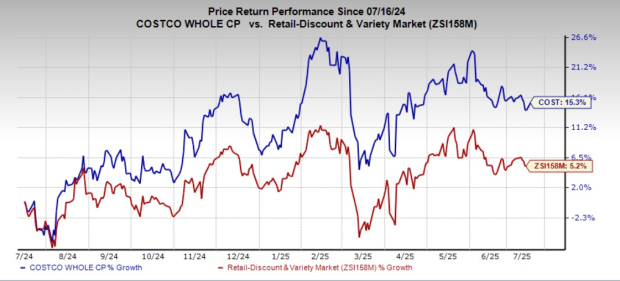

Shares of this Zacks Rank #3 (Hold) company have advanced 15.3% in the past year compared with the Retail – Discount Stores industry’s rise of 5.2%.

US Foods Holding Corp. USFD, one of America’s leading foodservice distributors, currently holds a Zacks Rank #2 (Buy). USFD has a trailing four-quarter earnings surprise of 1.5%, on average. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for US Foods Holding’s current financial-year sales and earnings implies growth of 5% and 21.3%, respectively, from the year-ago reported numbers.

BJ's Wholesale Club Holdings BJ, one of the leading operators of membership warehouse clubs, currently carries a Zacks Rank #2. BJ has a trailing four-quarter earnings surprise of 17.7%, on average.

The Zacks Consensus Estimate for BJ's Wholesale Club’s current financial-year sales and earnings calls for growth of 5.5% and 6.2%, respectively, from the year-ago reported numbers.

Grocery Outlet GO, an extreme value retailer of quality, name-brand consumables and fresh products, carries a Zacks Rank #2. GO has a trailing four-quarter earnings surprise of 25.7%, on average.

The Zacks Consensus Estimate for Grocery Outlet’s current financial-year sales suggests growth of around 7.9% from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite