|

|

|

|

|||||

|

|

|

Semtech has gotten torched over the last six months - since January 2025, its stock price has dropped 30% to $48.25 per share. This may have investors wondering how to approach the situation.

Is now the time to buy Semtech, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Despite the more favorable entry price, we're swiping left on Semtech for now. Here are three reasons why you should be careful with SMTC and a stock we'd rather own.

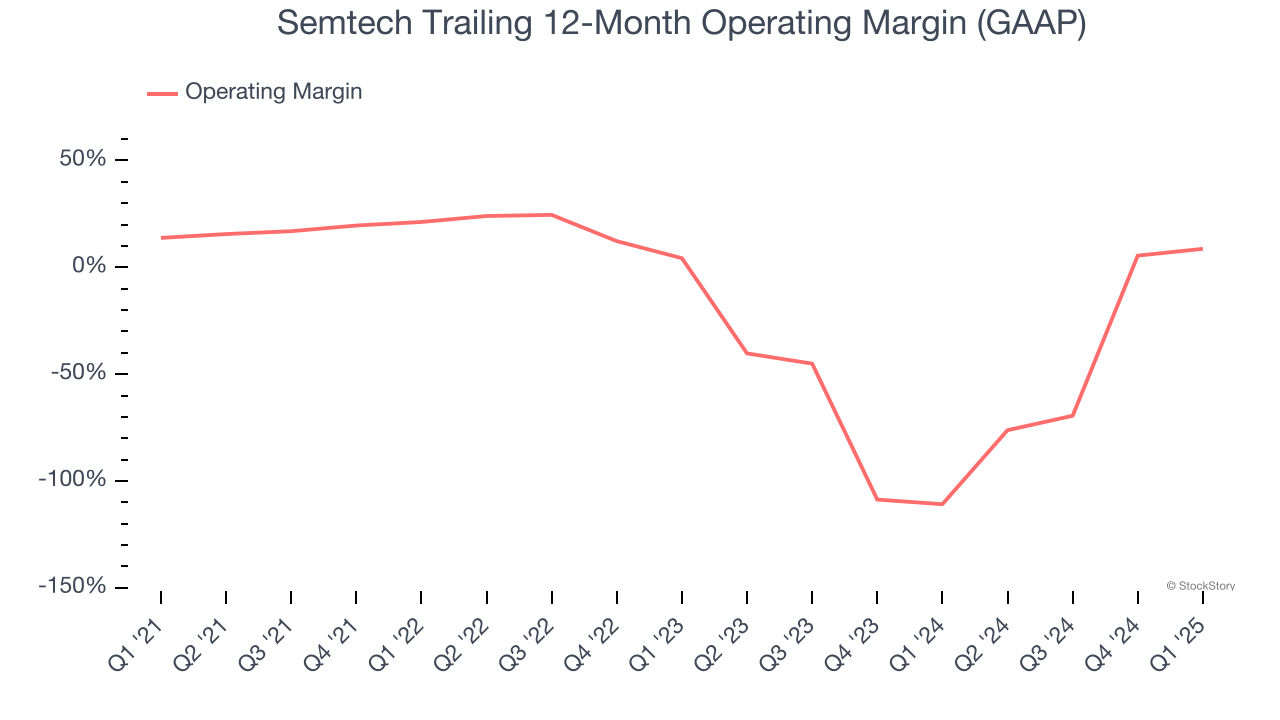

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Although Semtech was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 47.2% over the last two years. Unprofitable semiconductor companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

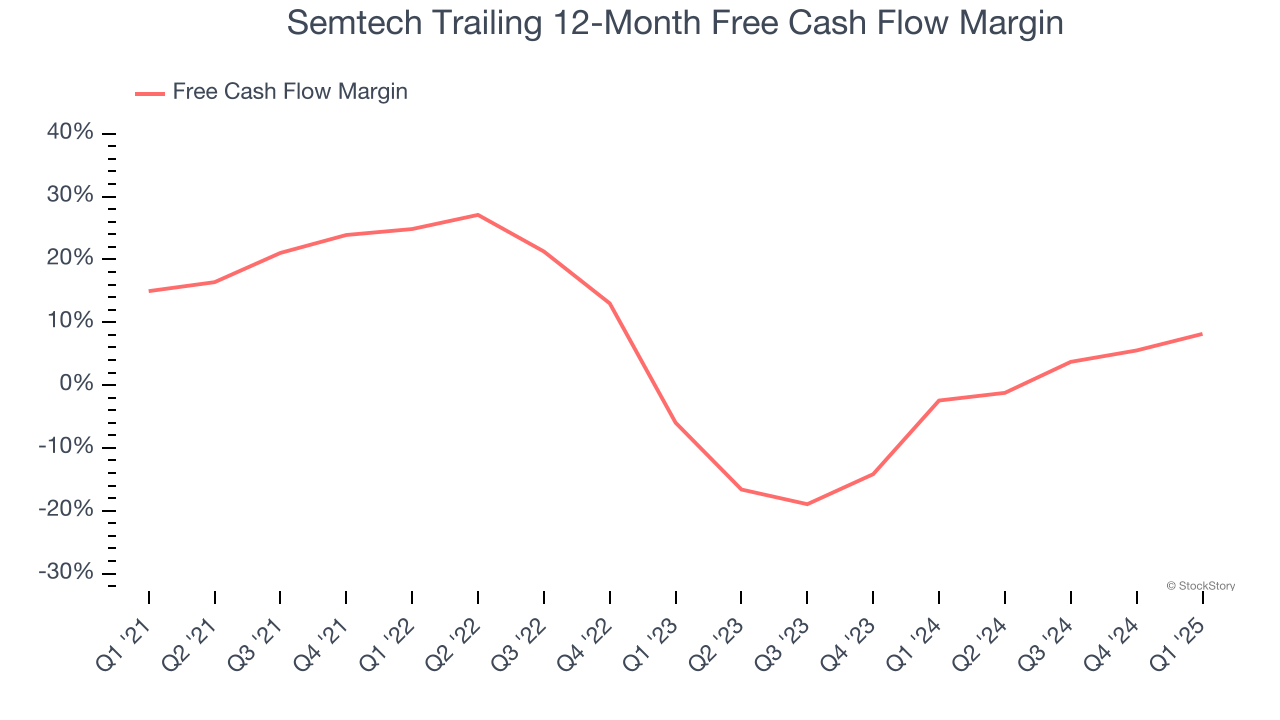

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Semtech’s margin dropped by 6.8 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because of its relatively low cash conversion. If the longer-term trend returns, it could signal it’s becoming a more capital-intensive business. Semtech’s free cash flow margin for the trailing 12 months was 8.1%.

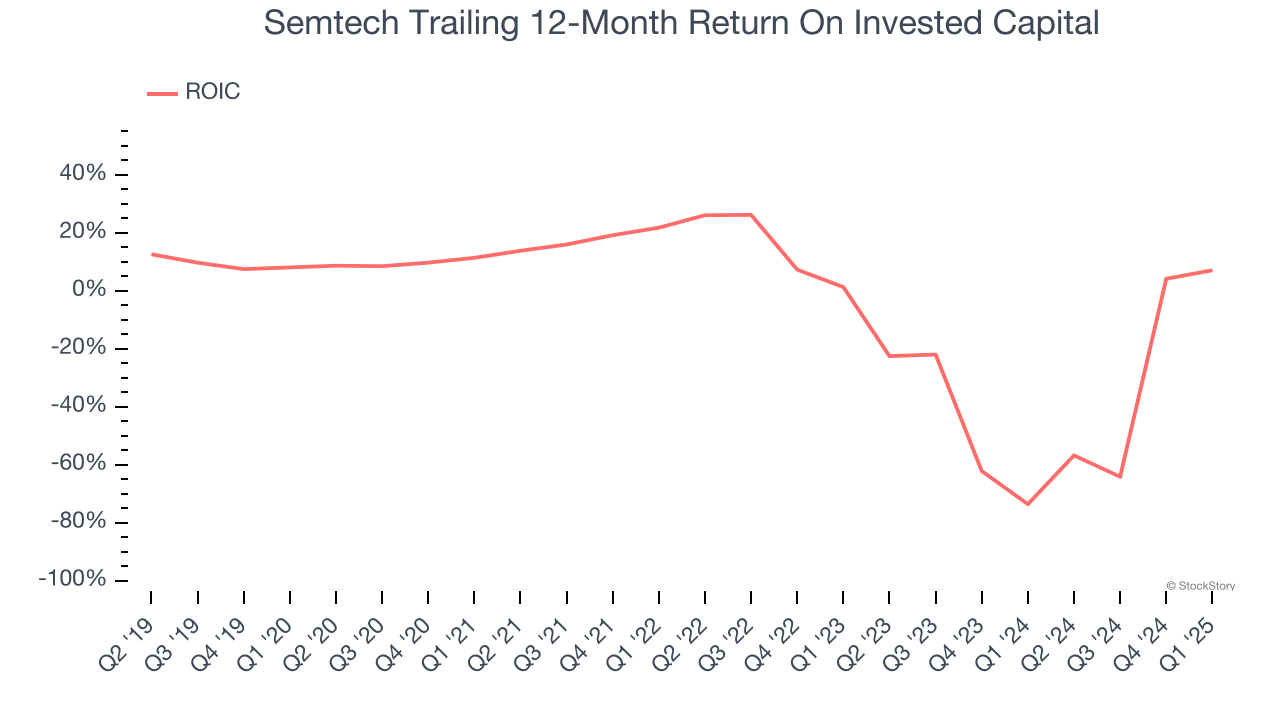

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Semtech’s five-year average ROIC was negative 6.4%, meaning management lost money while trying to expand the business. Its returns were among the worst in the semiconductor sector.

We cheer for all companies solving complex technology issues, but in the case of Semtech, we’ll be cheering from the sidelines. Following the recent decline, the stock trades at 27.7× forward P/E (or $48.25 per share). This valuation tells us a lot of optimism is priced in - you can find more timely opportunities elsewhere. Let us point you toward one of our all-time favorite software stocks.

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Mar-24 | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-16 | |

| Mar-16 | |

| Mar-16 | |

| Mar-16 | |

| Mar-16 | |

| Mar-12 | |

| Mar-12 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite