|

|

|

|

|||||

|

|

|

Toast, Inc.’s TOST shares have gained 21.6% year to date, outperforming the Internet Software market and the Zacks Computer & Technology sector’s growth of 14.6% and 8.4%, respectively. The S&P 500 composite has returned 5.6% over the same time frame. The company is one of the leading providers of software-as-a-service (SaaS) and hardware solutions focused on the restaurant market.

TOST was down 0.3% last day and closed the session at $44.34, close to its 52-week high of $46.57. While the recent momentum may seem encouraging, let us take a closer look at the company’s pros and cons to ascertain whether investors hold the stock or exit the investment.

Toast is expanding its presence in the core U.S. SMB restaurant market. Wins like Applebee’s and Topgolf reflect that its momentum is strong. TOST has only 10% penetration into its 1.4 million location TAM, thereby offering a substantial long-term expansion opportunity. Toast’s investments in AI-powered tools like Sous Chef and ToastIQ bode well.

Apart from this, the company is making progress in three new growth vectors: enterprise, international and food & beverage retail. It has set a target to cross 10,000 locations by the end of 2025 across these three new growth areas. To boost its international footprint, Toast has added loyalty, e-mail marketing and guest book to product offerings and consequently managed to double guest attach rate over the past year for the most recent locations that went live.

TOST registered more than 6,000 net locations in the first quarter of 2025. It ended with approximately 140,000 total customer locations globally at quarter-end, reflecting 25% year-over-year growth. Management expects to post record net adds in the current quarter and 2025 is now expected to top 2024’s full-year net additions.

Toast, Inc. price-consensus-eps-surprise-chart | Toast, Inc. Quote

Toast achieved an adjusted EBITDA margin of 32%, within its medium-term target of 30-35% well ahead of schedule. The company attributed the strong profitability to disciplined expense management. Excluding bad-debt charges and credit-related expenses, operating costs rose only around 12%, mainly due to increased spending on sales and marketing to hire representatives and amplify brand efforts. Research and development, and general and administrative expenses remained mostly flat.

Management emphasized that this disciplined approach is fueling healthy top-line growth while investing only in areas with high return on investment. Free cash flow turned positive. The figure was $69 million against a $33 million loss a year ago.

Driven by these developments, Toast now projects 26% growth in fintech and subscription gross profit for 2025 at the midpoint, while adjusted EBITDA is now estimated at $550 million, with a 31% margin, an increase of five percentage points from 2024.

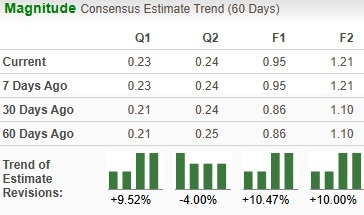

Given this, analysts have revised earnings estimates upwards for the current quarter and the current year.

Management highlighted that it was closely monitoring the macro environment and emphasized restaurants' ability to navigate macro challenges. Despite Toast’s confidence, the restaurant industry is still highly sensitive to consumer spending, labor inflation and supply-chain volatility. A consumer downturn or cost pressures could reduce restaurant spend on technology, thereby impacting TOST’s performance.

Decline in Gross Payment Volume (“GPV”) per location is another problem, as it implies lower average transaction volumes. TOST’s overall GPV surged 22% year over year to $42 billion in the first quarter. However, GPV per location declined 3% year over year. TOST added that it expects GPV per location to remain down in a similar range in the current quarter.

Higher costs and competitive pressure from various small and big players who are also vying for a larger share of this lucrative market are other headwinds. Subscription revenues were up 38%, driven by improved ARR to revenue conversion. The company expects subscription revenue growth to “return to more normalized levels” in the latter half of 2025.

TOST stock is also not so cheap, as its Value Style Score of F suggests a stretched valuation at this moment.

Toast is quite expensive, with the stock trading at a premium with a price/book multiple of 13.20X compared with the industry’s 6.57X.

Despite some headwinds, Toast’s focus on expanding addressable market and strategic investments in AI supports long-term upside. The company’s improving profitability, robust customer additions and raised outlook reflect operational strength.

TOST currently carries a Zacks Rank #3 (Hold). Long-term investors should continue holding their positions. However, new entrants may benefit from waiting for a more favorable entry point, as the current valuation indicates the optimism is already largely priced in.

Some better-ranked stocks within the Internet software space are Affirm Holdings, Inc. AFRM, Bumble Inc. BMBL and HubSpot, Inc. HUBS, each sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for AFRM’s fiscal 2026 EPS is pegged at 74 cents, improved by 4 cents in the past seven days. AFRM’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 102.2%. The stock has gained 104.9% in the past year.

The Zacks Consensus Estimate for BMBL’s 2025 earnings per share is pegged at $1.05, improved by 1 cent in the past seven days. Bumble’s earnings missed the Zacks Consensus Estimate in the last reported quarter by 18.8%. Its shares have lost 29.5% in the past year.

The Zacks Consensus Estimate for HUBS’ 2025 EPS is pegged at $9.34, unchanged in the past seven days. HubSpot’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 10.65%. The stock has risen 10.1% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-21 | |

| Feb-21 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite