|

|

|

|

|||||

|

|

|

Edwards Lifesciences EW is gaining from the robust uptake of its premium surgical technologies. The company’s Transcatheter Aortic Valve Replacement (“TAVR”) platform is positioned for continued global leadership and strong, sustainable growth. In Transcatheter Mitral and Tricuspid Therapies (“TMTT”), the company benefits from a strategic portfolio of leading transcatheter technologies to provide both repair and replacement solutions for mitral and tricuspid patients. Meanwhile, headwinds from macroeconomic challenges and currency fluctuations raise concerns for Edwards’ operations.

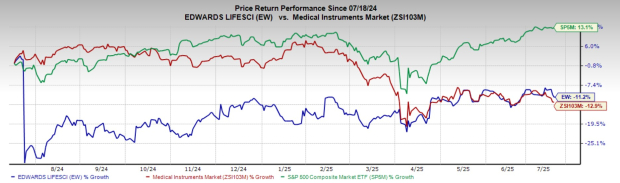

In the past year, this Zacks Rank #2 (Buy) stock has lost 11.2% compared with the 12.9% decline of the industry and the 13.1% growth of the S&P 500 composite.

The renowned global medical device company has a market capitalization of $44.66 billion. The company’s earnings yield of 3.2% favorably compares to the industry’s -3.6%. In the trailing four quarters, EW surpassed earnings estimates twice and matched on the other two occasions, the average surprise being 3.5%.

Let’s delve deeper.

Surgical Structural Heart, a Promising Business: The business pioneered the innovative RESILIA tissue, which is backed by more than 40 years of the company’s tissue technology leadership. In the first quarter of 2025, the segment grew 1% from the prior-year level, driven by the strong global adoption of Edwards’ premium surgical technologies, INSPIRIS, MITRIS and KONECT. The company continues to see positive procedure growth globally for the many patients treated surgically, including those undergoing complex procedures. Edwards has been continuously generating evidence to expand the RESILIA portfolio.

The company also made progress in advancing important innovations worldwide, including the launch of MITRIS in China, which received positive feedback from surgeons. As another major development, Edwards Lifesciences closed the acquisition of Endotronix in 2024, marking its entry into implantable heart failure management (IHFM).

TAVR Stands Strong: In the first quarter of 2025, TAVR sales exceeded $1 billion for the second consecutive quarter.In the United States, SAPIEN 3 Ultra RESILIA continued to demonstrate solid performance. Outside the United States, TAVR sales growth was supported by the continued launch of SAPIEN 3 Ultra RESILIA in Europe. Management anticipates TAVR growth momentum to continue as centers gradually adopt these new therapies and become part of extended processes. Alongside this, the next-generation SAPIEN X4 system is also in development.

In Japan, the company continues to focus on expanding the ability of this therapy, with AS being a significantly undertreated disease among the substantial elderly population in the country. Additionally, following the CE Mark for the Alterra system for congenital heart patients, Edwards Lifesciences is rolling out this therapy in Europe, and initial feedback from clinicians has been positive. The company anticipates FDA approval of the JenaValve Trilogy Heart Valve System in late 2025, which will represent the first approved therapy for patients suffering from AR.

TMTT Portfolio Holds Potential: In the first quarter, the TMTT segment witnessed a 58% increase in sales compared to the prior year, driven by the PASCAL system and the continued introduction of the EVOQUE system in the United States, Europe and globally. PASCAL’s growing adoption underscores its premium differentiation and the value it delivers to both physicians and patients. The adoption of differentiated PASCAL technology is expanding in both new and existing sites worldwide.

Management is pleased with the earlier-than-expected completion of enrollment for the CLASP IITR trial, studying TR patients with PASCAL randomized against optimal medical therapy alone. Meanwhile, Edwards Lifesciences is making strides with the EVOQUE commercial rollout, with successfully activated new sites in both the United States and Europe (other than initial trial centers). In April, the SAPIEN M3 mitral valve replacement system received CE Mark for the transcatheter treatment of patients with symptomatic mitral regurgitation who are unsuitable for surgery or transcatheter edge-to-edge therapy.

Macro Concerns Put Pressure on the Bottom Line: The global economy continues to experience volatility and disruptions, including conditions impacting inflation, credit and capital markets, interest rates, and factors influencing overall economic stability and the political environment relating to health care. The industry-wide increase in inflationary pressure, supply constraints stemming from geopolitical complications and regulatory changes are weighing heavily on the company’s operating results. Furthermore, Edwards anticipates pressure on its operating margin throughout 2025 due to the impact of current reciprocal tariff rates.

Foreign Exchange Headwinds: Foreign exchange is a major headwind for Edwards Lifesciences due to a considerable percentage of its revenues coming from outside the United States. We remain worried about the significant challenges Edward Lifesciences had to face owing to the unfavorable foreign currency impact that has been adversely affecting the company’s gross margin over the past few quarters. Foreign exchange rates decreased the first quarter’s reported sales growth by 170 basis points year over year.

The Zacks Consensus Estimate for Edwards’ 2025 earnings per share (EPS) has remained constant at $2.46 in the past 60 days.

The Zacks Consensus Estimate for the company’s 2025 revenues is pegged at $5.91 billion. This suggests a 1.1% fall from the year-ago reported number.

Some other top-ranked stocks in the broader medical space are Phibro Animal Health PAHC, Cardinal Health CAH and Cencora COR.

Phibro Animal Health has an estimated long-term earnings growth rate of 26% compared with the industry’s 13.9%. Its earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 30.6%. Its shares have rallied 60.5% compared with the industry’s 8.8% growth in the past year.

PAHC sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Cardinal Health, currently carrying a Zacks Rank #2, has an estimated long-term earnings growth rate of 10.9% compared with the industry’s 9.9% growth. Shares of the company have surged 67.7% against the industry’s 1.4% fall. CAH’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 10.3%.

Cencora, carrying a Zacks Rank #2 at present, has an earnings yield of 5.3% compared with the industry’s 3.7%. Shares of the company have rallied 30.8% against the industry’s 20% decline. COR’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 6%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite