|

|

|

|

|||||

|

|

|

Walmart Inc. WMT is refining its strategy to align with rapidly shifting consumer behaviors. In the first quarter fiscal 2026, Walmart U.S. delivered comp growth of 4.5% driven by transaction improvement of 1.6% and an average ticket increase of 2.8%, as well as strong e-commerce growth. Complementing this performance, Sam’s Club U.S. posted a robust 6.7% increase in comparable sales, excluding fuel. The growth was primarily volume-driven, with strength in Member’s Mark products.

A major driver of this traffic momentum is Walmart’s expansion of store-fulfilled delivery, now reaching 93% of U.S. households with delivery in under three hours. In the fiscal first quarter, one-third of Walmart’s deliveries were expedited, underscoring the increasing role of convenience in driving customer visits.

Membership remains another key growth lever. Walmart+ membership income rose at a double-digit rate. The company’s health and wellness category surged with high-teens growth, supported by strong prescription volume and over-the-counter product sales. To reinforce its price leadership, Walmart implemented more than 5,000 price reductions during the quarter.

Walmart’s strategy reflects a retail model that integrates stores, digital convenience and membership-driven engagement. By prioritizing faster fulfillment, competitive pricing and a broader customer reach, Walmart is positioning itself to drive steady same-store sales growth while adapting to evolving consumer demands in a highly competitive retail landscape.

Target Corporation TGT reported a 3.8% decline in comparable sales for the first quarter of fiscal 2025, driven by weaker discretionary demand. However, Target continues to prioritize same-day services, with Drive Up accounting for nearly half of digital sales in the quarter. Target expanded the Target Plus marketplace, growing GMV more than 20%, aiming to enhance assortment and offset comp pressures.

In contrast, Costco Wholesale Corporation COST reported 5.7% total company comparable sales growth in the third quarter of fiscal 2025, with U.S. comparable sales up 6.6%. Costco benefited from strong traffic and private label gains via Kirkland Signature. In addition, Costco is using local sourcing and strategic inventory management to maintain volume-driven comparable sales growth despite inflationary and tariff headwinds.

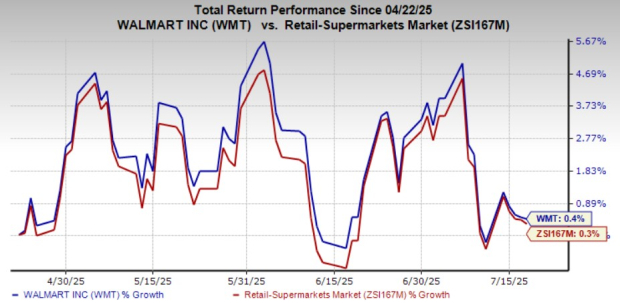

Shares of Walmart have gained around 0.4% in the past three months compared with the industry’s growth of 0.3%.

From a valuation standpoint, WMT trades at a forward price-to-earnings ratio of 34.74X, significantly up from the industry’s average of 31.99X.

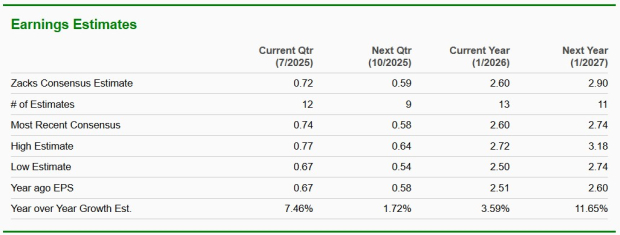

The Zacks Consensus Estimate for WMT’s fiscal 2026 earnings implies year-over-year growth of 3.6%, whereas the same for fiscal 2027 indicates a year-over-year uptick of 11.7%.

WMT currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite