|

|

|

|

|||||

|

|

|

lululemon athletica inc. LULU reported fourth-quarter fiscal 2024 results, wherein revenues and earnings beat the Zacks Consensus Estimate and improved year over year. The company’s top line improved year over year due to continued strength in the international business and improvement in the Americas.

lululemon’s fiscal fourth-quarter earnings per share (EPS) of $6.14 increased 16.1% compared with adjusted EPS of $5.29 in the prior-year quarter. The bottom line also surpassed the Zacks Consensus Estimate of $5.85.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

The company continues to advance its Power of Three X2 growth strategy. Since 2021, the plan’s base year, it has witnessed a 19% revenue CAGR, expanded adjusted operating margin by 170 basis points and grown the adjusted EPS at a 23% CAGR.

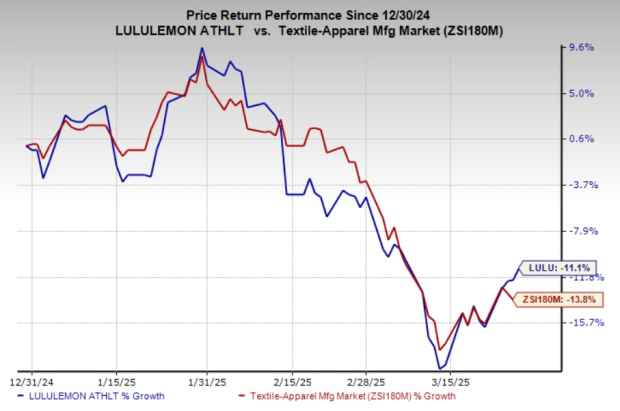

Shares of lululemon have dropped 10.1% in the after-hours trading session yesterday despite the strong fourth-quarter fiscal 2024 performance. The decline in share price is mainly due to the looming effects of the rising tariffs on imports from Mexico and China, and adverse currency rates. This Zacks Rank #3 (Hold) company has seen its shares decline 11.1% in the past three months compared with the Textile - Apparel industry’s fall of 13.8%.

The Vancouver, Canada-based company’s quarterly revenues advanced 13.6% year over year to $3.61 billion and outpaced the Zacks Consensus Estimate of $3.58 billion. On a constant-dollar basis, net revenues improved 14% year over year in the fiscal fourth quarter. Net revenues grew 7% in the Americas on a reported basis (8% on a constant-dollar basis) and 38% internationally (up 40% on a constant-dollar basis). Excluding revenues from the 53rd week of 2024, net revenues rose 8%.

Total comparable sales (comps) rose 3% year over year and 4% on a constant-dollar basis. Comps in the Americas were flat year over year. Internationally, comps increased 20% and rose 22% on a constant-dollar basis.

In the store channel, the company’s total sales increased 13% on a constant dollar basis, excluding the 53rd week, in the fiscal fourth quarter. Digital revenues improved 8% year over year and 4%, excluding the 53rd week. This contributed $1.8 billion, or 50%, to total revenues.

lululemon athletica inc. price-consensus-eps-surprise-chart | lululemon athletica inc. Quote

The gross profit improved 15% year over year to $2.2 billion. Also, the gross margin expanded 100 basis points (bps) to 60.4%, led by a 160-bps rise in the product margin, lower markdowns and improved shrink. This was partly offset by a 30-bps deleverage on fixed costs, 30-bps negative impacts of foreign exchange and higher air freight.

Management also noted that gross margin growth in the quarter was 30 bps ahead of its guidance. The upside was primarily driven by higher revenue leverage, disciplined fixed expense management within the gross margin and favorable-than-anticipated foreign exchange impacts. We expected the gross margin to expand 30 bps year over year to 59.7% for the fiscal fourth quarter.

SG&A expenses of $1.1 billion increased 15% from the year-ago quarter. SG&A expenses as a percentage of net revenues of 31.5% rose 60 bps from 30.9% in the prior-year quarter. The increase in SG&A expense rate was less than the leverage of 80-90 bps anticipated by the company due to the improved top line.

Our model predicted SG&A expenses to rise 14.6% year over year for the fiscal fourth quarter, with a 90-bps increase in the SG&A expense rate to 31.8%.

The operating income rose 14% year over year to $1 billion in the fiscal fourth quarter. The operating margin of 28.9% expanded 40 bps year over year. Our model predicted an 8.5% year-over-year increase in adjusted operating income. We estimated the operating margin to decline 70 bps year over year to 27.8%.

In fourth-quarter fiscal 2024, LULU opened 18 company-operated stores and completed 16 optimizations. This brought total store openings to 56 stores in fiscal 2024, including 14 company-operated stores from the acquisition of the Mexico operations. As of Feb. 2, 2025, the company operated 767 stores.

For fiscal 2025, LULU aims to expand its square footage by about 10% through store openings and its ongoing optimization efforts. The company plans to strengthen its presence in existing markets while entering new ones, including Italy as a company-operated market, and Denmark, Belgium, Turkey and the Czech Republic through a franchise model.

For fiscal 2025, the company anticipates 40-50 net new company-operated stores. It also expects to complete 40 co-located optimizations. LULU expects overall square footage growth of 10% for fiscal 2025. The store openings in fiscal 2025 will include 10-15 stores in the Americas. The rest of the store openings in fiscal 2025 are expected to occur in the international markets, primarily in China.

lululemon exited fiscal 2024 with cash and cash equivalents of $2 billion. The company had $393.9 million of capacity under its committed revolving credit facility and stockholders’ equity of $4.3 billion. Its inventories rose 9% year over year to $1.4 billion. Capital expenditure was $235 million in the fiscal fourth quarter.

In the fiscal fourth quarter, lululemon repurchased 0.9 million shares for $332.2 million at an average price of $354. In fiscal 2024, the company has repurchased 5.1 million shares for $1.6 billion. As of Feb. 2, 2025, it had $1.3 billion remaining under its current share repurchase authorization.

LULU is excited about building on its momentum in fiscal 2025 while staying adaptable in the face of macroeconomic uncertainties. With significant opportunities ahead, the company remains confident in its ability to drive sustainable growth and deliver long-term value for all stakeholders. However, the company anticipates higher costs and ongoing uncertainty due to the impacts of increased tariffs on imports from China and Mexico.

For the first quarter of fiscal 2025, management anticipates net revenues of $2.335-$2.355 billion, indicating 6-7% year-over-year growth. This also includes one percentage point negative impact of adverse currency rates. The company expects the gross margin to be flat year over year, as a modest improvement in the product margin is expected to be offset by deleverage on fixed costs. Markdowns are expected to be relatively flat with the prior-year quarter.

SG&A, as a percentage of sales, is expected to deleverage 120 bps year over year, driven by higher foundational investments and associated depreciation, as well as strategic initiatives to enhance brand awareness and support growth. The operating margin for the fiscal first quarter is expected to decline 120 bps year over year.

EPS for the fiscal first quarter is expected to be $2.53-$2.58, whereas it reported EPS of $2.54 in the prior-year quarter. EPS is expected to include a negative currency impact of 6 cents per share. LULU estimates an effective tax rate of 30% for the fiscal first quarter. The company expects dollar inventory to increase in the high-teens in the fiscal first quarter.

For fiscal 2025, LULU anticipates net revenues of $11.15-$11.3 billion, indicating 5-7% year-over-year growth. Excluding the 53rd week in 2024, revenues are expected to rise 7-8%. The company’s guidance assumes modestly positive revenue growth in the U.S. for fiscal 2025. Revenue guidance also includes an additional one percentage point negative impact from adverse currency rates.

lululemon expects a 60-bps year-over-year decline in the gross margin, driven by fixed cost deleverage, foreign exchange headwinds, and higher tariffs on imports from China and Mexico. Markdowns are expected to be relatively in line with fiscal 2024.

The SG&A expense rate is expected to rise 40-50 bps year over year for fiscal 2025, driven by ongoing investments into its Power of Three x2 plan and currency headwinds. Throughout fiscal 2025, the company plans to invest in marketing and brand building to enhance awareness and attract guests, support international growth and market expansion, and strengthen its technology and data analytics capabilities.

LULU expects the fiscal 2025 operating margin to contract 100 bps year over year. The company continues to be mindful of planning expenses while investing in its strategic roadmap to drive growth. The company noted that it is navigating headwinds from foreign exchange and tariffs, and absorbing additional costs compared with last year, including reinstating store labor hours, travel and incentive compensation.

The company projects an EPS of $14.95-$15.15, suggesting an increase from the $14.64 reported in fiscal 2024. It expects currency headwinds to hurt EPS by 30-35 cents per share. LULU anticipates an effective tax rate of 30% for fiscal 2025.

lululemon expects a capital expenditure of $740-$760 million for fiscal 2025. As part of the Power of Three X2 growth plan, LULU estimates net revenues of $12.5 billion by 2026, implying significant growth from the 2021 reported figure of $6.25 billion.

We have highlighted three better-ranked stocks from the same industry, namely Gildan Activewear GIL, Hanesbrands HBI and Ralph Lauren RL.

Gildan Activewear is a manufacturer and marketer of premium quality branded basic activewear for sale principally in the wholesale imprinted activewear segment of the North American apparel market. It carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Gildan Activewear’s current fiscal-year sales and earnings indicates growth of 4.4% and 16%, respectively, from the year-ago period’s reported figure. GIL has a trailing four-quarter average earnings surprise of 5.3%.

Hanesbrands engages in the design, manufacture, sourcing and sale of apparel essentials for men, women and children in the United States and internationally. It has a Zacks Rank #2 at present.

The Zacks Consensus Estimate for Hanesbrands’ current fiscal-year earnings indicates growth of 32.5% from the year-ago period’s reported figure. HBI has a trailing four-quarter average earnings surprise of 43.6%.

Ralph Lauren is a major designer, marketer and distributor of premium lifestyle products in North America, Europe, Asia, and internationally. The company currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Ralph Lauren’s current fiscal-year sales and EPS indicate growth of 5.8% and 16.5%, respectively, from the year-ago period’s reported figures. RL has a trailing four-quarter average earnings surprise of 6.5%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-01 | |

| Apr-01 | |

| Mar-30 | |

| Mar-27 | |

| Mar-26 | |

| Mar-24 | |

| Mar-24 | |

| Mar-24 | |

| Mar-23 | |

| Mar-20 | |

| Mar-19 | |

| Mar-18 | |

| Mar-18 | |

| Mar-18 | |

| Mar-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite