|

|

|

|

|||||

|

|

|

ASML holds a technological monopoly on its machines.

Management was a bit more cautious about the 2026 outlook than it was in the prior quarter.

The stock doesn't look overly expensive, considering its growth and market position.

Finding stocks that aren't hitting all-time highs in the world of artificial intelligence (AI) investing is becoming increasingly difficult. The market is incredibly bullish right now, but there are a few stocks that are still on sale.

One of those is ASML (NASDAQ: ASML), a relatively unknown company that makes the advanced chip technology investors know today possible. Without ASML, AI would look far different, which underscores its importance. While ASML is still down around 35% from its all-time highs, it recently crashed 10% from recent highs due to poorly received quarterly earnings.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

The reaction was mostly around short-term sentiment, rather than long-term outlook. If you can expand your investing horizon beyond one year into the three- to five-year time frame, ASML looks like a genius buy right now, as the demand for its machines is only going to rise.

Image source: Getty Images.

ASML holds a technological monopoly on its extreme ultraviolet (EUV) lithography machines. These machines help chip manufacturers lay microscopic electrical traces on chips, and their product is the only one that can do so at the distances considered cutting-edge today. Currently, 3 nanometers between electrical traces is the best available technology; however, ASML clients, such as Taiwan Semiconductor Manufacturing, are slated to launch 2nm chips later this year.

Because ASML's machines are highly specialized, it has only a handful of clients, making it relatively easy to monitor demand. Chip foundries like Taiwan Semiconductor and Intel are among its fairly small client list, and these two are moving in opposite directions. While TSMC is expanding its chip foundry capabilities by building plants in the U.S. (it has made a $165 billion commitment here), Intel isn't doing so great. Its foundry business is operating at a loss, and its CEO is starting to cut investments in this area.

It appears that TSMC is capturing market share, while Intel is losing it, resulting in relatively even demand for ASML's machines. This prompted ASML management to pull back on its language regarding the 2026 forecast. Previously, management had stated that 2026 would be a significant growth year for the business. Now, it is treading a bit lightly, saying: "While we are still preparing for growth in 2026, we cannot confirm it at this stage. We will continue monitoring developments over the coming months."

This caused some investors to panic and sell off the stock, but was that a logical reaction?

ASML backing down from its prior stance that 2026 would be a near-guaranteed growth year is somewhat concerning. With increasing chip demand, it's clear that its machines will be in greater demand, so this mismatch seems a bit odd, but in light of the Intel news, it makes more sense.

Furthermore, ASML will need to continue innovating and developing new machines to advance toward emerging chip technologies. Moore's Law dictates that the number of transistors on a microchip doubles every two years, and ASML plays a critical role in ensuring that leaders remain on this upward trend.

Still, 2025 isn't shaping up to be all that bad of a year. Management expects about 15% sales growth for the year, which isn't bad considering the company's size. Additionally, its net bookings experienced a significant increase from the total in Q1. In Q2, ASML reported net bookings of 5.5 billion euros, up from 3.9 billion euros in Q1. This indicates long-term demand for its machines is rising, which is a positive sign for shareholders.

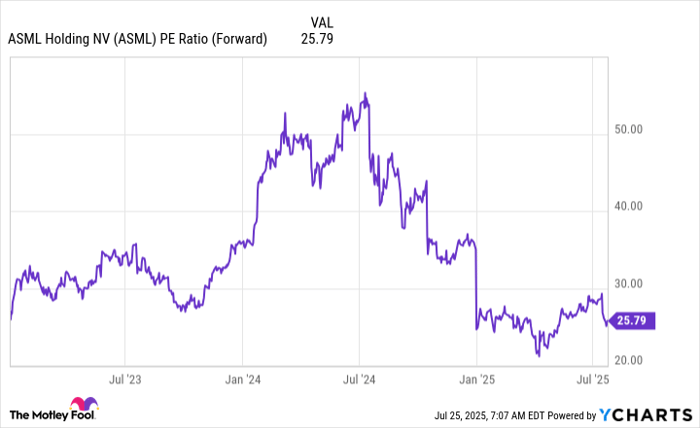

Currently, ASML trades for less than 26 times forward earnings, which isn't bad considering ASML is in a solid position and still posting solid growth.

ASML PE Ratio (Forward) data by YCharts

Although management is being slightly more cautious about 2026, I don't think investors need to be. ASML is a very important part of the chip industry, and it isn't going anywhere. Even if 2026 isn't the best year, most of that spending would likely be pushed out to 2027 and realized eventually.

I think this makes ASML a great stock to buy, hold, and forget about. The lumpy nature of ASML's business makes it more effective to analyze over the years, rather than by quarters. With the long-term trend heading toward more chips and more advanced ones, it bodes well for ASML, making it an attractive investment opportunity today.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of July 29, 2025

Keithen Drury has positions in ASML and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends ASML, Intel, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends the following options: short August 2025 $24 calls on Intel. The Motley Fool has a disclosure policy.

| 23 min | |

| 4 hours | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite