|

|

|

|

|||||

|

|

|

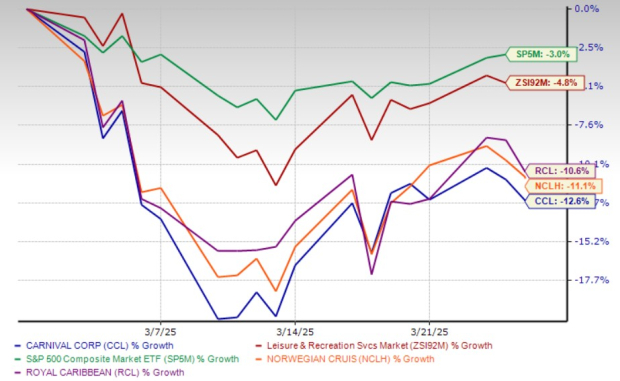

Carnival Corporation & plc CCL shares have declined 12.6% over the past month, significantly underperforming the leisure and recreation industry’s 4.8% decrease and the S&P 500’s 3% drop. The downturn is largely driven by mounting macroeconomic uncertainty and heightened scrutiny over industry taxation policies.

Recent comments from Commerce Secretary Howard Lutnick have ignited fresh concerns, as he questioned the cruise industry’s reliance on foreign-flagged vessels to sidestep U.S. taxes. This development sent shockwaves through the sector, triggering a broad sell-off in major cruise stocks, including Royal Caribbean Cruises Ltd. RCL and Norwegian Cruise Line Holdings Ltd. NCLH. While the long-term ramifications remain uncertain, the news has undoubtedly fueled short-term volatility in CCL shares, leaving investors wary amid the ongoing regulatory overhang.

Then again, high operating costs are concerning for the company. In the first quarter of fiscal 2025, cruise and tour operating expenses increased year over year to $3.77 billion from $3.71 billion. Several factors drove this uptick — elevated commissions, transportation costs and other expenses linked to higher ticket pricing, and higher onboard and other costs of sales. For fiscal 2025, it expects adjusted cruise costs, excluding fuel per ALBD (in constant currency), to increase 3.8% year over year (up from the prior mentioned 3.7%).

Carnival stock closed at $20.93 on Wednesday, still hovering well below its 52-week high of $28.72 but holding firmly above its low of $13.78. In the past month, CCL has underperformed other industry players like Royal Caribbean and Norwegian Cruise.

While the stock has faced near-term headwinds, its underlying fundamentals remain solid. With strong booking trends and sustained consumer demand for cruise travel, Carnival is well-positioned to navigate market volatility and capitalize on long-term growth opportunities.

Thanks to improved operational execution across its brands, Carnival has been witnessing solid booking trends for a few quarters now. In the fiscal first quarter, the company experienced another early start to a strong wave season, driven by its yield management strategy.

Entering the year with less inventory available for sale, the company secured higher prices in constant currency on bookings made during the quarter for the remainder of 2025. Its advanced booked position remains strong, with pricing at historical highs for each quarter and occupancy levels aligning with last year’s record.

The company continues to generate sustained demand, even for long-term sailings. With most of 2025 already booked, strong pricing trends continue in North America and Europe while efforts to build demand for future years remain underway. Booking volumes for 2026 sailings and beyond reached an all-time high, with prices in constant currency exceeding previous levels. The company’s booking curve remains the furthest out on record, reflecting continued demand for its offerings.

Carnival’s strategic investment in advertising is yielding significant returns, stimulating demand across its portfolio with the launch of several campaigns during the peak season. CCL’s Durable Wave marketing campaign saw considerable success, particularly with Flip, Lost in Paradise, which resonated strongly with audiences and drove key performance indicators across the board. The company highlighted the achievement as a testament to the marketing team’s ability to generate substantial engagement, even with computer-generated animation.

Looking ahead, CCL remains optimistic about the upcoming launch of Celebration Key, its exclusive new destination. With all five portals designed for guest enjoyment set to open, the company anticipates a strong reception when operations begin in July. Management reaffirmed that the project remains on schedule, with a structured ramp-up plan in place through the fourth quarter. As teams settle into these new operations, the focus remains on delivering the high-quality, immersive experiences that have become a hallmark of Carnival’s exclusive destinations.

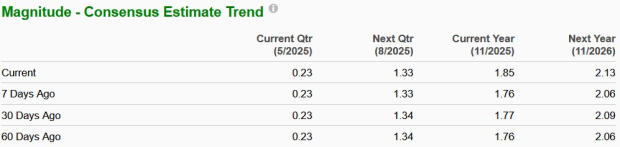

In the past 7 days, six analysts each have revised earnings estimates for 2025 and 2026, respectively. In the past 7 days, analysts have raised their estimates for the current and the next years by 5.1% to $1.85 and 3.4% to $2.13, respectively. These estimates indicate year-over-year growth rates of 28.9% and 16.5%, respectively.

The Zacks Consensus Estimate for 2025 and 2026 sales are pegged at $26.06 billion and $26.99 billion, suggesting 4.2% and 3.5% year-over-year growth, respectively.

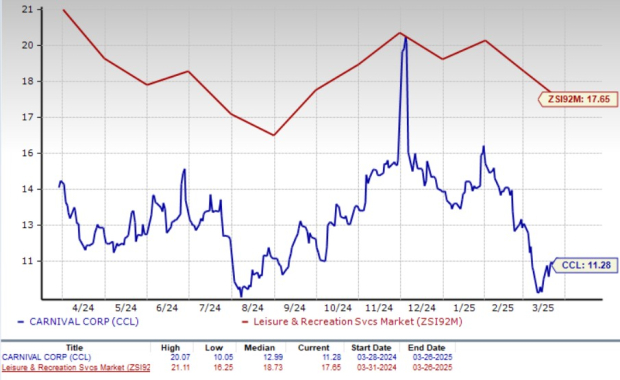

CCL is currently priced at an attractive discount relative to its industry, making it a compelling opportunity for investors. With a forward 12-month price-to-earnings (P/E) ratio of 11.28, below the industry average, Carnival’s valuation suggests room for upside, reinforcing its appeal for those looking to capitalize on its growth trajectory. Then again, other industry players like Royal Caribbean and Norwegian Cruise's P/E ratio stand at 14.14 and 9.08, respectively.

Carnival presents a compelling investment opportunity despite recent stock weakness, as its underlying fundamentals remain strong. The company continues to experience robust booking trends, with record-high pricing and strong occupancy levels extending into future years, signaling sustained demand for cruise travel. Strategic investments in marketing have successfully driven customer engagement, while the upcoming launch of Celebration Key is set to enhance its exclusive destination portfolio.

Despite near-term macroeconomic concerns and cost pressures, Carnival’s improving operational execution, favorable long-term outlook, and discounted valuation relative to industry peers make it an attractive buy for investors seeking growth potential in the travel and leisure sector. CCL currently has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-22 | |

| Feb-22 | |

| Feb-22 | |

| Feb-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite