|

|

|

|

|||||

|

|

|

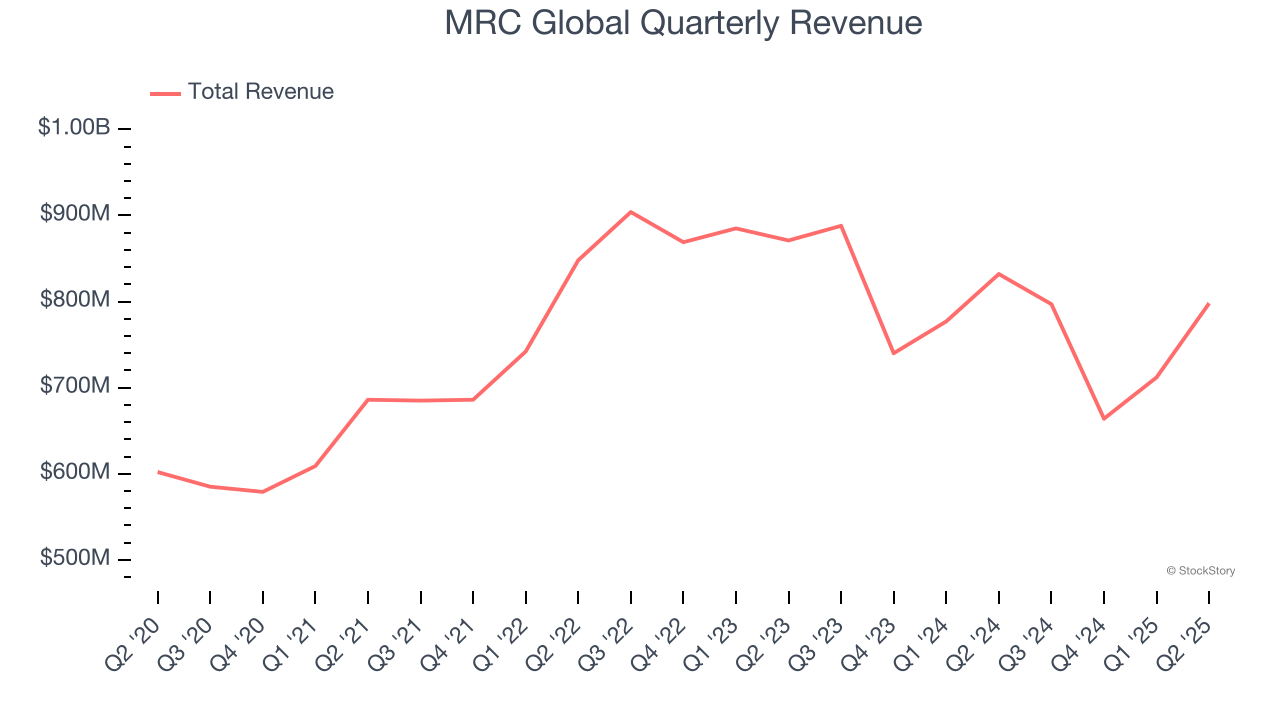

Fluid and gas handling company MRC (NYSE:MRC) reported Q2 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 4.1% year on year to $798 million. Its non-GAAP profit of $0.25 per share was in line with analysts’ consensus estimates.

Is now the time to buy MRC Global? Find out by accessing our full research report, it’s free.

Rob Saltiel, MRC Global’s President and CEO, stated, “We delivered a strong second quarter, with revenue rising 12% from the first quarter of 2025, at the top of our previous guidance range. All sectors contributed to the sequential revenue increase, led by PTI with 26% sales growth due to robust project activity across both the U.S. and international markets. Our Gas Utilities business continued its rebound with 10% sequential revenue growth, fueled by increased construction projects. Adjusted EBITDA surged 50% sequentially, with margins expanding 170 basis points, reflecting strong operating leverage. We also returned $15 million to shareholders through strategic share repurchases at an average price of $12.35 per share.

Producing bomb casings and tracks for vehicles during WWII, MRC (NYSE:MRC) offers pipes, valves, and fitting products for various industries.

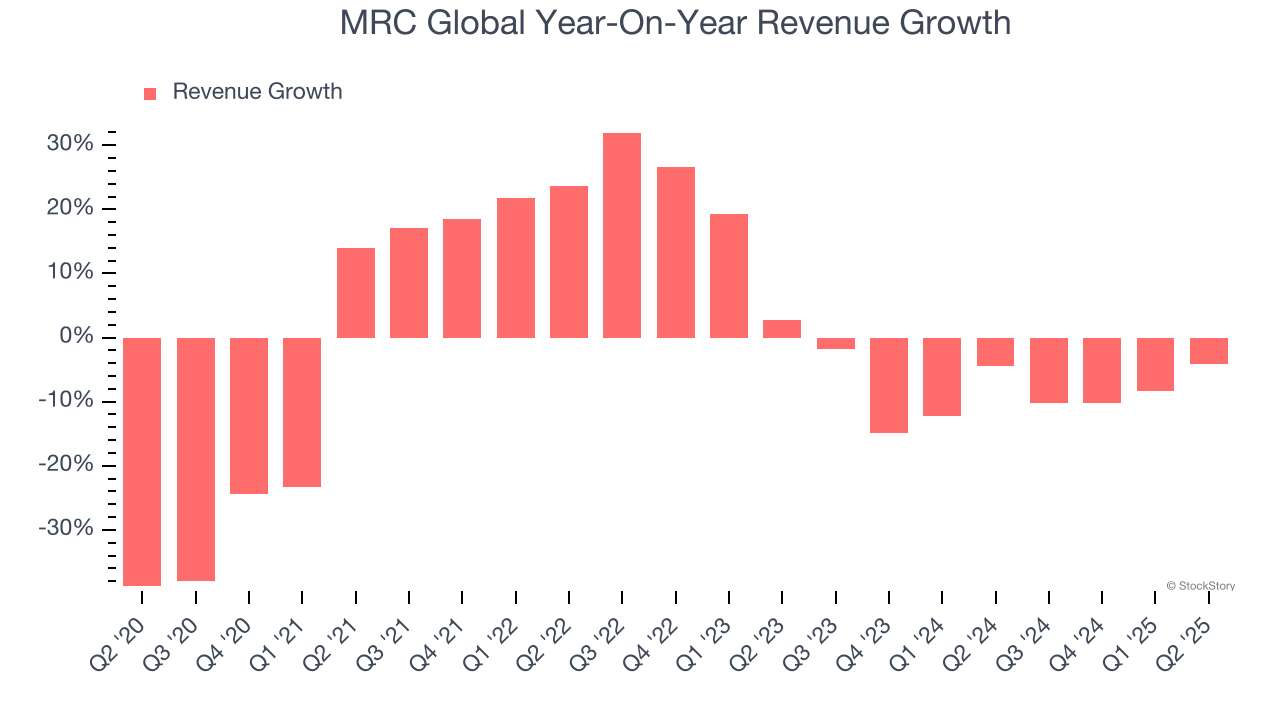

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, MRC Global struggled to consistently increase demand as its $2.97 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of poor business quality.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. MRC Global’s recent performance shows its demand remained suppressed as its revenue has declined by 8.2% annually over the last two years.

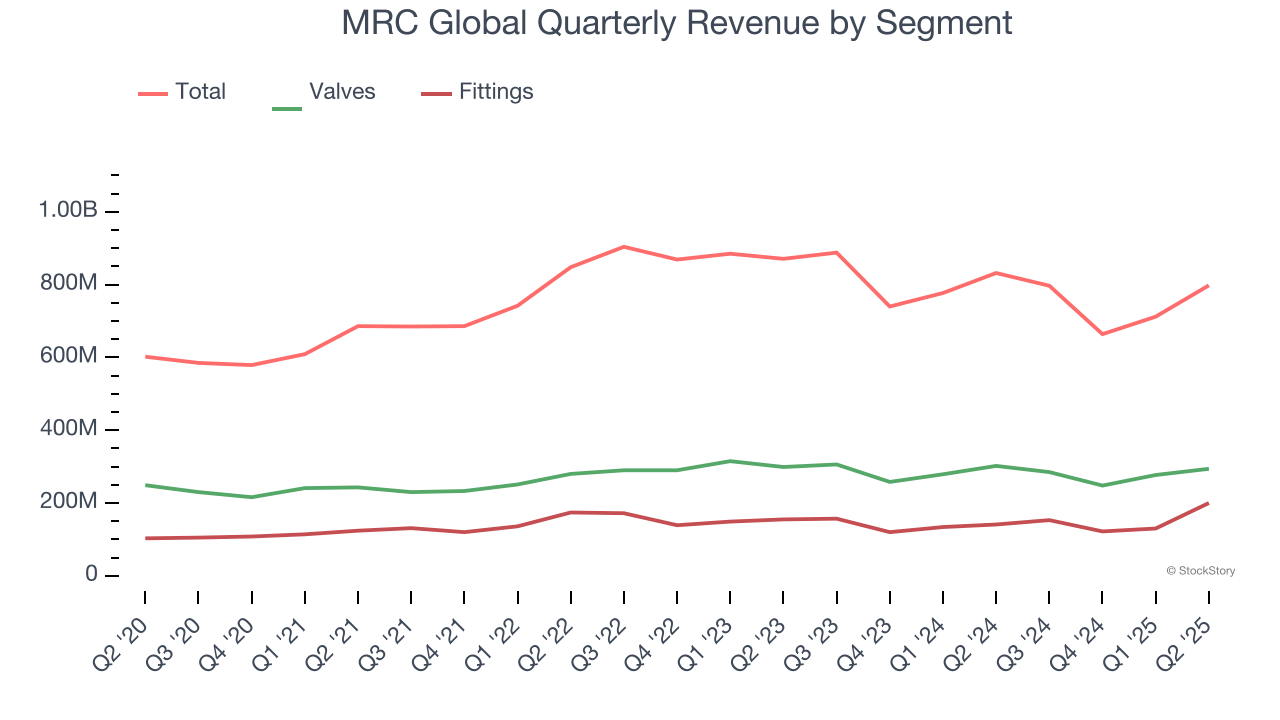

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Valves and Fittings, which are 36.8% and 25.1% of revenue. Over the last two years, MRC Global’s Valves revenue (fluid control) averaged 3.8% year-on-year declines while its Fittings revenue (pipe connectors) was flat.

This quarter, MRC Global’s revenue fell by 4.1% year on year to $798 million but beat Wall Street’s estimates by 1.7%.

Looking ahead, sell-side analysts expect revenue to grow 7.7% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and implies its newer products and services will fuel better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

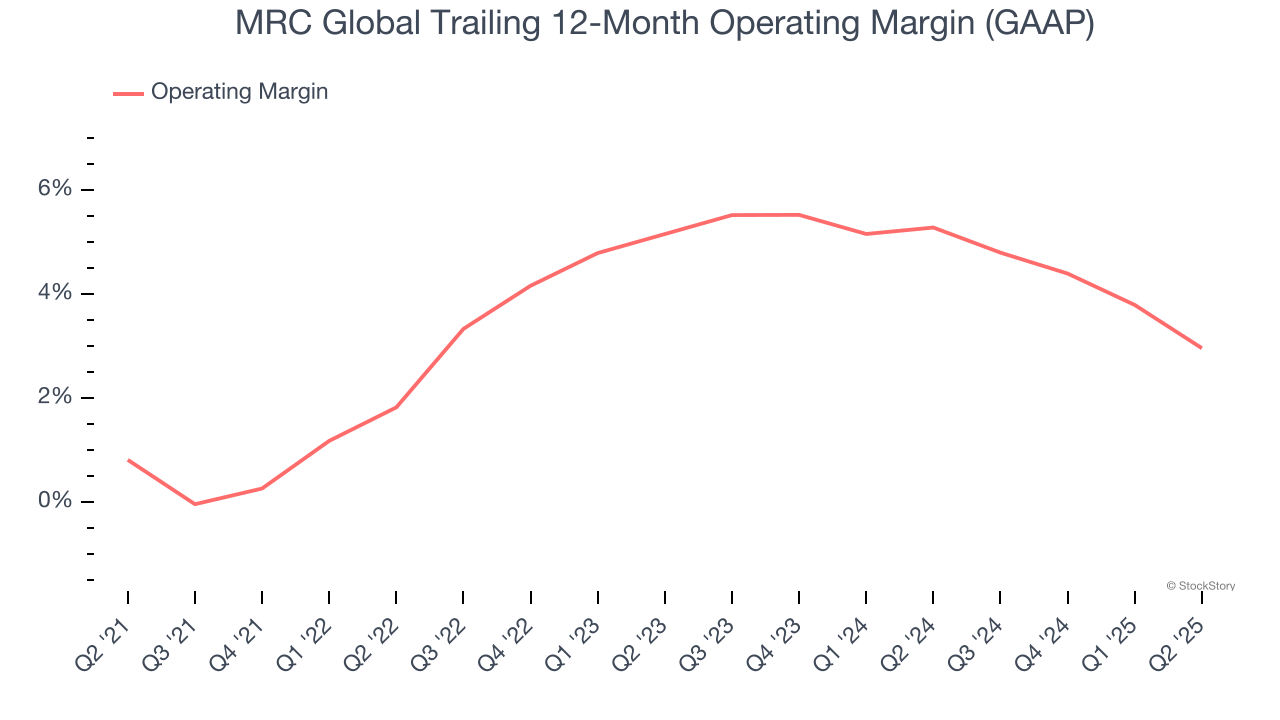

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

MRC Global was profitable over the last five years but held back by its large cost base. Its average operating margin of 3.4% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, MRC Global’s operating margin rose by 2.1 percentage points over the last five years.

In Q2, MRC Global generated an operating margin profit margin of 2.6%, down 3 percentage points year on year. Since MRC Global’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

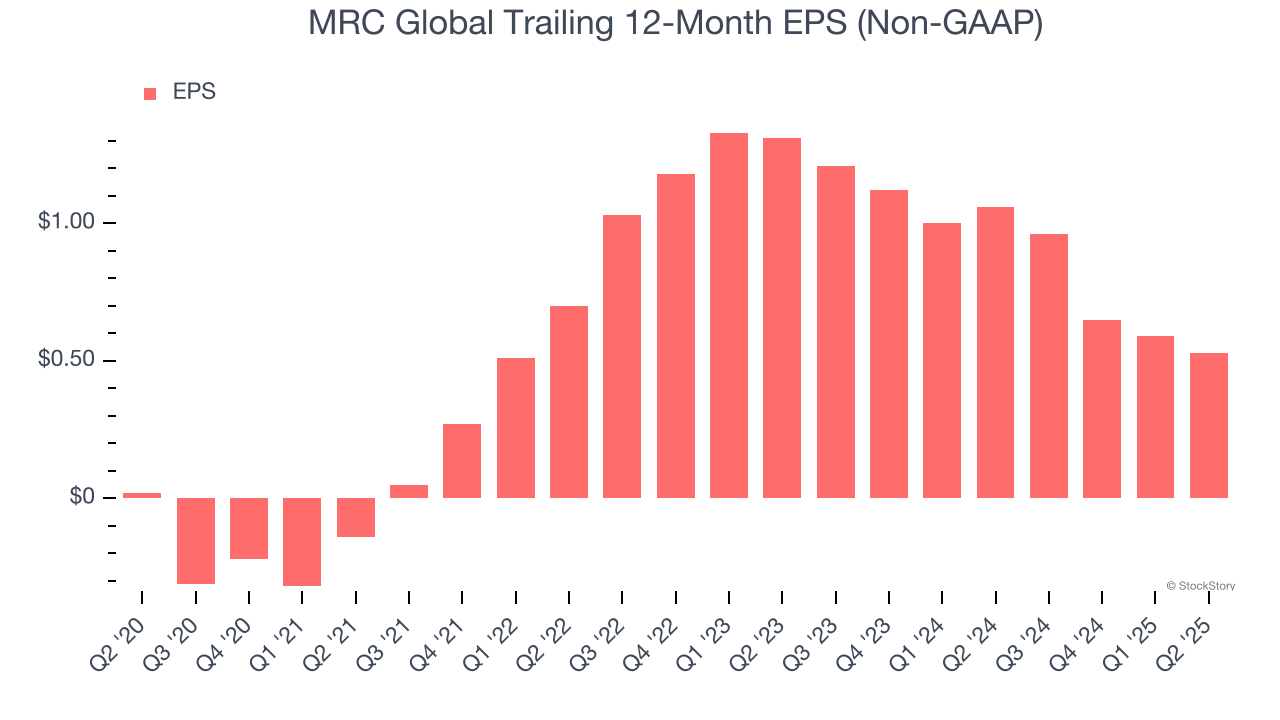

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

MRC Global’s EPS grew at an astounding 95.4% compounded annual growth rate over the last five years, higher than its flat revenue. This tells us management responded to softer demand by adapting its cost structure.

We can take a deeper look into MRC Global’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, MRC Global’s operating margin declined this quarter but expanded by 2.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For MRC Global, its two-year annual EPS declines of 36.4% mark a reversal from its (seemingly) healthy five-year trend. We hope MRC Global can return to earnings growth in the future.

In Q2, MRC Global reported adjusted EPS at $0.25, down from $0.31 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 2.7%. Over the next 12 months, Wall Street expects MRC Global’s full-year EPS of $0.53 to grow 133%.

We were impressed by how significantly MRC Global blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its Valves revenue missed. Zooming out, we think this was a solid print. The stock traded up 6.1% to $15.25 immediately following the results.

Sure, MRC Global had a solid quarter, but if we look at the bigger picture, is this stock a buy? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Nov-05 | |

| Nov-05 | |

| Nov-05 |

MRC: Q3 Earnings Snapshot

Associated Press Finance

|

| Nov-05 |

MRC Global Announces Third Quarter 2025 Results

GlobeNewswire

|

| Nov-05 |

DNOW Reports Third Quarter 2025 Results

Business Wire

|

| Oct-23 | |

| Oct-21 | |

| Oct-14 |

3 Value Stocks with Warning Signs

StockStory

|

| Oct-13 | |

| Oct-01 | |

| Aug-18 |

3 Volatile Stocks That Concern Us

StockStory

|

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

MRC: Q2 Earnings Snapshot

Associated Press Finance

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite