|

|

|

|

|||||

|

|

|

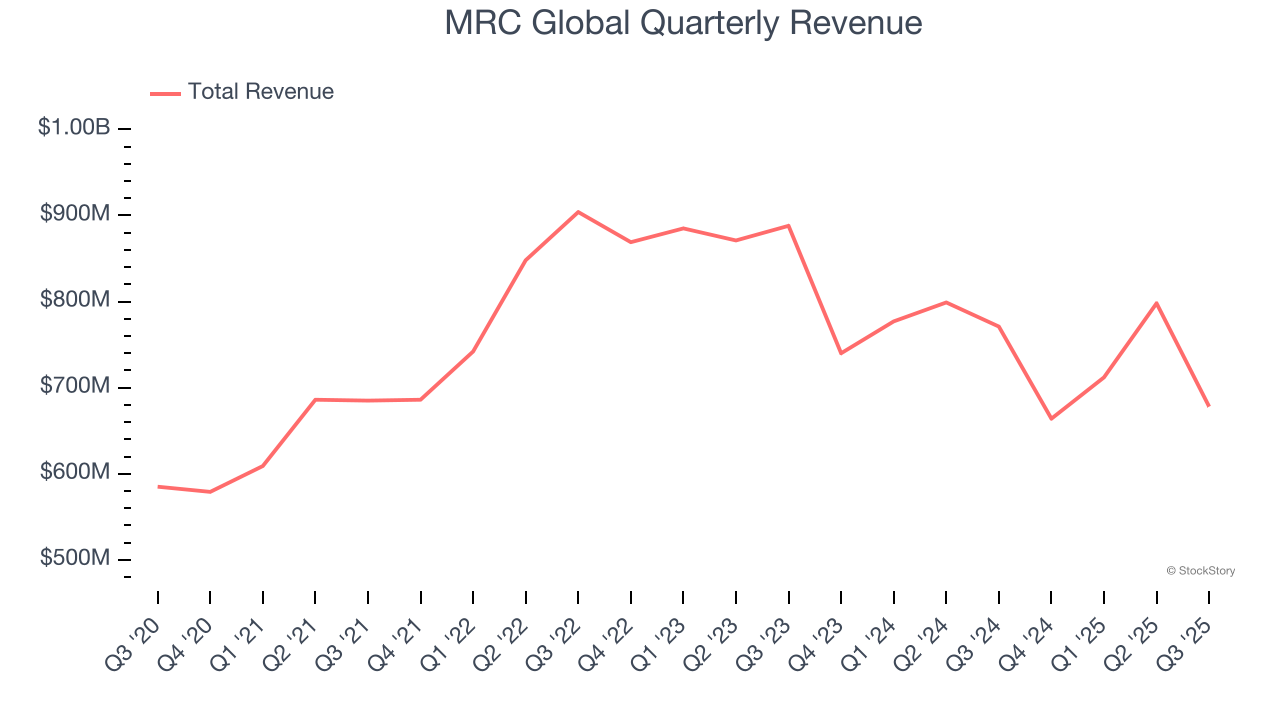

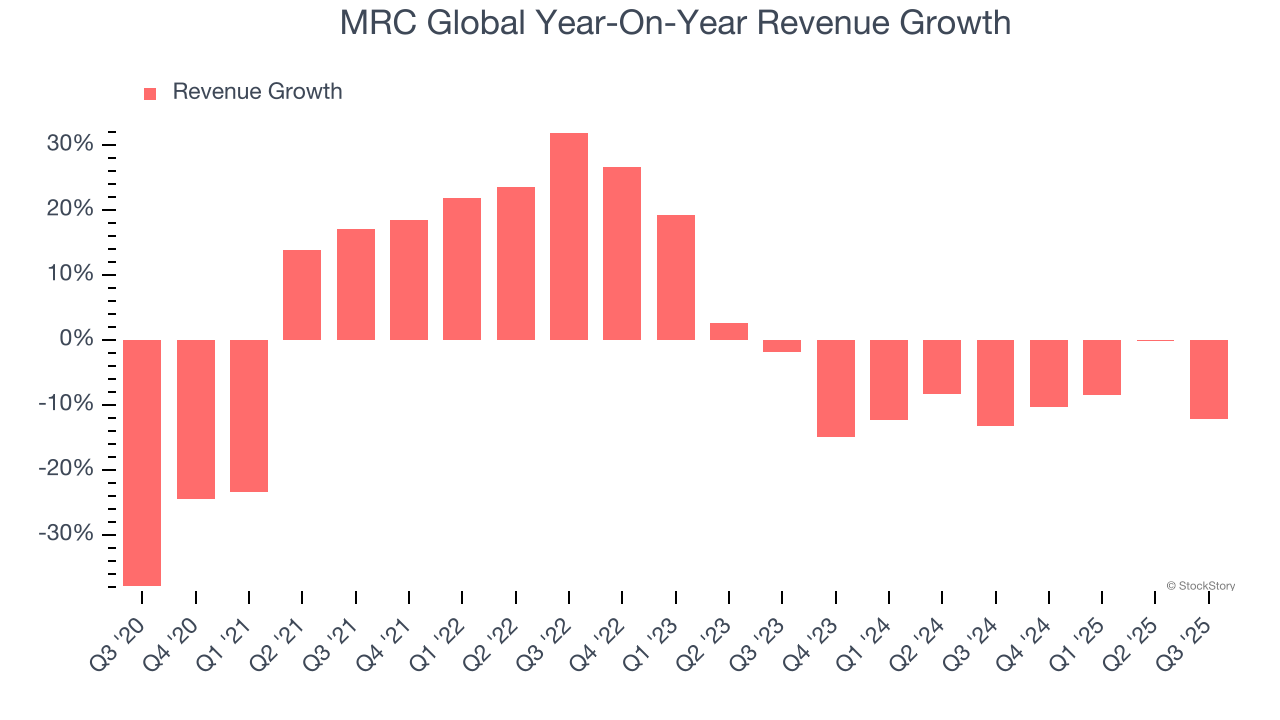

Fluid and gas handling company MRC (NYSE:MRC) missed Wall Street’s revenue expectations in Q3 CY2025, with sales falling 12.1% year on year to $678 million. Its non-GAAP profit of $0.13 per share was 60.6% below analysts’ consensus estimates.

Is now the time to buy MRC Global? Find out by accessing our full research report, it’s free for active Edge members.

Rob Saltiel, MRC Global’s President and CEO, commented, “The implementation of our new enterprise resource planning (ERP) system in our U.S. segment encountered significant challenges that adversely impacted our revenues, profitability, and cash flows, during our third quarter. We deployed extensive resources to ensure that customer service levels were maintained and that business operations could function as we addressed the system issues. I am pleased to report that our financial and operations performance improved dramatically by the end of our third quarter and that this more normalized performance has continued throughout the month of October. We greatly appreciate the patience of our customers and the hard work by the entire MRC Global team during this system transition.”

Producing bomb casings and tracks for vehicles during WWII, MRC (NYSE:MRC) offers pipes, valves, and fitting products for various industries.

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, MRC Global struggled to consistently increase demand as its $2.85 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. MRC Global’s recent performance shows its demand remained suppressed as its revenue has declined by 9.9% annually over the last two years.

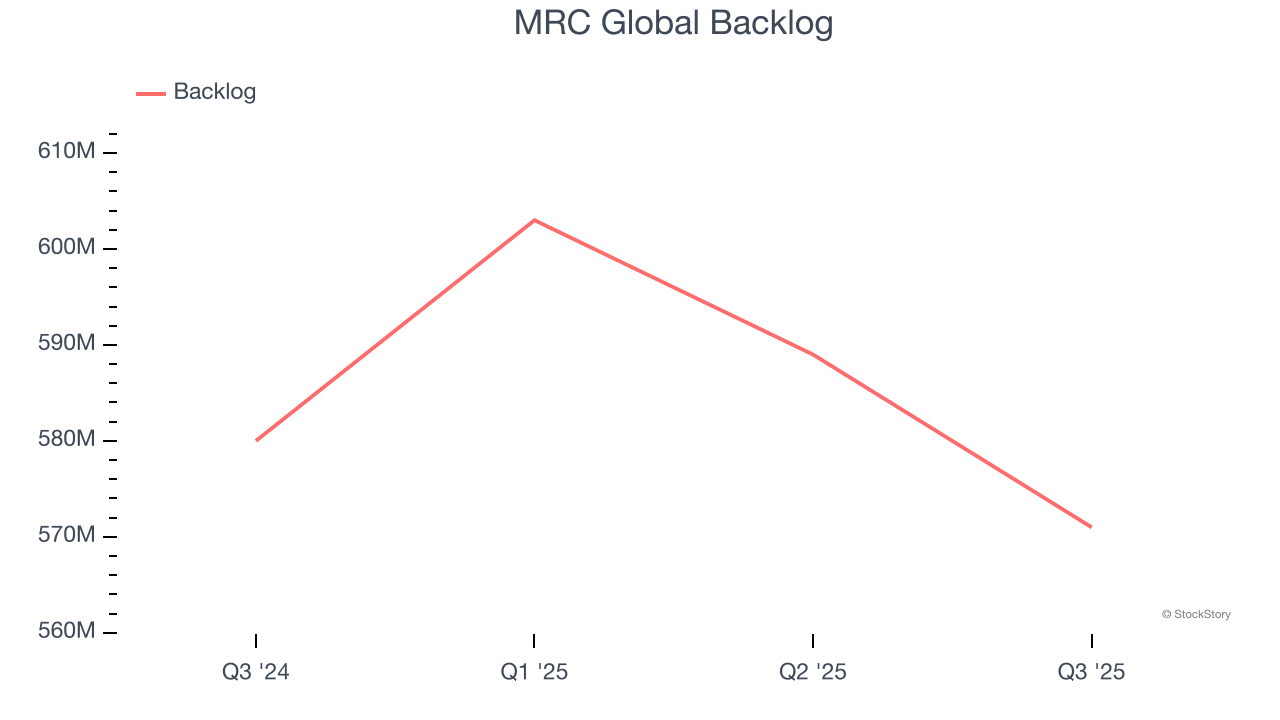

MRC Global also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. MRC Global’s backlog reached $571 million in the latest quarter and averaged 1.6% year-on-year declines over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for MRC Global’s products and services but raises concerns about capacity constraints.

This quarter, MRC Global missed Wall Street’s estimates and reported a rather uninspiring 12.1% year-on-year revenue decline, generating $678 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 15.1% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

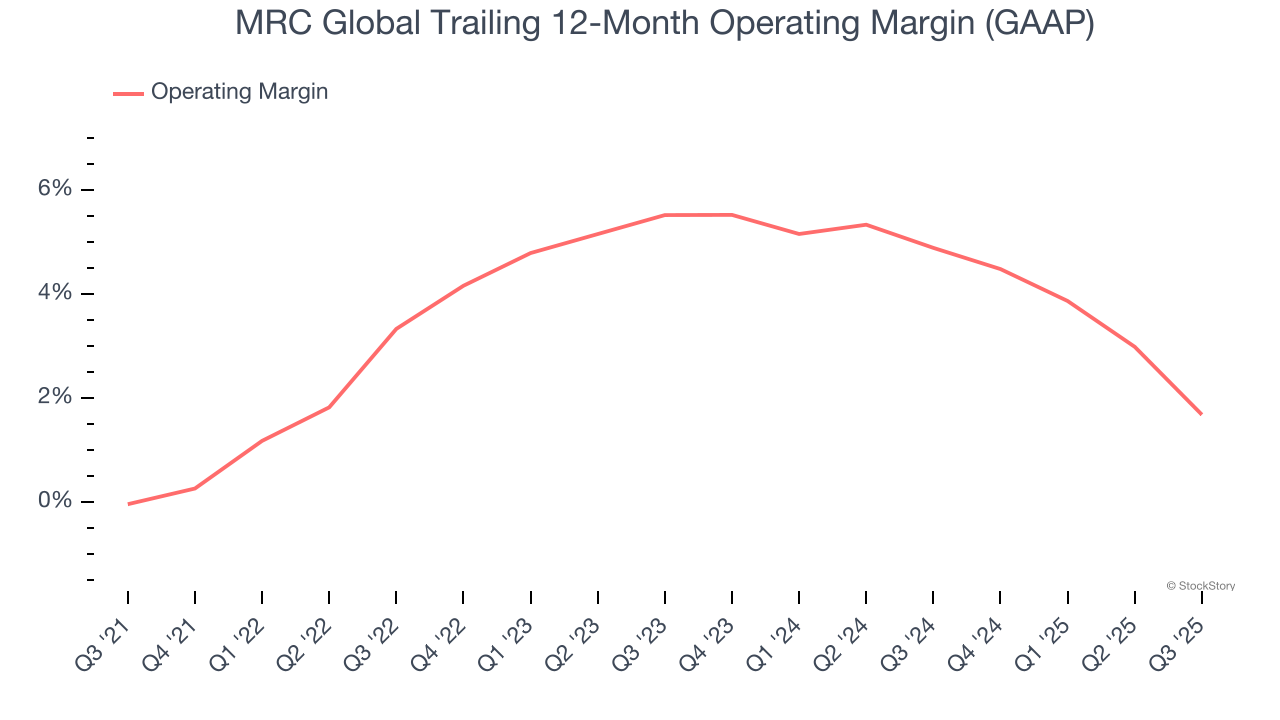

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

MRC Global was profitable over the last five years but held back by its large cost base. Its average operating margin of 3.3% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, MRC Global’s operating margin rose by 1.7 percentage points over the last five years.

In Q3, MRC Global’s breakeven margin was down 5.2 percentage points year on year. Conversely, its gross margin actually rose, so we can assume its recent inefficiencies were driven by increased operating expenses like marketing, R&D, and administrative overhead.

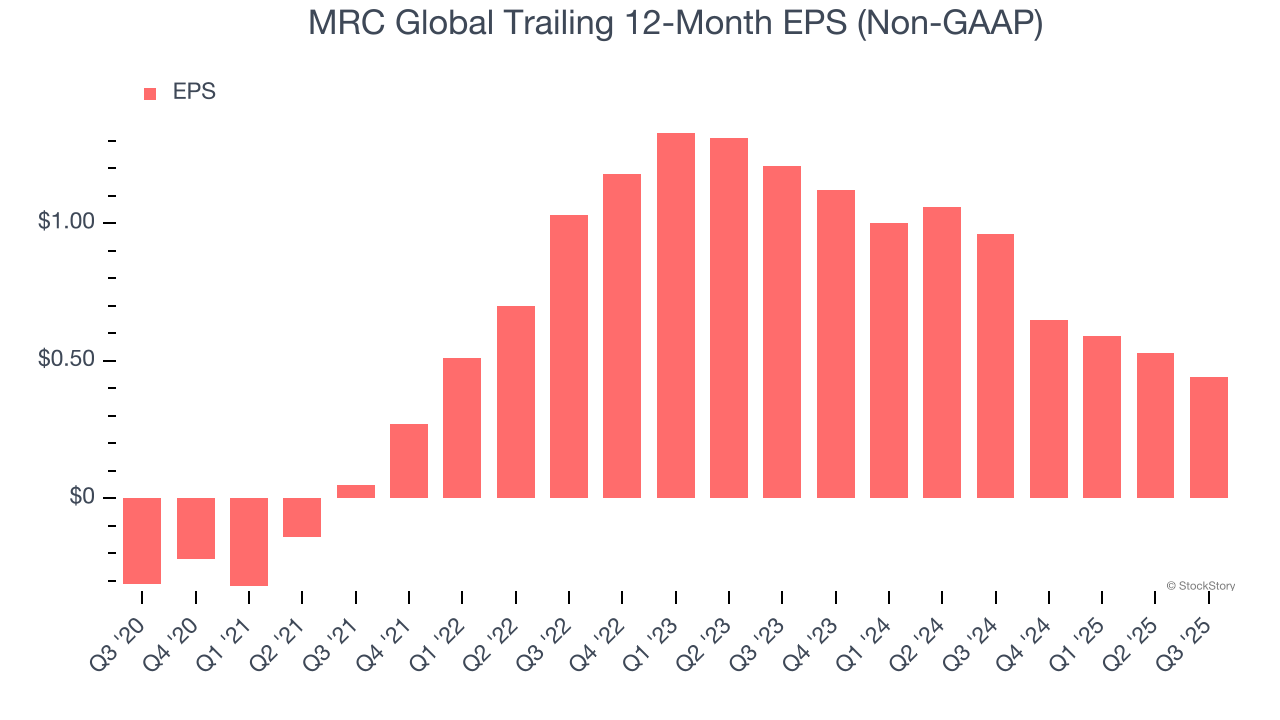

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

MRC Global’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for MRC Global, its EPS declined by more than its revenue over the last two years, dropping 39.7%. This tells us the company struggled to adjust to shrinking demand.

Diving into the nuances of MRC Global’s earnings can give us a better understanding of its performance. MRC Global’s operating margin has declined over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, MRC Global reported adjusted EPS of $0.13, down from $0.22 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects MRC Global’s full-year EPS of $0.44 to grow 178%.

We struggled to find many positives in these results. Its Valves revenue missed and its revenue fell short of Wall Street’s estimates. Overall, this was a softer quarter.

Is MRC Global an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Nov-05 | |

| Nov-05 | |

| Nov-05 |

MRC: Q3 Earnings Snapshot

Associated Press Finance

|

| Nov-05 |

MRC Global Announces Third Quarter 2025 Results

GlobeNewswire

|

| Nov-05 |

DNOW Reports Third Quarter 2025 Results

Business Wire

|

| Oct-23 | |

| Oct-21 | |

| Oct-14 |

3 Value Stocks with Warning Signs

StockStory

|

| Oct-13 | |

| Oct-01 | |

| Aug-18 |

3 Volatile Stocks That Concern Us

StockStory

|

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

MRC: Q2 Earnings Snapshot

Associated Press Finance

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite