|

|

|

|

|||||

|

|

|

SoundHound AI stock shot up after its latest report, thanks to its outstanding growth and improved guidance.

The company's voice AI solutions are in hot demand, and its terrific growth pace has legs.

Though the stock is expensive right now, it can justify its valuation because of its rapid growth.

SoundHound AI (NASDAQ: SOUN) has had a forgettable 2025 despite reporting strong growth quarter after quarter, with shares of the company trading down about 20% so far this year as of this writing. However, it looks like the voice-powered artificial intelligence (AI) company's fortunes are about to change following its latest quarterly results.

SoundHound AI stock shot up more than 26% after releasing its second-quarter 2025 results on Aug. 7. Let's see what has investors excited and check why this beaten-down AI stock has the potential to double by next year.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

SoundHound AI provides a platform that allows its customers in various industries to develop different types of voice AI systems, including AI assistants, chatbots, and online ordering systems (among other things). The company's platform has quickly gained traction, and it's now being deployed in the automotive, hospitality, healthcare, retail, financial services, and e-commerce industries.

That's why revenue more than tripled in the previous quarter to a record level of $43 million. The company also managed to reduce its adjusted loss per share by a penny to $0.03 despite a significant increase of 64% in its research and development expenses and a 180% spike in sales and marketing outlay.

Wall Street would have settled for $33 million in revenue and a loss of $0.09 per share. SoundHound blew past those estimates thanks to new customers last quarter. The company reports that 15 large enterprise customers are now using its voice-powered agentic AI platform, Amelia, which is impressive considering that it was introduced just three months ago.

The company reported "numerous wins, renewals, expansions, and cross-selling" in the restaurant industry. Other customer additions included a new automotive original equipment manufacturer (OEM) in China and bigger contracts with four of its financial services customers. In all, it benefited from a combination of new customers and more business from existing ones.

This trend is likely to continue, considering the $140 billion total addressable market that management projects across various industries. Also, the company says that it has been granted over 190 patents for its voice AI solutions, with another 110 pending. A strong intellectual property (IP) portfolio should provide a competitive advantage in the voice AI market and open up new sources of revenue growth through licensing.

As such, it is easy to see why the company is confident about its prospects and has raised its full-year revenue guidance to a range of $160 million to $178 million. That's up from its earlier guidance range of $157 million to $177 million. The updated forecast indicates that its top line could more than double in 2025 from last year's $85 million.

However, don't be surprised to see the company exceed its own expectations in 2025 and deliver stronger growth next year.

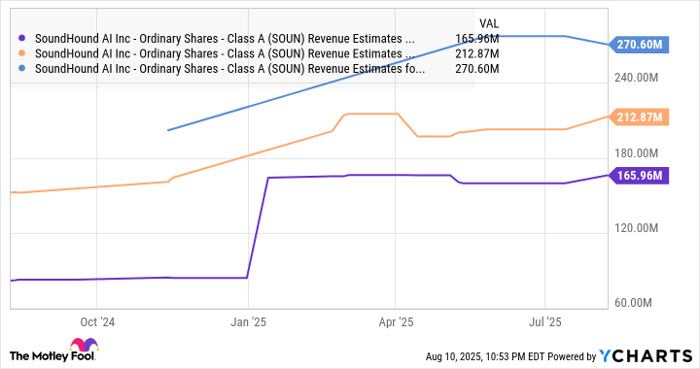

SoundHound operates in a fast-growing and lucrative market and is quickly expanding its customer base. As a result, there is a strong possibility that it will be able to maintain its outstanding revenue growth in 2026 as well. Consensus estimates, however, project a slowdown in its top-line growth next year, followed by an acceleration in 2027.

Data by YCharts.

But then, investors should note that SoundHound's cumulative subscriptions and bookings backlog stood at $1.2 billion at the end of last year. This metric provides insight into its future revenue generation ability and indicates that it is in a position to blow past consensus estimates in 2026 as well.

Assuming the company's growth next year slows down to even 50% in 2026 from the 100% increase that it is projecting in 2025, its top line could jump to at least $253 million next year (based on the midpoint of its 2025 revenue range).

The stock trades at 47 times sales right now. That multiple is, of course, expensive. But SoundHound's remarkable growth justifies its rich valuation, especially considering that AI companies with slower growth command a bigger premium. So there is a good chance that the market could continue putting a premium on the company's valuation.

A price-to-sales ratio of even 40 in 2026 could take the stock's market cap to more than $10 billion, which is around double its current valuation. However, SoundHound AI could deliver stronger growth than what's projected above, which could lead to even bigger gains in the market.

Before you buy stock in SoundHound AI, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and SoundHound AI wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $653,427!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,119,863!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 11, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

| Feb-15 | |

| Feb-14 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 | |

| Feb-10 | |

| Feb-09 | |

| Feb-09 | |

| Feb-07 | |

| Feb-05 | |

| Feb-05 | |

| Feb-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite