|

|

|

|

|||||

|

|

|

Nvidia relies on Taiwan Semiconductor Manufacturing Company to build its high-demand GPUs.

TSMC's business relies less on AI developments than Nvidia's, reducing long-term risks.

TSMC's valuation leaves it with more upside than Nvidia's stock, which has a lot of future growth priced into it.

If you look back at the past couple of years, there's arguably no stock that has received as much attention as Nvidia (NASDAQ: NVDA). The current artificial intelligence (AI) boom has propelled Nvidia into the spotlight and to being the world's most valuable public company. As of market close on Aug. 8, Nvidia's market cap is $4.55 trillion, more than $570 billion larger than second-place Microsoft.

There are plenty of things to love about Nvidia's business, especially regarding AI, but if you're looking for an AI-related stock that could outperform it between now and 2030, my prediction would be Taiwan Semiconductor Manufacturing Company (NYSE: TSM) (TSMC).

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

I'm not saying that in 2030, TSMC will be worth more than Nvidia -- TSMC's market cap is currently around $3.2 trillion less than Nvidia's -- but if today is the starting point, TSMC has a business that puts its stock in a good position to outperform Nvidia's in the next five years.

Image source: Getty Images.

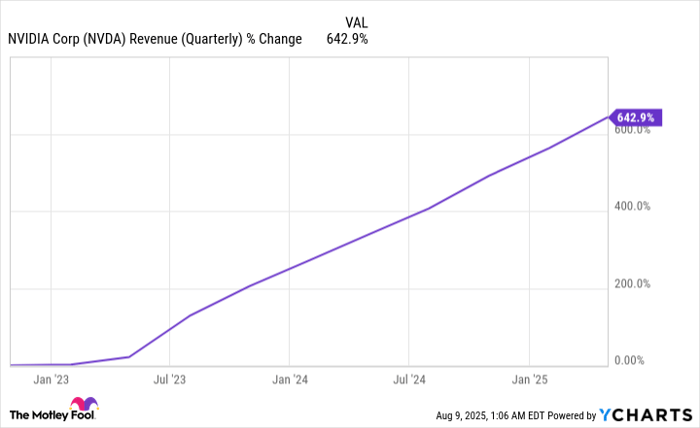

Over the past three years, Nvidia's stock is up 920%. When you look at what really matters, Nvidia's business comes down to graphic processing units (GPUs). GPUs are a key part of data centers, which power and enable AI training, deployment, and scaling.

Nvidia is far and away the main supplier of AI-focused GPUs, with an estimated market share of over 90%. This virtual monopoly has paid off for Nvidia (quite literally), increasing its revenue from $8.3 billion in its 2023 fiscal first quarter to $44 billion in its 2026 fiscal first quarter (ended April 27).

NVDA Revenue (Quarterly) data by YCharts

Despite how valuable Nvidia and its GPUs are to the AI world, Nvidia wouldn't be able to produce them without TSMC, the exclusive manufacturer of Nvidia's GPUs and advanced chips.

If Nvidia is a flashy sports car in the AI ecosystem, TSMC is the engine that makes its performance possible, which is why I'm comfortable calling the semiconductor manufacturer an AI stock despite not presenting itself as such or having a consumer-facing AI product.

It helps to see TSMC's impact by working backward. Consumer-facing products like generative AI (ChatGPT, Gemini, etc.) must be trained using tons of data. This training isn't possible without data centers. Most of these data centers run on Nvidia chips. Nvidia chips are built by TSMC.

Although demand for TSMC-manufactured AI-related chips has driven much of its recent revenue growth, it doesn't have to rely solely on them for long-term success. Its high-power computing segment, which includes its AI-related chips, was 60% of its $30 billion in revenue in the second quarter. That's admittedly a decent bit, but TSMC's business relies more on the broad tech world, and not just AI developments.

Lots of companies rely on TSMC to manufacture their chips. Everything from smartphones to laptops to cars to gaming consoles to data center servers all contain semiconductors manufactured by TSMC. Its client list includes Apple, Broadcom, AMD, and Qualcomm, just to name a few.

TSMC's diversified revenue streams reduce some potential hiccups. If AI spending and demand slows, TSMC has other segments that can pick up the slack. Nvidia's business, on the other hand, will take a major hit. Data centers accounted for over 88% of its revenue last quarter.

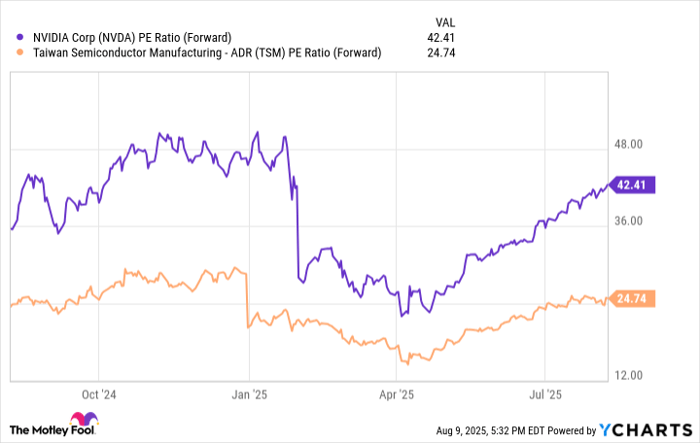

At the time of this writing, Nvidia is trading at 42.4 times earnings estimates, and TSMC is trading at 24.7 times earning estimates. Although TSMC isn't considered "cheap" by many standards, it's nowhere near as expensive as Nvidia and is much more fairly valued.

NVDA PE Ratio (Forward) data by YCharts

TSMC's lower valuation leaves much more room for growth over the next five years. At Nvidia's valuation, it seems to have a lot of future growth already priced into the stock, which leaves it susceptible to a sharp pullback if it falls short of its lofty expectations.

That's not to say that TSMC's stock can't experience a pullback, but its valuation gives it a larger margin of error and more upside. When we look back five years from now, I wouldn't be the least bit surprised to see TSMC's stock has outperformed Nvidia's from this point.

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $653,427!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,119,863!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 11, 2025

Stefon Walters has positions in Apple and Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Nvidia, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-15 | |

| Feb-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite