|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Micron Technology, Inc. MU forecasts industry DRAM bit demand to grow in the high-teen percentage range in 2025, mainly driven by the rising demand for AI-driven applications. The memory chip maker’s DRAM revenues climbed 51% year over year and 15% sequentially to $7.1 billion and represented 76% of total sales in the third quarter of fiscal 2025. Record sales in the data center end market and accelerating High Bandwidth Memory (“HBM”) adoption mainly drove DRAM revenues higher.

The growing adoption of AI servers is reshaping the DRAM market as these systems require significantly more memory than traditional servers. This is boosting demand for both high-capacity DIMMs (Dual In-line Memory Module) and low-power server DRAM. Micron is capitalizing on this trend with its leadership in DRAM technology and a strong product roadmap that includes HBM4, slated for volume production in 2026.

Tight supply conditions are another factor supporting the optimistic outlook for Micron’s DRAM products. The company intends to keep non-HBM DRAM bit supply growth below industry demand to maintain pricing discipline and profitability.

With AI adoption expanding across data center, mobile and automotive markets, Micron appears well-positioned to benefit from robust DRAM demand in the near term. The Zacks Consensus Estimate for fiscal 2025 indicates that DRAM revenues will soar approximately 59% year over year to $27.95 billion.

Although there are no U.S. stock exchange-listed direct competitors for MU in the memory chip space, Intel Corporation INTC and Broadcom Inc. AVGO play key roles in the HBM supply chain and AI hardware ecosystem.

Intel is developing its AI accelerators that rely on high-performance memory like HBM. Although Intel doesn't manufacture HBM chips, its Gaudi AI chips will require a robust HBM supply, and any shift in memory partnerships could impact Micron's position.

Meanwhile, Broadcom designs custom application-specific integrated circuits used in AI infrastructure that often include integrated HBM. As demand for Broadcom’s AI chips grows, it could influence how HBM suppliers like Micron allocate their future supply.

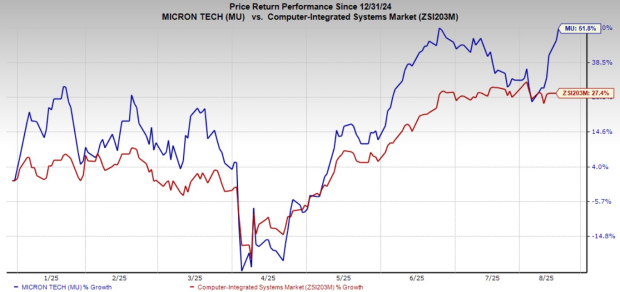

Shares of Micron Technology have risen around 51.8% year to date compared with the Zacks Computer – Integrated Systems industry’s gain of 27.4%.

From a valuation standpoint, MU trades at a forward price-to-sales ratio of 3, lower than the industry’s average of 3.72.

The Zacks Consensus Estimate for Micron Technology’s fiscal 2025 and 2026 earnings implies a year-over-year increase of approximately 497.7% and 57.9%, respectively. Estimates for fiscal 2025 and 2026 have been revised upward in the past 60 days.

Micron Technology currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 10 hours | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite