|

|

|

|

|||||

|

|

|

Apple’s U.S. manufacturing investment could lower its tariff expense.

The company’s results are improving, but growth is still sluggish.

Apple needs to justify its lofty valuation with AI-related product upgrades that are well-received by its diverse user base.

After closing at $202.69 per share on Aug. 5, Apple (NASDAQ: AAPL) stock soared a staggering 13% in just three days to finish Aug. 8 at $229.09 per share.

The move pole-vaulted the tech giant's market cap to $3.404 trillion -- a whopping $394 billion gain. That's like creating a company the size of Home Depot out of thin air.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

After languishing for most of the year, let's determine if Apple has what it takes to join Nvidia (NASDAQ: NVDA) and Microsoft (NASDAQ: MSFT) in the $4 trillion market cap club, and if the growth stock is a buy now.

Image source: Getty Images.

Apple's sudden pop came in response to its $100 billion manufacturing program. Announced last week, the program will create American jobs and onshore some of Apple's complex supply chain.

Due to Apple CEO Tim Cook's visit to the White House and Apple's manufacturing commitment, President Trump said that Apple would be 100% exempt from a specific tariff on imported semiconductors. The potential for Apple to reduce its costly tariff expense, and maybe even get government support for its onshoring efforts, is undoubtedly a boon for the company's near-term prospects.

Apple isn't the only mega-cap company that is trying to work with the current administration on tariffs. On Monday, reports indicated that Nvidia made a deal with President Trump, allowing the chipmaker to resume exporting its H20 chips in exchange for giving the U.S. government 15% of its revenue from China. The H20 is a scaled-down version of Nvidia's most advanced chips, which are custom-built for Chinese markets to comply with trade restrictions. The current administration intends to retain certain tariffs, but it also appears willing to negotiate deals with big businesses.

Apple's manufacturing news is positive, based on the near-term impact of tariffs. The investment could help Apple reduce its sensitivity to trade tensions and geopolitical risk. However, it's unclear how it impacts Apple's long-term investment thesis. Apple has mastered the art of managing a global supply chain to achieve cost advantages and boost its profit margins. Onshoring some of its supply chain could lead to higher costs.

However, Apple has yet to make a meaningful splash in artificial intelligence (AI) -- which is one of the main reasons why the tech giant has been lagging behind the performance of other, more defined AI winners like Nvidia and Microsoft.

In Apple's defense, the company has built on Apple Intelligence and released a new design update called Liquid Glass. Overall, the market is not impressed with the company's AI efforts, considering how sluggish Apple's growth has been in recent years.

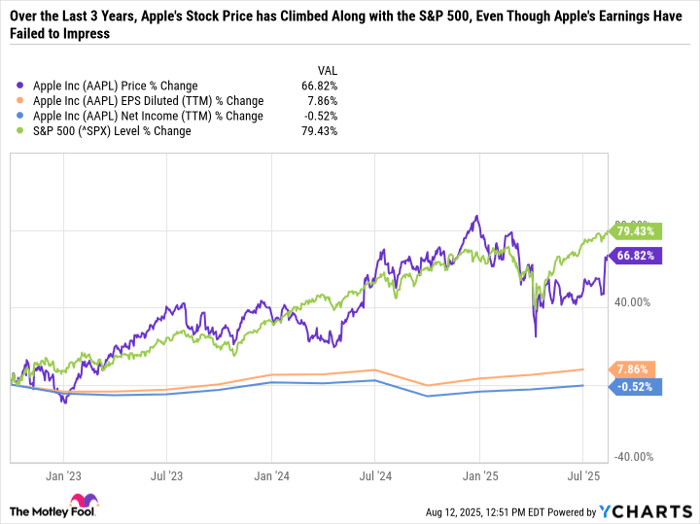

Apple has heavily relied on its high-margin services segment and stock buybacks to drive earnings to offset weak results from its product segment. Apple's services, which include iCloud, Apple Music, and Apple TV+, have been the standout for years now. But Apple's bottom line depends more on key products, like iPhone, Mac, iPad, and wearables.

Investors breathed a sigh of relief after Apple's latest quarter -- the third quarter of fiscal 2025 -- which showed a significant improvement in its product segment. Revenue grew 10% and diluted earnings per share (EPS) jumped 12% including double-digit growth in iPhone, Mac, and services. Despite the solid quarter, Apple's net income has slightly declined over the last three years, so its earnings are only up due to buybacks. But the stock price has gone up substantially, which has made Apple relatively expensive.

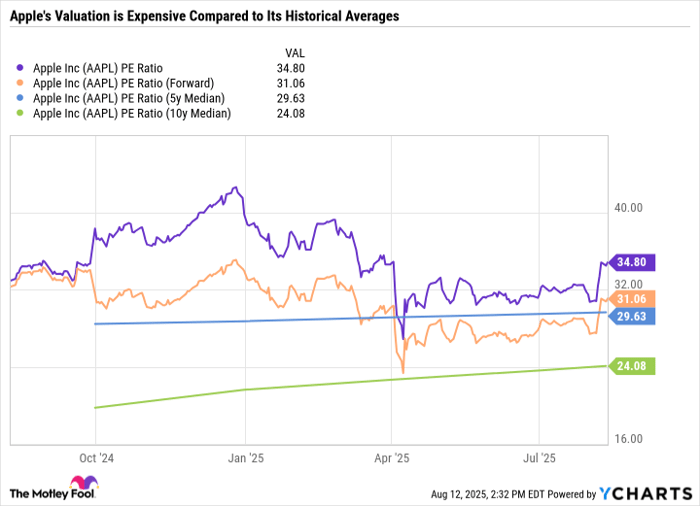

Apple's results are headed in the right direction, but the valuation is far from cheap. In fact, Apple's forward price-to-earnings (P/E) ratio, which is the stock price divided by analyst consensus EPS estimates over the next 12 months, is higher than its five-year and 10-year median P/E ratios. Even if Apple performs as expected and the stock price doesn't move for a year, it will still be relatively expensive.

AAPL PE Ratio data by YCharts.

Apple is taking the right approach to integrating AI across its product suite. Apple's competitive advantages are its design, user-friendly products, seamless integration of software and hardware, and comprehensive product offerings for consumers and businesses. In other words, the everyday usefulness of Apple's AI features is the most important performance indicator.

Investors who agree with Apple's deliberate approach to AI may still want to consider buying the stock now, despite the premium valuation. However, given how pricey Apple is, its road to $4 trillion in market cap will likely need to come from earnings growth rather than valuation expansion.

With a market cap of $3.418 trillion at the time of this writing, Apple would have to jump 17% to cross $4 trillion. It could certainly grow earnings by that much in a year or two. And if investors like what the company is doing with AI, it could maintain its higher-than-historical valuation.

All told, I expect Apple to cross $4 trillion in market cap by the end of 2026 -- but investors shouldn't expect the company to get there overnight -- even after adding $392 billion in market cap in just three days.

Before you buy stock in Apple, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Apple wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $663,630!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,115,695!*

Now, it’s worth noting Stock Advisor’s total average return is 1,071% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 13, 2025

Daniel Foelber has positions in Nvidia. The Motley Fool has positions in and recommends Apple, Home Depot, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 34 min | |

| Feb-28 |

Iran Says Khamenei Killed As U.S.-Israeli Attacks Continue; Dow Jones Futures Loom

AAPL

Investor's Business Daily

|

| Feb-28 | |

| Feb-28 |

Trump Says Khamenei Killed In U.S.-Israeli Attacks. How Will Dow Jones Futures React?

AAPL

Investor's Business Daily

|

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 |

Trump Says Khamenei Likely Killed In U.S.-Israeli Attacks On Iran. How Will Dow Jones Futures React?

AAPL

Investor's Business Daily

|

| Feb-28 | |

| Feb-28 | |

| Feb-28 | |

| Feb-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite