|

|

|

|

|||||

|

|

|

Lucid Group, Inc. LCID shares have been trending lower over the past month. Shares of the electric vehicle (EV) startup have plunged 22.7% over the past month, underperforming the Zacks Automotive - Domestic industry’s growth of 0.8%.

Lucid has also underperformed industry peers, including Rivian Automotive, Inc. RIVN and Tesla, Inc. TSLA. Rivian’s shares have lost 10.7%, while Tesla’s shares have returned 0.6%.

Lucid reported a quarterly loss of 28 cents per share in the second quarter of 2025, narrower than the loss of 29 cents per share incurred in the year-ago period. It posted revenues of $259.4 million in the quarter, which rose from $201 million posted in the year-ago period.

The automaker delivered 3,309 vehicles in the second quarter of 2025, which rose 38% year over year, marking its sixth consecutive quarter of record deliveries. However, in the second quarter of 2025, Lucid’s rivals, Rivian and Tesla, reported a year-over-year decline in deliveries. Rivian delivered 10,661 vehicles, down from 13,790 units in the same period last year, marking two consecutive quarters of year-over-year decline, while Tesla recorded a 13.4% decline in deliveries.

Lucid expects deliveries to ramp up throughout 2027, driven by the production of the midsize platform scheduled to begin in late 2026. The midsize platform, which is designed to underpin a more affordable line of vehicles compared to its luxury-centric models like the Air and Gravity, presents a key opportunity for the company to expand its addressable market.

The company is actively pursuing partnerships that go beyond selling or licensing its leading EV technology. On July 17, the company announced a major collaboration with Uber Technologies, Inc. UBER and Nuro to develop a next-generation premium robotaxi for Uber’s ride-hailing platform. The project combines Lucid Gravity’s advanced software-defined vehicle architecture, Nuro’s proven Level 4 autonomous driving system, and Uber’s global network and fleet management to create a fully integrated service designed for comfort, safety and scalability. Per the deal, Uber will invest $300 million in Lucid, which is subject to regulatory approval, and deploy at least 20,000 Lucid Gravity vehicles with Nuro autonomy over six years in multiple global markets, starting late next year.

Encouragingly, LCID reaffirmed its commitment to U.S.-based manufacturing to counter the tariff impact and other geopolitical issues. For instance, a couple of months back, it announced a preliminary agreement with Graphite One to source natural and synthetic graphite domestically starting in 2028, which complemented its existing nonbinding supply agreement signed in April 2024.

Lucid has also partnered with Alaska Energy Metals, Electric Metals USA and RecycLiCo to enhance its supply chain. The company will obtain nickel from Alaska Energy Metals to boost vehicle range, extend battery life and reduce dependence on metals like cobalt. Manganese from Electric Metals will support the development of long-range, high-performance EVs while maintaining battery and passenger safety. Collaboration with RecycLiCo, a critical minerals refining firm, will aid Lucid’s energy storage efforts, promote responsible supply chains and advance the push for increased domestic sourcing of essential materials.

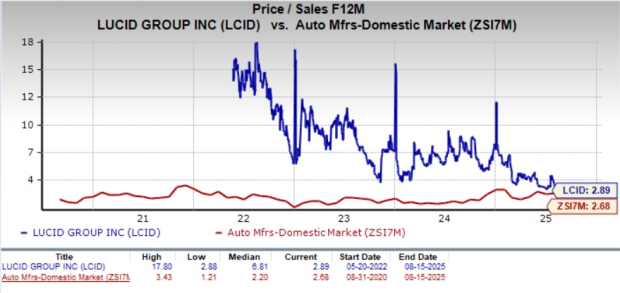

From a valuation standpoint, Lucid appears relatively overvalued. The stock trades at a forward price-to-sales (P/S) ratio of 2.89, above the industry’s 2.68.

The Zacks Consensus Estimate for LCID’s 2025 sales and earnings indicates year-over-year growth of 67.8% and 25.6%, respectively. The Zacks Consensus Estimate for 2025 and 2026 EPS has moved down a penny each in the past 30 days.

Despite all the positives, its stretched balance sheet and lowered output forecast are raising concerns. As of June 30, 2025, Lucid had long-term debt of $2.04 billion, which rose from $2 billion as of Dec. 31, 2024. Its long-term debt to capital ratio is 0.63, higher than the industry’s 0.4.

The company lowered its annual production forecast for 2025 from 20,000 units to a range of 18,000-20,000 units amid tariff-related headwind. Also, despite significant cost-cutting and supply chain adjustments, the company still expects tariff-related headwinds to hurt full-year 2025 profit margins.

Given this mix of factors, new investors shouldn’t rush into buying shares; existing shareholders might retain their holdings.

LCID carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 4 hours |

Tesla Autopilot under scrutiny after crash involving 49ers coach Kyle Shanahan

TSLA

Yahoo Finance Video

|

| 5 hours | |

| 5 hours | |

| 9 hours | |

| 11 hours | |

| 12 hours | |

| 13 hours | |

| 14 hours | |

| 14 hours | |

| 15 hours | |

| 16 hours | |

| 20 hours | |

| Aug-09 | |

| Aug-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite