|

|

|

|

|||||

|

|

|

The 2025 Q2 earnings season continues to slowly wind down, with this week’s docket primarily dominated by retail. The period has been resilient, with earnings growth remaining strong and a strong number of companies exceeding quarterly expectations.

Notably, expectations for the current period (2025 Q3) have also inched higher over recent months, a key item to keep in mind as we wrap up the Q2 cycle.

But before we wrap up anything, two retail heavyweights – Target TGT and Walmart WMT – are headlining the docket for retail companies this week.

Walmart’s outperformance relative to Target has been notable, outpacing it over the last several years, while Target has struggled in the post-COVID era. This development is illustrated in the chart below.

Let’s take a closer look at how each stacks up heading into their releases.

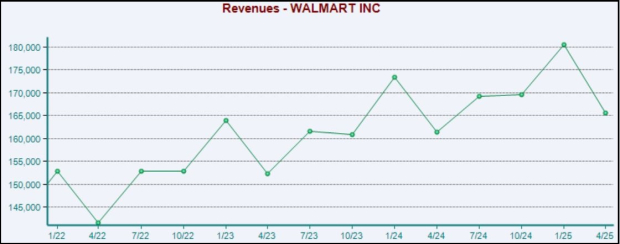

Walmart has been firing on all cylinders over the last several years, not only able to see strong growth thanks to its digital efforts but also benefiting from its more ‘staply’ mix of products. Consumers often trade down to WMT in times of stress, helping insulate it and providing a consistent level of demand.

Concerning its success within its digital efforts, Global eCommerce sales grew 22% YoY throughout its latest quarter, continuing the recent momentum nicely. Consumers have increasingly opted to pick up their groceries rather than shop, with its online marketplace also easy to use.

Additionally, Walmart US comparable store sales were up a strong 4.5%, a key metric for retailers. For the upcoming release, the Zacks Consensus estimate for US comparable store sales (ex-fuel) stands at 4.2%, alluding to continued momentum.

As shown below, WMT has regularly positively surprised on the metric, stringing together six consecutive beats.

Analysts have primarily been silent concerning their top and bottom line revisions for the quarter, with WMT expected to see 9% EPS growth on 3.7% higher sales. While the company hasn’t seen a flurry of upward revisions, the stability of the trends over recent months is a positive takeaway.

Below is a chart illustrating the company’s sales on a quarterly basis.

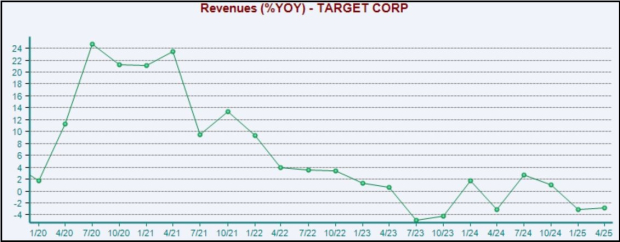

Quarterly results from Target have regularly disappointed over recent years, with the company’s more ‘discretionary’ inventory being a major thorn in the side in the post-COVID era. Comparable store sales decreased 3.8% YoY throughout its latest period, with overall sales also down 2.8%.

We expect TGT’s comparable store sales to decline 2.9% year-over-year, with the company unable to chain together positive beats on the metric over the last six periods.

While its retail stores may not be seeing growth, its digital efforts certainly can’t get overlooked. Digital comparable sales grew 4.7% YoY in its latest period, paired with a 36% increase in same-day delivery through Target Circle 360.

As we can see below, the company’s sales growth rates exploded during the COVID era, when consumers were spending on more discretionary items, but that trend has since subsided considerably. Target’s smaller mix of 'staply' products hasn’t been enough to offset the negative effects, also explaining the poor price action over recent years.

Please note that the chart below tracks the YoY % change in sales.

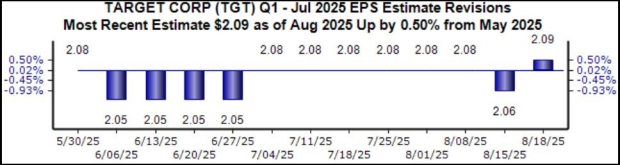

Still, the EPS outlook for the period is constructive and stable, as shown below. Given the several-year-long stretch of poor price action, the worst could be soon ‘behind’ Target, though that has remained the hope for several periods now.

Guidance will be the key hurdle for TGT to clear, though it’s worth noting that shares are already down more than 50% from their 2021 highs. Any sign of a turnaround concerning its discretionary merchandise would likely be enough to scare the bears away.

Bottom Line

Both Target TGT and Walmart WMT are titans in the retail space, with performance over recent years heavily skewed in favor of WMT.

TGT’s more discretionary merchandise mix has been an issue in the post-COVID era, whereas WMT’s more ‘staply’ mix has insulated it nicely, also providing consistent demand.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour |

Estée Lauder Files Lawsuit Against Walmart Alleging Sales of Counterfeit Products

WMT

The Wall Street Journal

|

| 1 hour |

Estee Lauder Files Lawsuit Against Walmart Alleging Sales of Counterfeit Products

WMT

The Wall Street Journal

|

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite