|

|

|

|

|||||

|

|

|

American Express Company AXP has rewarded investors handsomely, gaining 24.3% over the past year, outpacing the S&P 500’s 15.6% climb and the broader industry’s 14.5% rise. Still, its larger peers did even better — Visa Inc. V jumped 27.7% and Mastercard Incorporated MA rose 25.1%.

AmEx’s resilience reflects the strength of its premium brand, even in a choppy macro environment. Its affluent, high-spending customer base and consistent earnings have provided a buffer against broader volatility. As one of Berkshire Hathaway’s longest-standing holdings, AmEx continues to enjoy a reputation as a quality, blue-chip name.

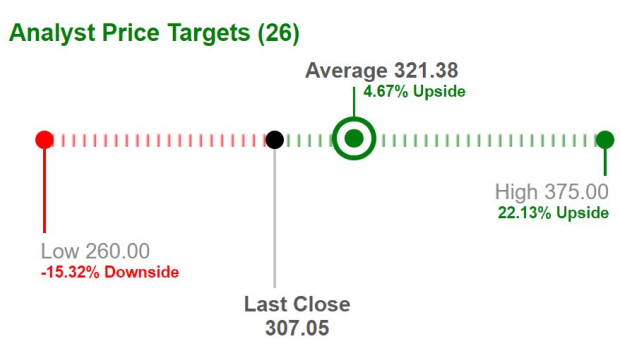

AXP currently trades below the Wall Street average price target of $321.38, suggesting only a 4.7% upside from current levels.

But the key question remains: Is there room for more growth? Even with its strong fundamentals, AmEx is not fully immune to global headwinds, ranging from tariff uncertainty and credit risk shifts to changing consumer spending trends.

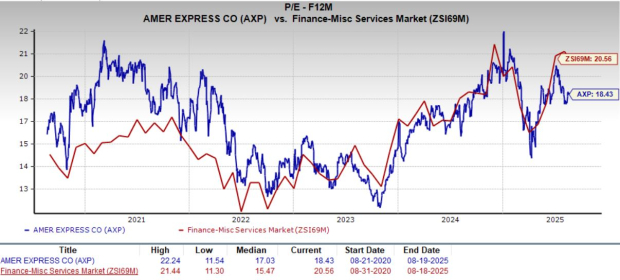

On the surface, AmEx looks attractively priced. It currently trades at a forward price-to-earnings (P/E) ratio of 18.43X, below the industry average of 20.56X. Yet, that figure sits above its five-year median of 17.03X, making it slightly expensive by its own historical yardstick. It carries a Value Score of B.

By comparison, Visa and Mastercard command significantly higher multiples, with forward P/E ratios of 27.01X and 32.50X, respectively, reflecting their more scalable, lower-risk business models.To fully grasp AmEx’s potential, however, we need to unpack how its business actually works.

American Express often gets lumped in with traditional credit card companies, but its model is distinct. Unlike Visa and Mastercard, which operate solely as networks, AmEx is both a card issuer and a bank. That means it earns money not only from transaction fees but also from interest on outstanding balances.

This closed-loop structure offers advantages, even in high-interest-rate environments. While higher rates can curb spending, they also lift the company’s interest income. Its second-quarter interest income of $6.3 billion increased 8% year over year.

At the same time, AmEx’s premium customer base remains a stabilizing force. Even as many U.S. households feel the squeeze of inflation and tighter credit, its affluent cardholders continue to spend on perks, rewards and lifestyle benefits. That strength showed up in the numbers, with network volumes rising 7% to $472 billion in the second quarter, fueled by resilient U.S. consumer spending.

AmEx’s business model hinges on the strength of its balance sheet, since it needs to finance cardholder loans, absorb credit risk and maintain regulatory capital. At the second-quarter end, the company held $57.9 billion in cash and cash equivalents and just $1.5 billion in short-term borrowing. Total assets of $295.6 billion rose from $271.5 billion at 2024-end.Its net debt-to-capital of 1.91% is significantly lower than the industry average of 16.11%.

This balance sheet strength enables it to take shareholder-friendly moves. In 2024, AmEx returned $7.9 billion via dividends and buybacks, with another $3.3 billion returned in the first half of 2025 alone.

Analysts remain bullish.The Zacks Consensus Estimate for AmEx’s 2025 earnings indicates a 14.3% year-over-year increase, while 2026 earnings are expected to grow 13.7%. Both the earnings estimates witnessed several upward revisions in the past month. Also, revenue estimates for 2025 and 2026 indicate growth of 8.3% and 8.1%, respectively.

AXP has a solid track record of surpassing earnings expectations, delivering an average surprise of 4.6% over the past four quarters.

American Express Company price-consensus-eps-surprise-chart | American Express Company Quote

Even with its strengths, AmEx faces some clear risks. The company is more exposed to travel and entertainment spending than some of its peers, a category that tends to fall sharply in downturns. Much of its recent momentum has come from Millennials and Gen Z, whose spending habits are more discretionary. That leaves AmEx somewhat vulnerable, though its affluent core customers are generally more resilient to economic shocks.

Another concern is the steady climb in operating costs. Expenses jumped 22% in 2021, 24% in 2022, 10% in 2023, 6% in 2024, and another 12% in the first half of 2025. While rising engagement explains part of the trend, it still squeezes margins. On top of that, AmEx carries meaningful consumer and small-business credit risk. A slowdown could push up delinquencies and loss provisions, weighing on earnings.

Finally, American Express remains more domestically focused than Visa and Mastercard, both of which have aggressively expanded their global digital payment ecosystems. AmEx’s reliance on lending and card volume growth may limit its flexibility in adapting to emerging non-card payment trends.

American Express has delivered impressive returns over the past year, underpinned by a resilient brand, a premium customer base and a strong balance sheet. Its dual role as both a card issuer and a network operator gives it unique advantages, particularly in an elevated rate environment, and earnings momentum remains solid with upward estimate revisions.

That said, the company faces meaningful near-term challenges. Rising expenses, exposure to discretionary categories like travel and entertainment, and heavy reliance on credit risk make it more vulnerable than peers such as Visa and Mastercard, which benefit from more scalable, globally diversified models. Valuation also suggests limited near-term upside, with shares trading close to Wall Street’s price target.

Given the mix of solid fundamentals but heightened risks and modest upside potential, American Express currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 10 hours | |

| 11 hours | |

| May-21 | |

| May-21 | |

| May-21 | |

| May-21 | |

| May-21 | |

| May-21 | |

| May-20 | |

| May-20 | |

| May-20 | |

| May-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite