|

|

|

|

|||||

|

|

|

Carnival Corporation & plc (CCL) continues to anchor its growth strategy on fleet expansion, with several new ships entering service as part of the modernization efforts. These additions are designed to enhance guest experience, improve fuel efficiency and capture rising demand across both North America and Europe. Management highlighted that the latest ships are delivering strong booking trends and higher onboard spending, positioning them as valuable assets in driving incremental revenue growth.

However, the bigger question for investors is whether these gains can translate into sustainable profitability. While the company reported record revenues and healthy occupancy rates in second-quarter 2025, the financial lift from new ships comes with elevated operating and financing costs. Carnival has been working to offset these pressures through cost discipline, including more efficient fuel usage and leveraging scale advantages. Early indications show margins benefiting from lower unit costs on newer vessels compared with older ships.

At the same time, broader industry tailwinds, such as resilient global travel demand and consumers prioritizing experiences, support Carnival’s expansion strategy. Still, headwinds persist, including fluctuating fuel prices, inflationary pressures and the need to balance debt reduction with capital investments.

In essence, Carnival’s new ship deliveries are bolstering growth and efficiency, but the true test lies in sustaining profitability as economic conditions shift. If management continues to execute on cost controls and capitalize on strong demand, these fleet additions could prove to be more than just short-term boosts, laying the foundation for long-term shareholder value.

Carnival Corporation’s push for profitability through new ship additions is mirrored by its closest rivals, Royal Caribbean Group (RCL) and Norwegian Cruise Line Holdings (NCLH). Royal Caribbean has leaned heavily on innovative mega-ships like the Icon of the Seas, which deliver strong pricing power and unmatched onboard revenue opportunities. Its strategy centers on creating destination-style ships that encourage longer stays and higher per-guest spending, helping to lift margins despite higher upfront costs.

Norwegian, on the other hand, is focused on a more measured fleet expansion. The company continues to introduce vessels under its Prima Class, which emphasize premium guest experiences and sustainability features. Norwegian’s smaller but more targeted fleet growth allows it to balance capital deployment with debt management.

Both competitors highlight the broader industry trend: leveraging new, efficient ships to capture demand and lift profitability. Carnival’s ability to keep pace will determine its competitive positioning.

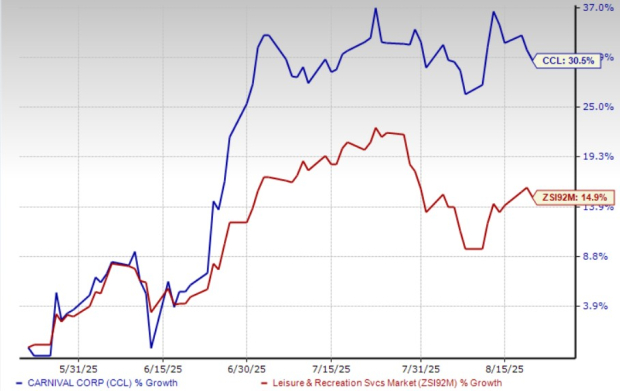

Shares of Carnival have gained 30.5% in the past three months compared with the industry’s growth of 14.9%.

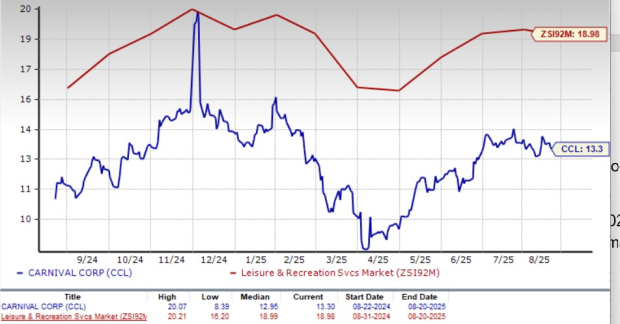

From a valuation standpoint, CCL trades at a forward price-to-earnings ratio of 13.3X, significantly below the industry’s average of 18.98X.

The Zacks Consensus Estimate for CCL’s fiscal 2025 and 2026 earnings implies a year-over-year uptick of 40.9% and 13.8%, respectively. The EPS estimates for fiscal 2025 have increased in the past 30 days.

CCL currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite