|

|

|

|

|||||

|

|

|

Amazon AMZN and Shopify SHOP represent two distinct yet compelling approaches to capturing the e-commerce growth opportunity. Amazon operates as a vertically integrated e-commerce giant with diverse revenue streams spanning retail, cloud computing, and digital services, while Shopify focuses on enabling merchants of all sizes to build and scale their online businesses through its comprehensive platform-as-a-service model.

The comparison between these e-commerce leaders becomes particularly relevant in today's market environment, where investors are increasingly scrutinizing growth stocks for sustainable profitability and operational efficiency. Recent earnings results from both companies have highlighted their resilience amid economic uncertainties, including tariff concerns and shifting consumer spending patterns.

Let's delve deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

Amazon's investment proposition remains compelling, anchored by its unparalleled scale and diversified revenue streams that provide multiple avenues for sustained growth. The company's second-quarter earnings demonstrated robust performance with net sales increasing 13% to $167.7 billion, while operating income surged 31% year over year to $19.2 billion, showcasing management's successful focus on operational efficiency. Amazon Web Services (“AWS”) continues to be a significant profit driver with revenues of $30.87 billion in the second quarter, up 18% year over year, while maintaining its leadership position in the rapidly expanding cloud infrastructure market.

The company's advertising business emerged as a particularly bright spot, with ad revenues growing 23% year over year to $15.69 billion in the second quarter, beating estimates and positioning Amazon as the third largest digital advertising platform globally. This high-margin business segment benefits from Amazon's vast customer data and shopping intent signals, creating a defensible competitive moat.

Recent strategic initiatives include the expansion of same-day and next-day delivery to tens of millions of customers in over 4,000 smaller cities and rural communities, the launch of generative AI tools to enhance shopping experiences, and the introduction of Alexa+, a next-generation AI assistant. Amazon's financial guidance for the third quarter projects net sales between $174 billion and $179.5 billion, representing 10-13% growth, while the company continues its massive $100 billion AI investment commitment.

The Zacks Consensus Estimate for 2025 earnings is pegged at $6.7 per share, which indicates a jump of 21.16% from the year-ago period.

Amazon.com, Inc. price-consensus-chart | Amazon.com, Inc. Quote

Shopify's investment narrative centers on its role as the backbone of modern e-commerce, empowering merchants to compete effectively in an increasingly digital marketplace. The company delivered solid second-quarter results with revenues surging 31% year over year to $2.68 billion, significantly beating analyst expectations, while gross merchandise volume (GMV) increased 31% to $74.75 billion. Shopify's strategic focus on its core platform capabilities after divesting its logistics business has yielded impressive results, with the company achieving eight consecutive quarters of double-digit free cash flow margins, including a 16% free cash flow margin in the second quarter.

International expansion represents a significant growth opportunity for Shopify, with international GMV growing 42% year over year, particularly driven by European markets where the company has signed major brands like Starbucks, Canada Goose, and Burton Snowboards. The company's B2B segment showed remarkable momentum with GMV increasing 101% year over year, while Shop Pay GMV grew 65% to $27 billion as the user base more than doubled over the past 2.5 years. Shopify's payments penetration reached 64% in the second quarter, up from 61% the previous year, driving higher-margin revenue streams. Recent product innovations demonstrate Shopify's commitment to staying ahead of commerce trends, including the launch of AI-driven products like Catalog, Universal Cart, and Checkout Kit, which enhance agentic commerce capabilities. Microsoft's Copilot integration with Checkout Kit validates Shopify's technological leadership. However, challenges include slowing monthly recurring revenue growth due to longer paid trials and profitability pressures from higher operating expenses.

The Zacks Consensus Estimate for 2025 earnings is pegged at $1.44 per share, which indicates an increase of 10.77% from the year-ago period.

Shopify Inc. price-consensus-chart | Shopify Inc. Quote

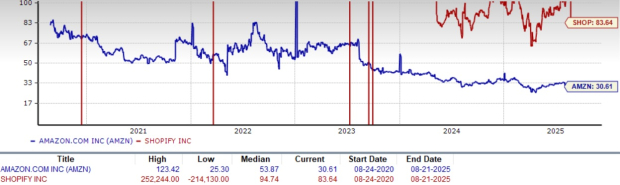

Both Amazon and Shopify command premium valuations, but Amazon presents a more attractive risk-adjusted valuation profile. Amazon’s current forward P/E ratio of 30.61x appears reasonable given the company's diversified growth drivers and strong free cash flow generation capabilities. Shopify trades at a current P/E ratio exceeding 83.64x, reflecting high growth expectations that require consistent execution.

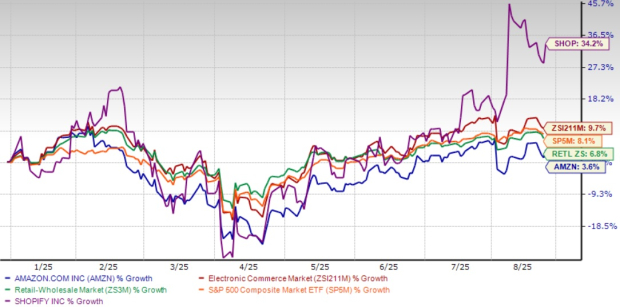

Year-to-date 2025 performance shows Amazon up 3.6% while maintaining relative stability, whereas Shopify has demonstrated higher volatility with significant gains following strong earnings reports. Amazon's more mature business model generates substantial free cash flow, providing flexibility for capital allocation, while Shopify's reinvestment requirements may pressure near-term profitability metrics.

Amazon emerges as the more compelling investment opportunity due to its superior diversification, stronger financial foundation, and more attractive valuation. The company's multiple growth drivers across e-commerce, cloud computing, and advertising provide greater resilience while offering substantial upside potential from AI initiatives. Amazon's operational scale advantages and cash generation capabilities position it advantageously for sustained performance. Investors should track Amazon stock for attractive entry points given its superior risk-adjusted return potential, while those interested in Shopify should wait for better entry opportunities as current valuation appears stretched. Both AMZN and SHOP carry a Zacks Rank #3 (Hold) each at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

Marketplaces Are the Next Frontier in Publisher Deals With AI Companies

AMZN

The Wall Street Journal

|

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite