|

|

|

|

|||||

|

|

|

Chipotle's traffic and per-restaurant sales are declining.

The company still trades at a high P/E ratio.

If comparable store sales growth recovers, the stock will likely do well going forward.

For years, Chipotle (NYSE: CMG) has been considered a bulletproof stock. After getting past its previous food health scares, the fast casual Mexican chain has steadily grown its unit count and per store sales, driving earnings higher and higher. Investors believed there was a huge runway for unit growth, both in the United States and internationally, and gave Chipotle stock a premium valuation because of it.

Chinks may finally be showing up in Chipotle's armor. Last quarter, the company reported a sharp drop in its per-restaurant sales, which inspired investors to panic sell out of the stock. Chipotle is now down 28% year-to-date (YTD), severely underperforming the market indices in 2025. Let's dive into the current problems with Chipotle and decide whether this is a short-term blip and buying opportunity or a long-term concern for investors.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Chipotle reported its latest quarterly earnings in July. Revenue grew 3% in the period to $3.1 billion, driven by more restaurant location openings. However, this was not the metric investors were focused on. What alarmed Wall Street was a 4% decline in same-store sales -- measuring year-over-year revenue growth from existing restaurants -- driven by customer traffic falling off a cliff. The company has even been implementing price increases, meaning that traffic declined even more than the 4% year-over-year comparable store sales decrease.

Comparable store sales growth is vital for a restaurant chain. If it cannot match or outpace inflation that is currently running at 3%-5% across various cost inputs, then it is going to see declining profit margins. That is exactly what happened to Chipotle in the quarter. Its restaurant-level operating margin was 27.4%, down from 28.9% a year ago.

What is driving these traffic declines? It is hard to pinpoint an exact reason, which is providing even more uncertainty for shareholders. Some may point to increased unemployment for young professionals, who have a higher share of spending at fast casual chains like Chipotle compared to older generations. It also could be broad-based trading down to cheaper options for consumers, which has helped other chains such as Domino's Pizza and McDonald's.

Regardless, a 4% same-store sales decline is wrecking Chipotle's profits. If traffic problems do not get fixed, the company's profits will keep sliding lower and lower.

Image source: Getty Images.

Another issue with Chipotle stock was its high starting earnings multiple. Chipotle had a price-to-earnings ratio (P/E) well above 50 at the end of 2024. This implied high expectations for future earnings growth, which would be driven by consistently strong comparable store sales growth.

These high expectations led to a collapsing Chipotle stock price after posting its recent comparable store sales figure. Today, Chipotle trades at a trailing P/E ratio of 38.5, which implies less future earnings growth but is still a premium to the S&P 500 Index.

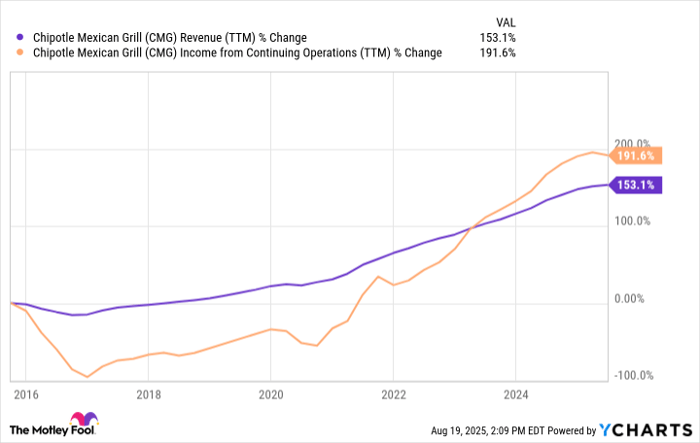

CMG Revenue (TTM) data by YCharts

At the end of last quarter, Chipotle had 3,839 company-owned restaurant locations. It has plenty of room to expand unit count around the United States and globally, at least if you compare it to other restaurant brands. With average annual restaurant sales of over $3 million, each new location that Chipotle adds can push revenue higher and higher. This is why the company's revenue is up 153% in the last 10 years.

Income from operations has grown even quicker at close to 200% over 10 years due to strong comparable store sales growth. If Chipotle can reverse these recent same-store sale declines and get them back at or above inflation, Chipotle stock will likely perform well even if you buy it at the current P/E ratio of 38.5. However, if the traffic and per store sales keep declining, the stock has a lot of room to fall further from here.

Before you buy stock in Chipotle Mexican Grill, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Chipotle Mexican Grill wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $650,499!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,072,543!*

Now, it’s worth noting Stock Advisor’s total average return is 1,045% — a market-crushing outperformance compared to 182% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 18, 2025

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chipotle Mexican Grill and Domino's Pizza. The Motley Fool recommends the following options: short September 2025 $60 calls on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

| 4 hours | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 | |

| Feb-09 |

Chipotle's in a funk, Taco Bell cannot be stopped, and snacks are all the rage

CMG

Nation's Restaurant News

|

| Feb-09 | |

| Feb-08 | |

| Feb-08 | |

| Feb-06 | |

| Feb-06 | |

| Feb-06 | |

| Feb-06 | |

| Feb-05 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite