|

|

|

|

|||||

|

|

|

While Target TGT and Walmart WMT both posted mixed Q2 results this week, the two retail giants disclosed different stories regarding their current growth and expansion.

However, this story has been consistent over the last year, so it’s no spoiler alert that Walmart came out on top as the company is riding a wave of digital strength thanks to its growing e-commerce presence.

Walmart’s operations are also thriving from its grocery business, with Target being more exposed to weaker demand for discretionary items, being in a transitional phase amid leadership changes and shifting consumer behavior.

Reporting Q2 earnings of $0.68 a share on Thursday, Walmart’s profit was dented by unexpected legal expenses, missing EPS expectations of $0.73. Still, Walmart’s earnings were up from $0.67 a share in the prior year quarter, with Q2 sales of $177.4 billion rising nearly 5% year over year and comfortably eclipsing estimates of $175.51 billion.

Furthermore, Walmart has remained bullish on its outlook, especially in AI and digital transformation, seeing a 25% surge in global E-commerce sales during Q2 and a 46% spike in advertising revenue. Walmart’s U.S. comparable sales also helped drive its growth, rising over 4% driven by grocery and health & wellness segment sales. Ending a streak of surpassing the Zacks EPS Consensus in six of the previous quarters, Walmart has still posted an average earnings surprise of 2.79% over its last four quarterly reports.

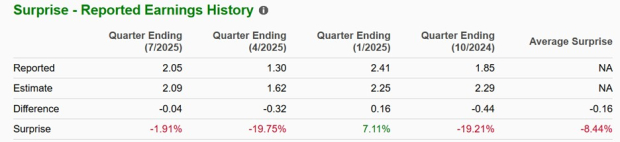

Similarly, Target exceeded Q2 sales estimates on Wednesday but missed earnings expectations. Target’s Q2 sales of $25.11 billion were down from $25.45 billion a year ago but edged estimates of $24.91 billion. That said, Target’s Q2 EPS of $2.05 came up short of expectations of $2.09 and fell 20% from $2.57 a share in the prior period.

Notably, Target saw a 4% increase in digital sales led by same-day delivery and drive-up orders, but experienced a 2% decline in comparable sales with store traffic down more than 1%. Target has now missed the Zacks EPS Consensus in three of its last four quarterly reports, with an average earnings surprise of -8.44%.

Reflecting strong performance in its grocery, health & wellness, and e-commerce segments, Walmart raised its guidance for full-year revenue growth to between 3.75%-4.75%, up from a previous range of 3%-4%. Walmart also raised its full-year adjusted EPS guidance for its current fiscal 2026 to $2.52-$2.62 from $2.43-$2.55, with its annual earnings at $2.51 per share in its FY25.

As for Target, it maintained its full-year outlook for its current FY26, still expecting a low-single-digit decline in full-year sales, with adjusted EPS between $7.00-9.00 compared to earnings of $8.86 per share in its FY25.

With Target planning to recalibrate its operational strategy, CEO Brian Cornell announced he will step down in February after an 11-year tenure and will be transitioning to the role of executive chair of the board. Cornell will be replaced by Target’s current COO, Michael Fiddelke, who has been with the company for 20 years.

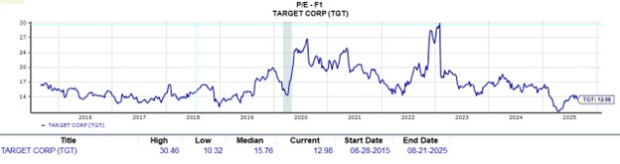

Although analysts have cited Target’s inability to keep up with consumer trends as the main culprit for losing ground to competitors like Walmart and Amazon AMZN, the omnichannel retailer's valuation has been hard to overlook at 12X forward earnings. In contrast, Walmart and Amazon stock trade at more than 30X forward earnings, with the S&P 500’s average at 24X.

Despite being in a down period, in terms of its growth and relevance, Target's stock is also trading at a nice discount to its decade-long median of 15X forward earnings and trades well under the preferred level of less than 2X sales.

Target’s very generous annual dividend yield of 4.7% also stands out as opposed to Walmart’s 0.96%. Reassuringly, Target and Walmart both have reliable payouts, being classified as Dividend Kings, raising their dividends for at least 50 consecutive years.

Walmart’s operational performance has a clear edge over Target right now, but regarding their stocks, both offer different advantages that investors may prefer depending on their portfolio strategy. To that point, income and value investors may still prefer Target’s stock despite its challenges, while those focused on growth and short-term stock performance may be better suited with Walmart.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite