|

|

|

|

|||||

|

|

|

Revvity, Inc. RVTY is well-positioned for growth in the coming quarters, thanks to its strong product portfolio. The optimism, led by its solid fourth-quarter 2024 performance and focus on artificial intelligence (AI), is expected to contribute further. Headwinds resulting from foreign exchange volatility and integration risks are major downsides.

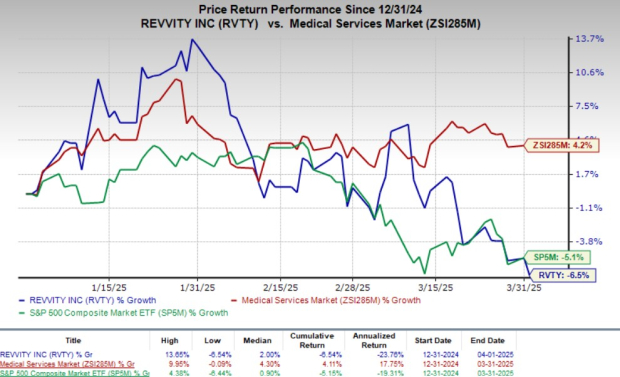

This Zacks Rank #3 (Hold) company’s shares have lost 6.5% so far this year against the industry’s 4% growth. The S&P 500 has decreased 5.1% during the same time frame.

The renowned provider of health science solutions has a market capitalization of $12.71 billion. It projects 6.1% growth over the next five years and expects to witness continued improvement in its business going further. Revvity’s earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, delivering an average surprise of 7.48%.

Let’s delve deeper.

Focus on AI: We are upbeat about the trend of healthcare companies using AI for quite some time now. Management at Revvity introduced PKeye Workflow Monitor, a cloud-based platform allowing laboratory personnel to remotely manage and monitor the company’s instruments and workflows in real-time.

Revvity also introduced Signals Research Suite, a complete cloud-based solution used by Amazon Web Services.

Promising Product Portfolio: We are optimistic about Revvity’s portfolio, which provides a comprehensive suite of scientific informatics and software solutions that aggregate data into actionable insights in an automated and scalable manner. During 2024, the company’s software and informatics division, Revvity Signals Software, demonstrated strong growth, a trend that is likely to continue in 2025 and beyond on the back of new offerings.

In fourth-quarter 2024, Revvity launched new software enhancements within its Signals Software platform, focusing on AI-driven analytics and cloud-based solutions. These innovations improved data interpretation, workflow automation, and scalability for biopharma and research customers. The company also introduced advanced integration features, making it easier for users to incorporate Signals Software into existing laboratory workflows.

With a growing emphasis on AI and cloud technology, these updates strengthened Revvity’s Informatics segment and contributed to recurring revenue growth. The expansion of Signals Software underscored the company’s commitment to digital transformation and positioned it as a key player in data-driven life sciences research.

Revvity has bolstered its innovation strategy with the launch of groundbreaking products in diagnostics and AI. PhenoLOGIC AI, an advanced tool for high-content screening, enhances image analysis and accelerates live cell data insights using pretrained AI models.

Meanwhile, the Revvity transcribed AI service automates handwritten data transcription in clinical labs, boosting workflow efficiency by 40%. The service saw strong demand from biopharma companies during the fourth quarter.

Additionally, EUROIMMUN's genotyping solution for Alzheimer’s therapies positions Revvity at the forefront of personalized medicine in Europe. These innovations demonstrate Revvity’s agility in meeting emerging healthcare needs and solidify its leadership in leveraging AI for transformative medical advancements.

Robust Q4 Results:In fourth-quarter 2024, Revvity experienced strong performance across several key business franchises. The Signals Software segment within Informatics saw robust recurring revenue growth, driven by increasing adoption of AI-driven analytics and cloud-based solutions in biopharma research. The Reproductive Health business continued to perform well, with steady demand for prenatal and neonatal screening solutions.

Additionally, the Biopharma Solutions segment within Life Sciences benefited from strong demand for drug discovery and development tools. The Applied Genomics business also demonstrated positive momentum, driven by increasing interest in molecular diagnostics and research applications. These franchises were key contributors to Revvity’s overall performance.

Foreign Exchange Volatility: Increasing exposure to international markets enhances the risk of foreign exchange volatility. Fluctuations in currency exchange rates can adversely impact the company’s international sales. Due to sluggish Asian growth, especially in China, future revenues and earnings are likely to be affected if RVTY does not hedge against exposure to such fluctuations. During the fourth quarter, sales growth reflected unfavorable impact of 120 basis points due to foreign exchange volatility.

Immunodiagnostics Franchise Faces Soft Performance: During the fourth quarter, Revvity’s Immunodiagnostics franchise faced several challenges that affected its overall performance. One of the primary issues was weaker demand in certain end markets, particularly in China, where market conditions and regulatory dynamics created headwinds.

Additionally, the franchise experienced pricing pressures and competitive challenges, making it difficult to maintain growth in some regions. Slower-than-expected recovery in routine testing volumes also affected sales. Despite these challenges, Revvity remains focused on portfolio expansion and geographic diversification to drive future growth. The company is investing in new product development and strategic initiatives to strengthen its position in the immunodiagnostics market.

Revvity Inc. price | Revvity Inc. Quote

Revvity has been witnessing a stable estimate revision trend for 2025. Over the past 30 days, the Zacks Consensus Estimate for earnings per share (EPS) has remained unchanged at $4.94.

The Zacks Consensus Estimate for first-quarter 2025 revenues is pegged at $662.7 million, indicating a 2% improvement from the year-ago reported number. The Zacks Consensus Estimate for EPS is pinned at 95 cents, implying a year-over-year decline of 3.1%.

Some better-ranked stocks in the broader medical space are Masimo MASI, Cencora, Inc. COR and Boston Scientific Corporation BSX.

Masimo, sporting a Zacks Rank #1 (Strong Buy) at present, has an estimated growth rate of 20% for 2025. MASI’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 14.41%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Masimo’s shares have gained 1.4% against the industry’s 4.5% decline so far this year.

Cencora, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 12.1%. COR’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 4.9%.

Cencora’s shares have gained 23.5% compared with the industry’s 4.2% improvement year to date.

Boston Scientific, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 13.3%. BSX’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 8.3%.

Boston Scientific’s shares have rallied 13.4% compared with the industry’s 7.6% growth so far this year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite