|

|

|

|

|||||

|

|

|

HubSpot, Inc. HUBS is witnessing solid user engagement in its customer relationship management (CRM) platform, which is driving subscription-based revenues. In the second quarter, Subscription revenues rose to $744.5 million from $623.7 million, up 19% year over year. The figure surpassed the Zacks Consensus Estimate of $722.7 million. The company added more than 9,700 net new customers during the quarter, which increased the total customer count to 267,982, up 18% year over year.

HubSpot has significant scope in cross-selling its products to the existing customer base. The company’s pricing optimization strategy and its seat pricing model are driving customer additions.

HUBS has a vast user base that uses its products for free. Given the growing effectiveness of its inbound applications and an innovative product portfolio, many customers are upgrading their subscription and opting for pro products for marketing and sales functions. The seat pricing model lowers the barrier for customers to get started with HubSpot and mitigates pricing friction for upgrades.

The company is also integrating AI across its product suite and customer platform. Sales Hub seat upgrades increased 71% year over year during the second quarter. The growth is driven by solid adoption of leading-edge AI features such as deal intelligence and an AI-powered meeting assistant. Service hub seat upgrades were up 110% year over year.

In the CRM space, HubSpot faces competition from Salesforce, Inc. CRM, one of the world’s leading Customer Relationship Management companies. The company dominates the market due to its strong clientele. In the CRM business segment, Salesforce generated $9.3 billion in revenues from Subscription and Support services in the first quarter. Rapid digital transformation across industries and management’s approach of aligning its product offerings with evolving customer needs is a positive. Salesforce’s initiative to integrate AI across its portfolio will likely drive growth.

Microsoft Corporation MSFT is also seeing healthy demand trends in the Productivity & Business Processes segment, which includes the Office and Dynamics CRM businesses. In the June quarter, revenues from Microsoft’s Dynamic 365 surged 23% year over year. The Dynamic 365 is powered by Microsoft Copilot, which facilitates the generation of engaging content, key insights and summarizes customer experience. This significantly boosts the efficiency of customer service workers, enabling sellers to accurately identify and engage their target market.

HubSpot has declined 6% over the past year compared to the industry’s growth of 39.8%.

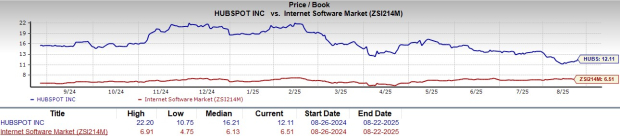

Going by the price/book ratio, the company's shares currently trade at 12.11 book value, higher than 6.51 of the industry average.

HUBS’ earnings estimate for 2025 and 2026 have improved 1.5% to $9.49 per share and 0.98% to $11.36 per share, respectively, over the past year.

HubSpot currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite