|

|

|

|

|||||

|

|

|

Tempus AI TEM and Butterfly Network BFLY both just reported their respective second-quarter 2025 results, which shed light on their AI-driven trajectories. Tempus AI continues to post rapid top-line expansion while leveraging its growing data ecosystem and clinical partnerships to reach closer to profitability. Butterfly Network, meanwhile, reported modest revenue growth as it works to scale adoption of its AI-driven handheld ultrasound platform and drive operating discipline. For investors, the choice is between Tempus’ high-growth precision medicine model and Butterfly’s turnaround-stage imaging platform.

Let's Delve Deeper:

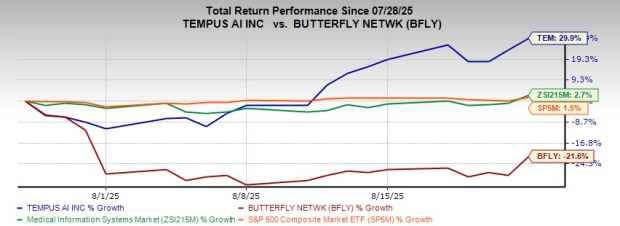

Over the past 30 days, shares of Tempus AI have surged 29.9% while Butterfly Network stock has declined 21.6%. Butterfly’s moderate top-line gains, continued cash burn and reliance on cost-cutting over meaningful revenue acceleration dampened investor confidence. Meanwhile, the broader Medical Info Systems industry hasgained 2.7% and the S&P 500 index has risen 1.5% during this period.

Building a Wide Moat, Profitability Within Reach: Tempus AI posted a strong second quarter of 2025, with revenues rising nearly 90% year over year, beating the Zacks Consensus Estimate by 5.12%, led by a 115% surge in Genomics from accelerating oncology and hereditary testing volumes and a 35.7% increase in high-margin Data and Services from AI-enabled data licensing. Gross profit jumped 158%, lifting adjusted gross margin to 62% despite a 32.2% rise in the cost of revenues (genomics, data and services). This breadth highlights how Tempus AI is building a wide moat across both clinical diagnostics and data-driven insights.

Adjusted EBITDA loss narrowed to just $5.6 million. Management’s raised guidance for $1.26 billion in 2025 revenues and $5 million adjusted EBITDA underscores a disciplined shift toward sustainable growth.

Innovation and Data Scale: Innovation is strengthening Tempus’ AI’s competitive moat, highlighted by the launch of the xM liquid biopsy, Ambry’s expanding role as a standard in hereditary testing and the growing integration of AI tools like Tempus Next and Tempus One into routine clinical practice. Alongside these advancements, Tempus’ scale in data and AI is becoming a structural advantage, with more than 40 million patient records connected and advanced foundation models now being trained on NVIDIA’s NVDA latest hardware. Strategic partnerships, such as the AstraZeneca AZN /Pathos AI collaboration, further demonstrate how Tempus AI’s data assets and AI capabilities combinedly is becoming essential to the pharmaceutical industry.

Tempus AI is still operating at a loss, with negative adjusted EBITDA in the second quarter of 2025. Costs are also climbing, with the cost of revenues rising 32.2% year over year, reflecting the heavy investments required to scale both genomics and data services. This reliance on continued expansion to offset expenses leaves Tempus vulnerable if testing volumes or data licensing growth were to slow.

Enterprise Momentum: Butterfly is gaining traction with large-scale deployments, including closing an enterprise-wide deal with one of the world’s top five health systems. This validates the scalability of its iQ3 handheld ultrasound and demonstrates confidence among major providers in Butterfly’s platform. Although sales cycles remain elongated, these large-scale wins create a foundation for repeatable, high-value contracts. At the same time, Compass AI, launching in the third quarter, signals Butterfly Network’s shift from hardware-led growth to a recurring, software-driven model. With features like voice automation and scan quality feedback, it is designed to boost productivity, positioning Butterfly to capture higher-margin, recurring revenue growth.

Expanding Horizons With HomeCare, Octiv, and Butterfly Garden: Butterfly’s HomeCare pilots have reduced heart failure readmissions, with a state-level rollout due in 2025 and nationwide expansion that could generate $40-$60 million annually from one customer. Octiv, its semiconductor and imaging platform, is attracting partners, including a generative AI company, creating new licensing opportunities. At the same time, Butterfly Garden is becoming a differentiator with new partners, three FDA-cleared AI apps, the upcoming HeartFocus launch, and collaborations like MSK VUE and ScanLab. Together, these initiatives extend ultrasound’s reach, drive integration in healthcare, and enhance customer stickiness.

Despite clear progress, Butterfly Network continues to face challenges that may temper near-term momentum. Sales cycles remain elongated, which could delay the conversion of enterprise wins into meaningful revenue. The HomeCare opportunity, while promising, is still in early pilot and rollout stages. Similarly, Octiv and Butterfly Garden are in formative phases, reliant on partner uptake, regulatory progress, and execution to deliver meaningful returns.

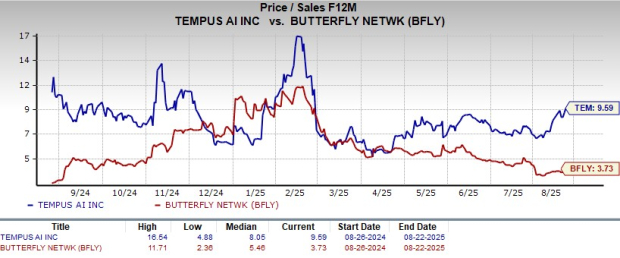

Tempus AI is trading at a forward 12-month price-to-sales (P/S) ratio of 9.59, above its median of 8.05 over the last year. Butterfly Network’s forward sales multiple sits at 3.73, below its last one-year median of 5.46. Meanwhile, TEM appears expensive when compared with the industry average of 6X. On the other hand, BFLY stays slightly discounted compared to the industry.

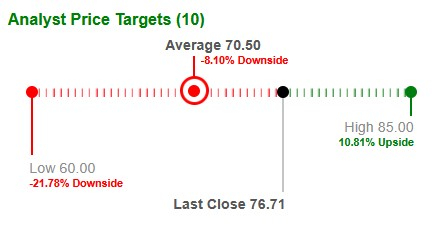

Based on short-term price targets offered by 10 analysts, TEM’s average price target represents a decline of 8.1% from the last closing price of $76.71.

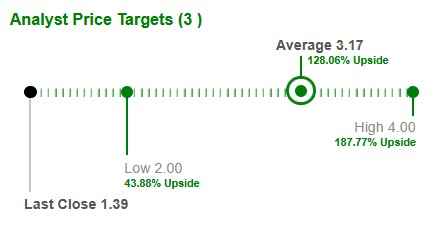

Based on short-term price targets offered by three analysts, BFLY’s average price target represents an increase of 128% from the last closing price of $1.39.

In summary, while Tempus AI continues to deliver impressive growth, margin expansion and product innovation, its premium valuation, ongoing losses, and rising costs justify a more cautious stance, aligning with its Zacks Rank #3 (Hold). Investors may want to wait for a more attractive entry point or clearer path to sustained profitability before adding exposure. By contrast, Butterfly Network — despite modest top-line progress and lingering execution risks — now trades at distressed levels with analyst targets implying significant upside potential. With a Zacks Rank #2 (Buy), the stock appears more compelling in the near term, offering investors a chance to capitalize on a turnaround story. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 9 hours | |

| 9 hours | |

| 10 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite