|

|

|

|

|||||

|

|

|

The data storage market is growing rapidly, fueled by cloud adoption, AI, IoT and Big Data, with rising demand for scalable, secure solutions like distributed file systems and object storage, further boosted by global data center expansions. Both Seagate Technology Holdings plc (STX) and Western Digital Corporation (WDC) are dominant players in the hard disk drive (HDD) and data storage industry, together controlling the vast majority of the HDD market.

Western Digital is a diverse storage company with a wide range of products, including traditional HDDs and NAND-based SSDs, serving both consumer and enterprise markets. Seagate, a major storage provider and direct competitor, is promoting growth through its Heat-Assisted Magnetic Recording (HAMR) technology, which enables higher areal density to meet the increasing storage demands of hyperscale data centers, AI training and edge environments.

Per a report from Mordor Intelligence, the global data storage market is projected to grow from $250.8 billion in 2025 to $483.9 billion by 2030 at a compound annual rate of 14%. Both WDC and STX are well-positioned to benefit from these growing trends, attracting renewed investor interest. However, if investors must choose between the two, which stock should they consider based on fundamentals, valuations, growth potential and risks?

Let’s explore this in detail.

Cloud service providers (CSPs) are increasingly investing in AI applications and expanding their infrastructure. Seagate anticipates that HDDs will play a critical role in supporting these phases of AI adoption, with demand expected to accelerate. As data volumes surge, the need for mass-capacity storage is extending beyond cloud environments into edge data centers, where data is generated, stored for longer periods and replicated across locations to train and support AI models. Additionally, with nearly half of global data centers concentrated in just four countries, evolving data sovereignty regulations are fueling demand for localized storage solutions.

In this context, mass capacity hard drives provide the ideal balance of space, efficiency and cost, helping to ensure data security and compliance. Seagate is seeing a surge in demand for mass capacity storage, with nearline cloud storage demand increasing. It expects that enterprise edge storage will follow the cloud trend, with AI investments fueling long-term demand. The company continues to observe strong demand for high-capacity nearline products from cloud customers worldwide.

A key pillar of Seagate’s strategy is the ramp-up of its HAMR technology to address rising demand from cloud providers. Its HAMR-based Mozaic drives remain the industry’s only products delivering 3 terabytes per disk. Seagate is scaling volume production of Mozaic 3+ drives by leveraging common features across its PMR and HAMR platforms, with shipments broadening to additional CSPs in the September quarter and qualifications advancing steadily.

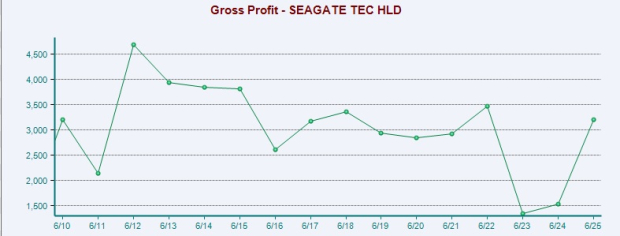

The company’s expanding margins, cushioned by the growing adoption of its high-capacity nearline products and the continued execution of pricing initiatives, bode well for its prospects. In the last reported quarter, non-GAAP gross margin was 37.9%, expanding 170 basis points (bps) sequentially and nearly 700 bps year over year.

Moreover, its robust cash flow funds innovation and growth while supporting dividends and buybacks. In fiscal 2025, it reduced debt by $684 million while maintaining shareholder returns, demonstrating balanced capital allocation. Management expects higher free cash flow in the second half, with share repurchases set to restart. A strong product pipeline and shifts in the business model position Seagate for higher profitability and steady dividends in fiscal 2026.

However, STX’s $5 billion debt against just $891 million in cash highlights a heavy burden. This leverage increases financial risk, and despite solid cash flow, it jeopardizes the company’s ability to sustain dividends, buybacks and future growth. It also faces growing pressure from rivals like Western Digital, as well as competition from storage subsystem providers and ongoing macroeconomic and supply chain challenges—factors that threaten its market position and increase execution risks.

Western Digital remains a cornerstone of the global data infrastructure, delivering exceptional value in mass storage solutions. The company is committed to innovation, advancing HDD technology to provide drives with greater capacity, enhanced performance, improved energy efficiency and the lowest total cost of ownership. To further expand its SSD business, the company formed a separate entity, Sandisk, in 2025. It has broadened its focus on the booming HDD market, giving tough competition to STX for a lion’s share of the sector.

The proliferation of AI is fueling demand for Western Digital’s platforms business, which delivers high-density storage systems designed to maximize drive performance and capacity. These solutions are gaining adoption among infrastructure providers and are particularly valuable for native AI companies that lack internal storage expertise. By enabling efficient, large-scale data handling, WDC is positioned to become a key enabler of AI workloads, from training to inference.

In addition to emerging AI trends, the advent of Agentic AI is powering demand for unstructured data storage. The company is already using AI to boost product development, while industry-wide adoption is generating data at unprecedented levels. As AI-driven innovation accelerates, the need for scalable, cost-efficient storage grows—keeping HDDs core to global data infrastructure.

WDC’s ePMR and UltraSMR technologies continue to deliver reliability, scalability and TCO benefits in the data center market. In the fiscal fourth quarter, it shipped 190 exabytes of storage, up 32% year over year, driven by strong demand for nearline drives and rapid adoption of its 26TB CMR and 32TB UltraSMR products—shipments of which more than doubled sequentially. Looking ahead, next-gen ePMR drives are set for qualification by early 2026, while HAMR drives, already showing promising results with hyperscalers, are on track for qualification in 2027. Management expects strong data center demand and greater adoption of high-capacity drives to support ongoing revenue growth and profitability in fiscal 2026.

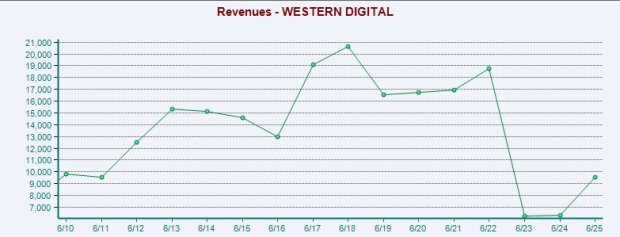

Western Digital’s profitability is improving as the company shifts toward higher-capacity drives and maintains strong cost discipline across its operations and supply chain. At the same time, disciplined cost management aids in reducing expenses. Together, these trends enhance efficiency, support healthier margins and strengthen the company’s ability to reinvest in innovation and long-term growth. In the last reported quarter, it posted a non-GAAP gross margin of 41.3%, up 610 bps year over year and above its guidance (40-41%), while non-GAAP operating costs fell 16% to $345 million.

However, it faces notable risks from its high customer concentration coupled with mounting debt load. As of June 27, 2025, cash and cash equivalents were $2.1 billion, while long-term debt (including the current portion) was $4.7 billion. The high debt level jeopardizes its ability to pursue accretive acquisitions and other growth endeavors. It is required to constantly generate adequate cash flows to meet debt requirements.

Also, macroeconomic volatility driven by tariffs and global trade tensions adds uncertainty, creating potential demand fluctuations across the enterprise, distribution and retail segments.

Nonetheless, in the June quarter, management took steps to reduce its debt and strengthen its balance sheet, improving overall financial flexibility. It generated $746 million in cash from operations, while free cash flow amounted to $675 million, up 139%. The company also launched a quarterly dividend program and a new share repurchase plan, underscoring its commitment to returning value to shareholders. Despite ongoing uncertainties in the global trade environment, management sees strong demand for its products, particularly as AI adoption and related trends continue to fuel growth opportunities.

Over the past year, STX and WDC have registered gains of 73.2% and 25.1%, respectively.

WDC looks more attractive than STX from a valuation standpoint. Going by the price/earnings ratio, WDC’s shares currently trade at 12.43 forward earnings, lower than 16.04 for STX.

The Zacks Consensus Estimate for STX’s earnings for fiscal 2026 has been revised up 4.15% to $10.30 over the past 60 days.

The Zacks Consensus Estimate for WDC’s earnings for fiscal 2026 has been revised up 13.4% to $6.50 over the past 60 days.

Both WDC and STX are poised to capitalize on the emerging data storage industry, capturing growth across multiple end-markets, from AI to enterprise to consumer storage. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

WDC at present sports a Zacks Rank #1, while STX has a Zacks Rank #3 (Hold). Consequently, in terms of Zacks Rank and valuation, WDC seems to be a better pick at the moment.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite