|

|

|

|

|||||

|

|

|

Surging global electricity usage, significantly driven by data center growth of late, has steadily contributed to strong demand for oil and gas over the past decade. This demand, further supported by technological advancements that have made extraction more efficient, has proved to be a major driving force for Crescent Energy (CRGY) and SM Energy (SM), two prominent shale explorers.

Both CRGY and SM are well-known upstream oil and gas exploration and production (“E&P”) companies, with shared operations in the Uinta basin of Utah. In addition, Crescent Energy’s operations focus on the Eagle Ford, while SM Energy operates in the Midland and Maverick basins. Both these stocks thrive on strategic acquisitions, optimized drilling technologies, and strong cash flow generation backed by solid sales volume for oil, natural gas, and natural gas liquids (NGLs).

As both these stocks are steadily growing their production volumes, supported by disciplined capital allocation and cost control initiatives, as well as offering solid balance sheet performance, investors interested in shale explorers might be in a quandary regarding which one of them should be in their portfolio. To ease this decision-making, let’s delve deeper into their fundamentals, as discussed below.

As strategic acquisitions continue to shape the U.S. shale industry by enhancing scalability, efficiency, and drilling inventory quality, they remain a key growth lever for explorers like Crescent Energy and SM Energy. A strong balance sheet is essential to sustain this momentum, yet both companies face notable solvency risks.

Crescent closed June 2025 with $7 million in cash and no short-term debt, but its long-term debt of $3.38 billion significantly outweighed liquidity. SM Energy reported $102 million in cash and no short-term debt; however, its long-term debt of $2.71 billion exceeded available cash.

On the cash flow front, SM posted a 40.1% year-over-year jump in operating cash flow during the first half of 2025, while Crescent recorded a stronger 77.6% surge. These healthy inflows, implying solid liquidity, support their acquisition strategies despite long-term leverage concerns.

Recent deals underscore this trend. SM Energy’s $2 billion-plus Uinta Basin acquisitions (closed October 2024) expanded its production base. Crescent has also pursued an aggressive growth strategy, completing the Ridgemar purchase and Silverbow merger last year. Its recently announced $3.1 billion acquisition of Vital Energy is expected to close by 2025-end.

These transactions (except for Vital Energy) are already boosting output. SM’s second-quarter 2025 production rose 32% year over year, driving 25% revenue growth, with Uinta assets as the key performance driver. Crescent Energy, meanwhile, reported a 59.4% jump in daily sales volumes, fueling a 37.5% revenue increase to $898 million, partly aided by Eagle Ford assets from Ridgemar.

We may expect these acquisitions to play the role of critical growth catalysts for both SM and CRGY and should continue to fuel their revenues.

Looking ahead, the fundamental growth outlook for the natural gas market remains a strong tailwind for CRGY and SM, considering the steadily growing demand for natural gas, which has been the leading source of U.S. power generation since 2016, as stated by the U.S. Energy Information Administration (“EIA”).

Moreover, the EIA projects a notable increase in U.S. natural gas spot prices in fourth-quarter 2025 and throughout 2026. This should further boost revenue growth for CRGY and SM from increased natural gas sales.

Although the growth outlook for natural gas remains bright, the outlook for the oil market is less favorable, which, in turn, might hurt both CRGY and SM. To this end, the International Energy Agency (“IEA”) stated in its March 2025 report that the macroeconomic conditions that influence oil demand projections have deteriorated recently as trade tensions escalated between the United States and several other countries, particularly following the heightened U.S. imported tariffs, combined with escalating retaliatory measures.

Moreover, a decline is expected in the U.S. oil prices in the near term, as projected by EIA in its latest short-term energy outlook report, primarily with OPEC members accelerating their production increases, which might outpace demand growth and pull down prices. This is likely to affect oil revenue growth for both Crescent Energy and SM Energy in the coming quarters. Also, as a result of enhanced tariffs, the rising price of raw materials such as steel, a critically needed material in the oil and gas industry, is putting upward cost pressure on U.S. shale explorers, thereby clouding their earnings growth prospects.

The Zacks Consensus Estimate for CRGY’s 2025 sales implies a year-over-year improvement of 23.3%, while the same for its earnings per share (EPS) suggests a decline of 14.6%. The stock’s near-term EPS estimates have moved north over the past 60 days.

The Zacks Consensus Estimate for SM’s 2025 sales implies a year-over-year improvement of 23.9%, while that for earnings suggests a deterioration of 13.8%. The stock’s near-term bottom-line estimates have moved south over the past 60 days, except for 2025.

CRGY (up 14.5%) has underperformed SM (up 22.7%) over the past three months but has outperformed the same in the past year. Shares of CRGY have lost 19.4%, while those of SM have declined 37% over the said period.

SM Energy is trading at a forward earnings multiple of 5.25, below Crescent Energy’s 6.66.

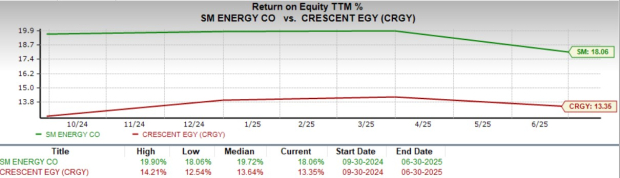

A comparative analysis of both these stocks’ Return on Equity (ROE) suggests that SM is more efficient at generating profits from its equity base compared to CRGY.

Both Crescent Energy and SM Energy stand out as strong shale players, underpinned by disciplined capital allocation, strategic acquisitions and rising production volumes. However, investors should remain cautious of the fact that both these stocks have high long-term debt burdens.

Crescent’s aggressive acquisition spree, particularly through the Vital Energy deal, offers scalability and revenue upside. SM Energy, meanwhile, presents stronger valuation metrics, better ROE, and healthier liquidity, making it relatively more attractive for risk-conscious investors. While CRGY’s growth prospects look robust, SM’s attractive valuation and superior capital efficiency suggest it currently has the edge as the more compelling choice to remain in a shale investor’s portfolio, despite industry headwinds.

Both SM and CRGY stocks carry a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks Rank #1 (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-14 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jun-02 | |

| Jun-01 | |

| May-28 | |

| May-26 | |

| May-21 | |

| May-14 | |

| May-07 | |

| May-06 | |

| May-06 | |

| May-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite