|

|

|

|

|||||

|

|

|

Despite its smaller cloud market share, Oracle has significant advantages compared to Amazon, Microsoft, and Alphabet.

Netflix is at the top of its game, but its valuation is extended.

Nvidia’s latest quarterly results showcase why the stock remains a compelling long-term buy.

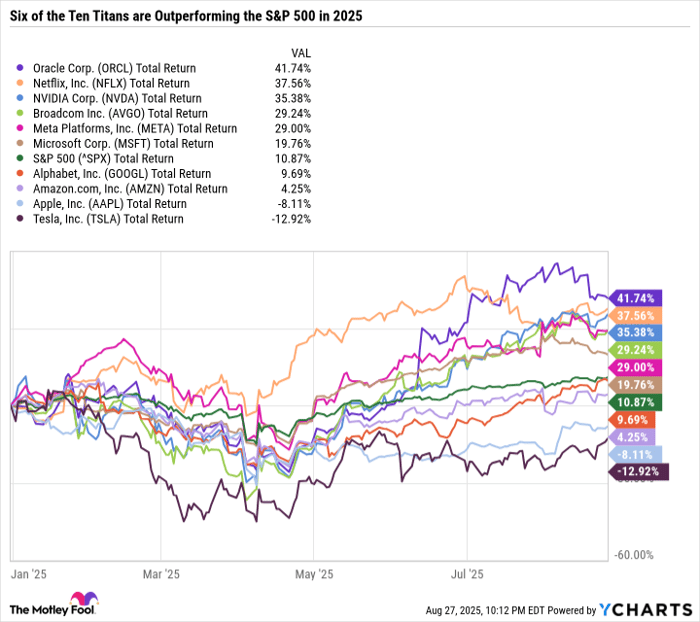

The 10 largest growth-focused U.S. companies now make up 38% of the S&P 500. Known as the "Ten Titans," the list includes Nvidia (NASDAQ: NVDA), Microsoft, Apple, Amazon, Alphabet, Meta Platforms, Broadcom, Tesla, Oracle (NYSE: ORCL), and Netflix (NASDAQ: NFLX).

Oracle, Netflix, and Nvidia have been the best performers of the Titans year to date. Let's determine if these growth stocks have what it takes to continue outperforming next year.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

Oracle has been the standout among the Titans. With a year-to-date total return of more than 40%, it vaulted its market cap above $660 billion.

ORCL Total Return Level data by YCharts.

Oracle was close to dead money in the five years between 2015 and the end of 2019 -- gaining just 17.8% compared to 56.9% for the S&P 500. But since the start of 2020, Oracle is up 345% compared to a 100.6% gain in the S&P 500. A big driver of the outperformance is the build-out and adoption of Oracle Cloud Infrastructure (OCI).

Oracle transformed from a database-first company to a fully fledged ecosystem. Not long ago, companies were using Oracle's database software on third-party clouds. Oracle decided to capture that revenue by building out its own cloud services.

Oracle Integration Cloud hosts software-as-a-service offerings for financial reporting, automated workflows, human resources operations, marketing, personalization, and more. Oracle also offers artificial intelligence (AI)-powered database services. And OCI has been shown to be much more cost-effective for data-intensive operations than Amazon Web Services, Microsoft Azure, or Google Cloud. It's an especially ideal offering for industries like financial services and healthcare that have complex regulatory frameworks and sensitive information. On its earnings calls, Oracle often discusses how industries are choosing OCI for its security and compliance capabilities.

Oracle was already a leader in enterprise software solutions. And now, it is a major player in the cloud business. The main downside of Oracle is that its valuation is expensive, and it is spending extremely aggressively. Oracle is arguably among the higher-risk, higher-potential-reward Titans. If its investments translate to bottom-line earnings growth, it could continue to be one of the best performers in the group. If not, it wouldn't be surprising if the stock underwent a sizable sell-off.

Netflix's outsized returns in recent years are partly due to how beaten down the stock was going into 2023. Netflix fell over 50% in 2022, outpacing the broader sell-off in the Nasdaq Composite (NASDAQINDEX: ^IXIC) that year. At the time, other streaming platforms were gaining traction, and Netflix was still inconsistently profitable.

The business model has remained largely unchanged over the past decade. So it's not a transformational story like Oracle. Rather, Netflix has perfected its craft.

The biggest change has been its content slate -- what it spends on, how it markets that content (like the global success of "KPop Demon Hunters,") and basically just boosting its overall content success rate. The second major change was cracking down on password sharing. This was a resounding success because a lot of new accounts opened up -- showing that customers were willing to pay for Netflix because they value the service (again, despite a lot of competition). And finally, Netflix's ad-supported tier is driving new signups, which accelerates revenue growth.

Netflix is an industry-leading cash cow with high margins. It has become a near-perfect business. The only issue is that the valuation reflects that, as Netflix trades at 52 times trailing 12-month earnings. Netflix could still be a winning long-term stock, but it may need a year or two to grow into its valuation. Therefore, it may not be a standout performer in 2026.

Nvidia reported exceptional second-quarter fiscal 2026 results on Aug. 27 despite the company's China business being hindered by export restrictions to China.

Even with difficult comps from the second-quarter fiscal 2025, Nvidia grew revenue by 56% and adjusted earnings per share by 54%. Arguably, the most impressive aspect of Nvidia's results is that it continues to sustain ultra-high gross margins over 70%. Nvidia's high margins allow it to convert a substantial amount of sales into profit, which is a testament to its edge over the competition and technological leadership on the global stage.

Nvidia gets a lot of attention for its data center business -- and rightfully so, as it made up 88% of revenue in the recent quarter. But it's worth noting that the rest of the business is doing well too. Nvidia's non-data center revenue, which includes gaming and AI PC professional visualization, automotive, and robotics, was collectively $5.49 billion -- up 48% compared to $3.7 billion a year ago.

Nvidia is in its third year of what has been an uninterrupted masterclass of exponential growth on a scale unlike any business the world has ever seen. And somehow, the company still has its foot on the gas with no signs of slowing down.

Nvidia's outlook for the third-quarter fiscal 2026 calls for $54 billion in revenue even if it ships zero H20 chips to China -- all while maintaining a 73% gross margin. That would mark a 54% increase in revenue and just slightly lower gross margins than third-quarter fiscal 2025 and a near three-fold increase in revenue in just two years.

Despite the impeccable results, Nvidia's valuation isn't cheap, as investors are pricing in a sustained breakneck growth rate. But Nvidia just keeps delivering, so its 58.4 price-to-earnings ratio is reasonable.

If Nvidia's stock price remained unchanged for a year but the company grew earnings by 50%, the P/E would drop to 38.9. So even now, with the stock on track to crush the S&P 500 for the third consecutive year, Nvidia remains a top AI stock to buy now.

I expect Nvidia to continue leading the Ten Titans higher in 2026, especially if trade policy with China eases. However, if for whatever reason there's a slowdown in AI spending from key Nvidia customers, Nvidia could drag down the Ten Titans and the broader market with it.

Before you buy stock in Oracle, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Oracle wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $651,599!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,067,639!*

Now, it’s worth noting Stock Advisor’s total average return is 1,049% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Daniel Foelber has positions in Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Netflix, Nvidia, Oracle, and Tesla. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 13 min | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 |

Paramounts Newest Bid Could Open Door to Beating Netflix Deal, Warner Says

NFLX

The Wall Street Journal

|

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite