|

|

|

|

|||||

|

|

|

The quality of Microsoft's business justifies its premium valuation.

Brookfield Asset Management and Verizon continue to reward their shareholders with attractive dividends.

The sell-off in Target and Procter & Gamble is a buying opportunity.

Amid the back-to-school season and hints of crisp fall air, it's easy to miss the epic run the U.S. stock market has been on.

At the time of this writing, the S&P 500 (SNPINDEX: ^GSPC) is up 9.6% year to date and has gained a staggering 33% from its April low as investors bet big on sustained innovation from artificial intelligence (AI).

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

With the market at an all-time high, investors may be grappling with what to do next, whether that's sticking with winning companies, digging deep in the bargain bin for hidden gems, or something in between. While it's never a good idea to overhaul your investment portfolio on emotion or just because the market has gone up, it can be a good idea to review what you own and why you own it, and make sure your holdings align with your risk tolerance and investment objectives. Holding shares in well-run businesses is a great way to bolster your conviction and be prepared for whatever comes next.

Here's why these Fool.com contributors believe that Microsoft (NASDAQ: MSFT), Brookfield Asset Management (NYSE: BAM), Verizon Communications (NYSE: VZ), Target (NYSE: TGT), and Procter & Gamble (NYSE: PG) stand out as top stocks to buy in July.

Image source: Getty Images.

Demitri Kalogeropoulos (Microsoft): Sure, it's already an over $3 trillion company. But Microsoft still looks like a great long-term buy heading into September. The software giant just closed out an eye-popping fiscal year headlined by a 15% revenue spike and even faster profit growth. Microsoft booked $129 billion of operating income in the past 12 months, in fact, translating into a blazing 46% profit margin.

You can't fault Wall Street for being excited about the potential for this business to capitalize on tech trends such as AI, the pivot toward subscription software services, and the cloud. That optimism helps explain why Microsoft stock has more than doubled since mid-2020.

The rally has admittedly pushed the stock into "expensive" territory, trading at 37 times the past year's earnings. Microsoft earns that premium, though, by providing a level of diversity that's hard to find in the tech world. Where else can you get so much exposure to enterprise and consumer software, gaming, and consumer tech in one package?

But the best reason to like Microsoft right now might be the simplest: cash flow. The tech giant generated $136 billion of operating cash this year, up from $119 billion in fiscal 2024. Those resources should support aggressive growth investments over the coming years while leaving room for an expanding dividend and ample stock buyback spending -- all factors that point to excellent shareholder returns from here.

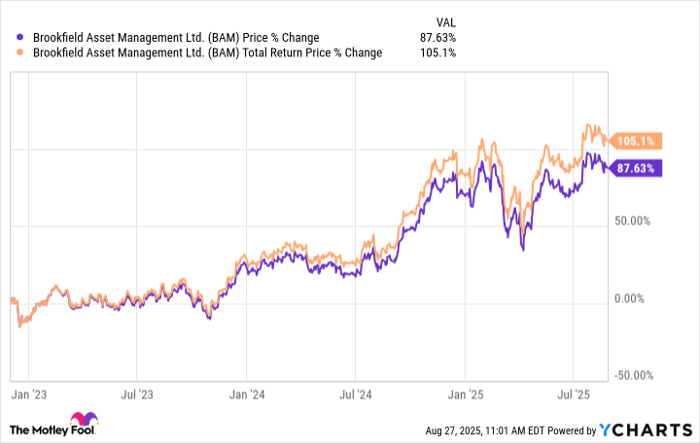

Neha Chamaria (Brookfield Asset Management): Brookfield Asset Management was founded in late 2022 after the spinoff of the asset management operations of Brookfield Corporation (NYSE: BN), itself formerly known as Brookfield Asset Management. Investors who bought the stock then have already doubled their money, with dividends reinvested. Management believes the "best is yet to come," and it's highly likely those words will come true for investors who buy shares of Brookfield Asset Management now for five reasons.

First, Brookfield Asset Management is among the world's largest asset management companies with over $1 trillion of assets under management, with a goal to double the size of its business in five years. Second, the company generates revenue under long-term, fee-based contracts, which makes its revenue and cash flows highly stable and resilient. Third, megatrends like digitalization, decarbonization, and deglobalization should open up massive opportunities for Brookfield Asset Management across all five of its verticals -- renewable power and transition, infrastructure, real estate, private equity, and credit.

Fourth, the company believes these opportunities, investments, and pipelines could boost its fee-based and distributable earnings per share by compound annual growth rates of 17% and 18%, respectively, through 2029. Fifth, the company expects that earnings growth will support over 15% annual dividend growth.

Put it all together, and you have one of the most compelling investing theses here. It's a simple investing strategy: Brookfield Asset Management is a solid multibagger contender. Simply buy the stock now and hold.

Keith Speights (Verizon Communications): Are you at least a little uneasy about frothy stock valuations and the possibility of market disruptions in the near future? If so, I think Verizon Communications could be an ideal stock for you.

Let's start with the telecommunications giant's valuation. Verizon's shares trade at a forward price-to-earnings (P/E) ratio of only 9.4. That's a fraction of the S&P 500's forward earnings multiple of 22.8. It's also much more attractive than the forward P/E ratio of 13.8 for Verizon's top rival, AT&T (NYSE: T).

Want even better news? Verizon has been a decidedly low-volatility stock in recent years. Its beta over the last five years is a super-low 0.36. I suspect that will remain the case going forward. Verizon's business continues to perform well, with the company reporting industry-leading wireless service revenue in the second quarter of 2025. The company is adding broadband and mobility customers at a healthy rate.

Sure, Verizon faces competition. However, the company stacks up well against others in the industry. As a case in point, J.D. Power recently recognized Verizon for having the best wireless network quality. This was the 35th time that Verizon earned this distinction. RootMetrics also selected Verizon's 5G network as the best, fastest, and most reliable in the U.S.

There's one other reason I really like Verizon, though: its dividend. The telecom company's forward dividend yield is an ultra-high 6.16%. Verizon has also increased its dividend for 18 consecutive years. Even if the stock market tanks, this stock will pay you handsomely to wait for better days.

Anders Bylund (Target): Wall Street is acting as if Target is going out of business. The big-box retailer trades at valuations normally reserved for truly desperate situations -- 11.3 times trailing earnings and 0.4 times sales. Meanwhile, investors are celebrating arch-rivals Walmart (NYSE: WMT) and Costco Wholesale (NASDAQ: COST) with valuation ratios doubling or even tripling Target's.

Sure, Target has some issues. The company's sales and earnings growth have stalled in recent years as it continues to struggle to overcome the inflation-driven retail panic of 2022. But Target has embraced a promising turnaround strategy, avoiding a rock-bottom price war with its cost-effective rivals. Instead, the company celebrates its slightly higher-end market position with the French-flavored "Tar-zhay" moniker. Offer a better shopping experience, and consumers will gladly pay a little bit extra. That's the idea, and I like it.

So, who sports the strongest net and operating profit margins in the big-box retail trio? That would be Tar-zhay. The company is already doing something right, and I look forward to seeing Target address the next holiday shopping season.

A leadership change is coming in February, but I'm not worried about that, either. Incoming CEO Mike Fiddelke is a longtime insider with several years of top-level executive experience. He should hit the ground running, with longtime CEO Brian Cornell providing support as Target's executive chairman.

So, I think Target is on the right track, and Wall Street should give the stock a fresh look as this turnaround effort unfolds. Meanwhile, you can pick up Target shares from the stock market's bargain bin, paired with a generous dividend yield of 4.7%. Don't be surprised if Tar-zhay starts ringing up even stronger profits over the next few years, making today's bargain hunters look like geniuses in the long run.

Daniel Foelber (Procter & Gamble): P&G is a highly diversified consumer staples company with leading brands across major everyday use categories -- including fabric and home care, grooming and beauty, baby, feminine, and family care, and healthcare. Tide, Gillette, Bounty, Charmin, Dawn, Febreze, and Crest are just a few of its dozens of recognizable brands.

P&G's lineup of brands spanning several categories, supply chain, and marketing makes it a juggernaut in the consumer brands space. But even with its many advantages, P&G hasn't been immune to the impact of higher costs and strained consumer spending.

In July, P&G reported its fourth-quarter and full-year results -- including net sales growth of 0% and organic sales growth of just 2%. The impact of foreign exchange offset pricing increases. Most concerning of all was flat sales volume. P&G expects fiscal 2026 to show slight improvement, with 1% to 5% sales growth and a 3% to 9% increase in diluted earnings per share compared to 8% in fiscal 2025. All told, the company's results have been fairly mediocre relative to investor expectations, and the near-term guidance suggests that mediocrity will persist.

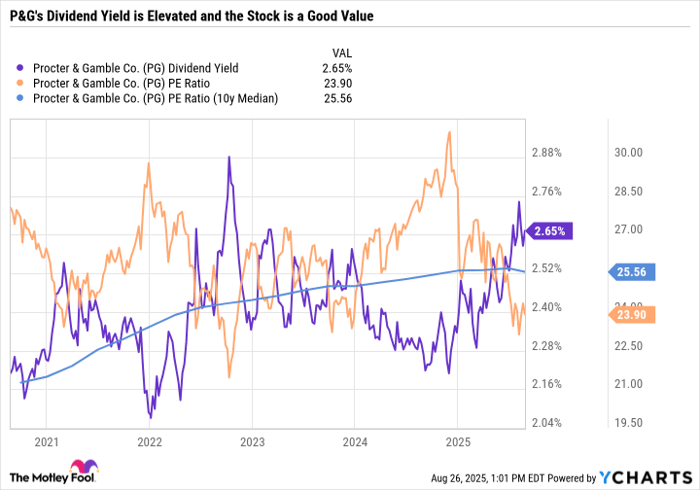

Still, P&G is growing at a pace that allows it to return value to shareholders through buybacks and dividend increases. P&G has boosted its annual payout for 69 consecutive years, making it one of the longest-tenured Dividend Kings. And there's no reason to think that will change anytime soon.

The stock is hovering around a 52-week low, pushing the yield up to around the high end of P&G's five-year range and the price-to-earnings ratio below the 10-year median.

PG Dividend Yield data by YCharts

Some of the best buying opportunities in the stock market come when top-tier companies go on sale for what appear to be near-term issues that don't have to do with the underlying investment thesis. That's exactly what's happening with P&G, making it a safe stock that dividend and value investors can confidently buy in September and hold for years to come.

Before you buy stock in Microsoft, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Microsoft wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $651,599!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,067,639!*

Now, it’s worth noting Stock Advisor’s total average return is 1,049% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Anders Bylund has positions in Walmart. Daniel Foelber has positions in Procter & Gamble. Demitri Kalogeropoulos has positions in Costco Wholesale. Keith Speights has positions in Microsoft, Target, and Verizon Communications. Neha Chamaria has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Brookfield, Brookfield Corporation, Costco Wholesale, Microsoft, Target, and Walmart. The Motley Fool recommends Brookfield Asset Management and Verizon Communications and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 1 hour | |

| 3 hours | |

| 3 hours | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite