|

|

|

|

|||||

|

|

|

Cencora, Inc. COR is well-poised for growth on the back of a robust U.S. Healthcare Solutions business and product launches. However, intense competition is a concern.

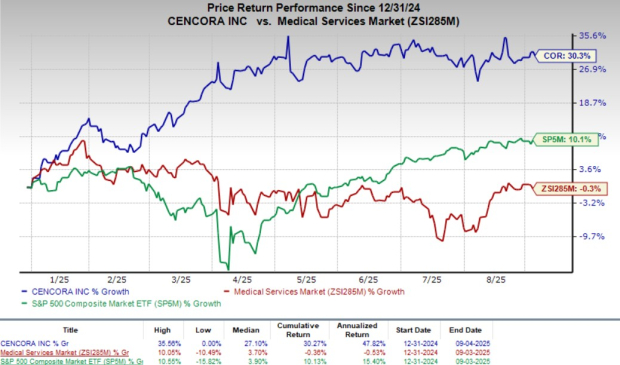

Shares of this Zacks Rank #3 (Hold) company have risen 30.3% so far this year against the industry’s 0.3% decline. The S&P 500 Index has jumped 10.1% in the same time frame.

Cencora is one of the world’s largest pharmaceutical service companies. It is focused on providing drug distribution and related services to reduce healthcare costs and improve patient outcomes. The company has a market capitalization of $57.22 billion.

COR’s bottom line is anticipated to improve 13.2% over the next five years. Its earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 6.19%.

COR delivered a strong second quarter in fiscal 2025, fueled by sustained momentum in its U.S. Healthcare Solutions segment. Specialty products and GLP-1 therapies were standout drivers, and management expects these categories to remain key growth engines in the year ahead. The company’s peers are also doubling down on high-margin therapies as demand rises for treatments addressing complex conditions such as rheumatoid arthritis and cancer.

Earnings per share climbed 19.8% year over year to $4.00, while revenues advanced 8.7% to $80.7 billion. International revenues grew 8.8% at constant currency, led by European and Canadian markets. However, profitability in the International segment was pressured by weaker results in global specialty logistics, partially offset by strength in European distribution.

COR raised its fiscal 2025 outlook. Adjusted EPS is now estimated between $15.85 and $16.00 (previously $15.70–$15.95), representing 15–16% growth from last year. Revenues are expected to increase 9%, with U.S. Healthcare Solutions projected to grow 9–10% and International Healthcare Solutions 6-7%. Adjusted operating income is anticipated to rise 15-16%, up from the earlier estimate of 13.5–15.5%.

Cencora also acquired Retina Consultants of Americaearlier this year, expanding its specialty capabilities beyond oncology. This acquisition complements COR’s pharmaceutical-centric strategy, strengthens its Management Services Organization portfolio and positions it well in the growing retina and ophthalmology market.

Cencora continues to benefit from its focus on specialty pharmaceuticals, a key driver of growth. Rising demand for GLP-1 therapies and specialty distribution services for physicians and health systems is fueling strong revenue momentum. The company’s investments in advanced distribution infrastructure and technology are strengthening logistics, enhancing cold-chain handling for temperature-sensitive products and improving compliance with regulatory standards.

In international markets, automation initiatives and operational consistency across Cencora’s European and Canadian businesses are helping build resilience and scalability. Meanwhile, renewed partnerships with Express Scripts and Walgreens reinforce its core distribution network, ensuring resources remain aligned with evolving customer needs.

Cencora faces intense competition in pharmaceutical distribution and healthcare services. The generic drug sector continues to consolidate across customers and manufacturers, while global rivals and evolving regulations add further pressure.

Profitability is being squeezed by higher sales of lower-margin GLP-1 products and the ongoing decline in COVID-related revenues. Shifts in U.S. healthcare policy, particularly Medicare Part B and D reimbursement reforms, pose additional risks to earnings. The recent goodwill impairment at PharmaLex underscores weakness in outsourced pharma services amid broader market headwinds.

Rising competition in both specialty drugs and biosimilars may further challenge Cencora’s market share and pricing power.

COR has been witnessing a positive estimate revision trend for fiscal 2025. In the past 30 days, the Zacks Consensus Estimate for earnings has increased from $15.81 to $15.92 per share.

The consensus mark for fourth-quarter fiscal 2025 revenues is pegged at $83.91 billion, indicating a 6.1% improvement from the year-ago reported actuals. The bottom-line estimate is pinned at $3.84, implying year-over-year growth of 15%.

Cencora, Inc. price | Cencora, Inc. Quote

Some better-ranked stocks in the broader medical space are Medpace Holdings, Inc. MEDP, West Pharmaceutical Services, Inc. WST and Boston Scientific Corporation BSX.

Medpace Holdings, sporting a Zacks Rank #1 (Strong Buy), reported second-quarter 2025 EPS of $3.10, beating the Zacks Consensus Estimate by 3.3%. Revenues of $603.3 million outpaced the consensus mark by 11.5%. You can see the complete list of today’s Zacks #1 Rank stocks here.

Medpace Holdings has a long-term estimated growth rate of 11.4%. MEDP’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 13.9%.

West Pharmaceutical reported second-quarter 2025 adjusted EPS of $1.84, beating the Zacks Consensus Estimate by 21.9%. Revenues of $766.5 million surpassed the Zacks Consensus Estimate by 5.4%. It currently flaunts a Zacks Rank #1.

West Pharmaceutical has a long-term estimated growth rate of 8.5%. WST’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 16.8%.

Boston Scientific reported second-quarter 2025 adjusted EPS of 75 cents, beating the Zacks Consensus Estimate by 4.2%. Revenues of $5.06 billion surpassed the Zacks Consensus Estimate by 3.5%. It currently carries a Zacks Rank #2 (Buy).

Boston Scientific has a long-term estimated growth rate of 14%. BSX’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 8.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-13 |

How Cardinal Health, The IBD Stock Of The Day, Is Navigating The Tricky Macro

COR

Investor's Business Daily

|

| Mar-13 | |

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite