|

|

|

|

|||||

|

|

|

Exxon Mobil Corporation XOM has built its moat on capital discipline and advantaged upstream assets. In the second quarter of 2025, XOM began production at its fourth Guyana offshore mega-project, Yellowtail, boosting Guyana capacity past 900,000 barrels per day with a clear path to 1.7 million boe/d by 2030.

ExxonMobil’s success in Guyana is rooted in ultra-low lifting costs, robust reserve growth, and a record of delivering projects ahead of schedule and under budget. This upstream focus drives 80% of net earnings and supports durable free cash flow, even as commodity prices fluctuate. ExxonMobil’s disciplined approach yields resilient dividends, sector-leading returns and the ability to reinvest heavily in future projects while maintaining strong financial flexibility.

Chevron Corporation’s CVX acquisition of Hess for $53 billion secured a coveted 30% share in the Stabroek Block, resolving years of reserve declines and cost overruns. Chevron’s Guyana assets promise 465,000 boe/d incremental output and more than $1B in annual cost synergies, bolstering production and dividend capacity well into the next decade. Chevron’s expanded deepwater portfolio provides a credible, high-margin growth stream, transforming its upstream risk profile and market standing.

BP plc BP relies on balanced global expansion and disciplined exploration rather than blockbuster individual frontier plays. Recent developments in the Argos Southwest Extension and the deepwater Bumerangue discovery in Brazil exemplify BP’s strengths, including flexible project allocation and geographic risk balancing. BP aims to grow production to 2.3-2.5 million boe/d by 2030, but its Guyana exposure remains limited relative to ExxonMobil and Chevron. While BP delivers reliable cash flows and innovation, its upstream competitiveness stems from scale, agility and broad-based exploration, not from dramatic low-cost surges or landmark market share gains.

ExxonMobil’s combination of Guyana prowess, cost discipline and upstream diversification sets the sector’s bar for sustainable competitive moats. Chevron’s strategic reinvention through Guyana ensures direct rivalry, while BP’s diversified execution highlights the contrasting models of upstream advantage in a transforming energy landscape.

Shares of XOM have declined 0.2% over the past year against the industry’s 4% growth.

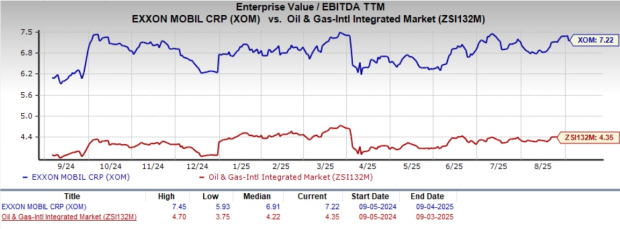

From a valuation standpoint, XOM trades at a trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 7.22X. This is above the broader industry average of 4.35X.

The Zacks Consensus Estimate for XOM’s 2025 earnings has been revised upward over the past 30 days.

ExxonMobil stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite