|

|

|

|

|||||

|

|

|

Consumer staples companies sell relatively cheap products that are used regularly.

Many consumer staples companies have achieved Dividend King status.

PepsiCo has a historically high yield even as it continues to invest for a brighter future.

If you take a look at all of the companies on the list of 2025 Dividend Kings, you'll find the name PepsiCo (NASDAQ: PEP). It has increased its dividend annually for 53 consecutive years at this point. That's a great record for any company, but this consumer staples giant offers much more than just an impressive history of dividend increases.

The best part, however, is that the stock is still out of favor on Wall Street. Here's what you need to know before you buy it.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Image source: Getty Images.

PepsiCo is a consumer staples company, as noted. This means it makes products that are relatively inexpensive and bought on a regular basis. To be fair, PepsiCo's products are branded and relatively expensive for their niches, but they are all considered affordable luxuries and few people question buying them. In fact, the brands that PepsiCo owns tend to elicit a lot of consumer loyalty.

Specifically, PepsiCo makes beverages (Pepsi), salty snacks (Frito-Lay), and packaged foods (Quaker Oats). It is an important player in each segment of its business, with an industry-leading position in the salty snack space and a second-place ranking in beverages. All in all, it is one of the most diversified branded consumer staples companies you can buy.

This diversified business model's strength is highlighted by PepsiCo's status as a Dividend King. You simply can't achieve a dividend record like that by accident. It requires a strong business model that is executed well in both good times and bad. This is important because even well-run companies go through bad times. Right now, PepsiCo is struggling a little bit.

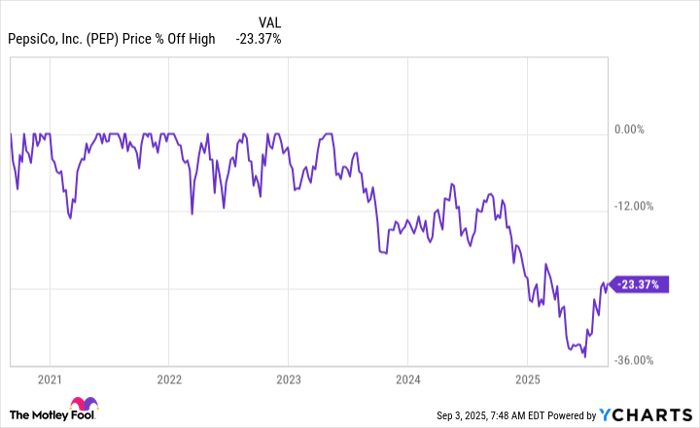

Even after a recent price rally, PepsiCo's shares remain down nearly 25% from their 2023 highs. That price decline has pushed the dividend yield up to around 3.8%, which is toward the high end of the stock's historical yield range. This hints at a cheap valuation, a fact that is buttressed by the fact that PepsiCo's price-to-sales and price-to-book value ratios are both below their five-year averages.

The caveat here is that PepsiCo's price-to-earnings ratio is close to the longer-term average. But that's not surprising given the company's recent performance weakness. And it is important to note that sales, book value, and dividends all tend to be more consistent over time than earnings, which can be very volatile from quarter to quarter. Taken together, the data here suggests a relatively cheap entry point for long-term investors.

The bet is that the company's recent weak performance will improve in the future. To put some numbers on that statement, PepsiCo's organic sales were less than half the level achieved by its arch beverage rival Coca-Cola in the second quarter of 2025. The two companies, however, have a habit of switching places performance-wise. Right now is Coca-Cola's time to shine.

PepsiCo isn't sitting still and hoping for the best. It is using its historically successful playbook to position itself for a brighter future. That has notably included buying a Mexican-American food maker and a probiotic drink maker, moves that should help the company's product portfolio better align with consumer buying habits. It has also inked a deal to increase its stake in Celsius Holdings to 11%, as it buys more of the strongly performing energy drink maker.

Then there's a new development, with activist investor Elliott Investment Management having taken a stake in PepsiCo. The stock jumped on the news noting that the involvement of Elliot means there's an outsider helping to push the consumer staples giant toward the changes needed to get back on track.

None of these moves is going to instantly turn PepsiCo from an industry laggard to an industry leader. But they do show how management is working to position the business for growth. And that, in time, should have the same effect it has in the past, better performance.

For long-term investors with a dividend focus, there's still plenty of opportunity for upside from this underrated consumer staples stock and Dividend King. But don't dawdle -- the recent rally suggests that Wall Street is starting to catch on to the opportunity ahead for PepsiCo.

Before you buy stock in PepsiCo, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and PepsiCo wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $678,148!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,052,193!*

Now, it’s worth noting Stock Advisor’s total average return is 1,065% — a market-crushing outperformance compared to 186% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Reuben Gregg Brewer has positions in PepsiCo. The Motley Fool has positions in and recommends Celsius. The Motley Fool has a disclosure policy.

| 8 hours | |

| Apr-01 | |

| Mar-31 | |

| Mar-29 |

Food Mega-Mergers Hardly Ever Work. Could McCormick-Unilever Be Different?

PEP

The Wall Street Journal

|

| Mar-25 | |

| Mar-25 | |

| Mar-24 | |

| Mar-23 | |

| Mar-23 | |

| Mar-20 | |

| Mar-20 | |

| Mar-20 | |

| Mar-20 | |

| Mar-19 | |

| Mar-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite