|

|

|

|

|||||

|

|

|

The Allstate Corporation ALL has been trading above its 50-day simple moving average (SMA), signaling a short-term bullish trend.

The 50-day SMA is a key indicator for traders and analysts to identify support and resistance levels. It is considered particularly important as this is the first marker of an uptrend or downtrend.

Allstate, the third-largest property-casualty insurer and the largest publicly-held personal lines carrier in the United States, is poised to deliver growth banking on growing premiums, business streamlining and solid cash flows.

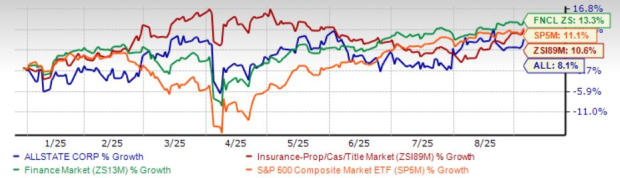

Shares of ALL have gained 8.1% in the year-to-date period compared with the industry’s growth of 10.6%. The Finance sector and the Zacks S&P 500 Composite have increased 13.3% and 11.1%, respectively, in the same time frame.

The insurer has a market capitalization of $54.9 billion. The average volume of shares traded in the last three months was 1.6 million.

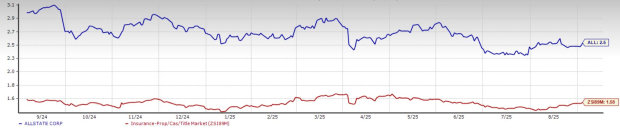

Shares of Allstate are trading at a premium compared with the industry. Its price-to-book value of 2.5X is higher than the industry average of 1.58X.

However, shares of Chubb Limited CB are trading at a multiple lower than the industry average, whileshares of The Progressive Corporation PGR and The Travelers Companies, Inc. TRV are trading at a premium.

The Zacks Consensus Estimate for ALL’s 2025 earnings per share (EPS) is pegged at $21.19, and the same for revenues is pegged at $69 billion. The consensus estimate for 2026 earnings per share and revenues indicates a rise of 7.7% and 5.4%, respectively, from the corresponding 2025 estimates. The expected long-term earnings are pegged at 11.8%, better than the industry average of 7%. It has a Growth Score of B

The Zacks Consensus Estimate for 2025 earnings has moved up 1.2% in the past seven days, while the same for 2026 has moved up 0.04% in the same time frame.

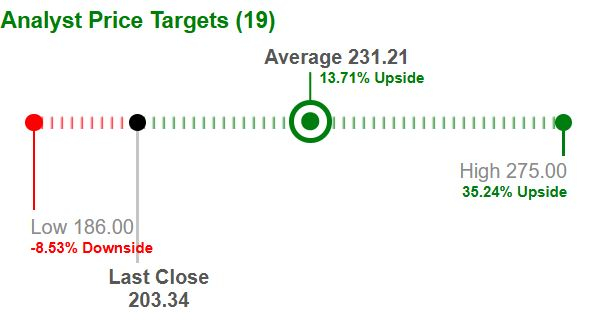

Based on short-term price targets offered by 19 analysts, the Zacks average price target is $231.21 per share. The average suggests a potential 13.7% upside from the last closing price.

Allstate’s growth trajectory is being shaped by steady expansion in premiums, supported by targeted acquisitions and new business ventures. By sharpening its core operations, the company has been able to channel resources into higher-growth segments while implementing cost efficiencies to protect margins. Strong cash flow generation further strengthens its ability to reward shareholders, underscoring a balanced approach to profitability and expansion.

Allstate continues to record healthy revenue gains, with premium growth serving as the primary engine. The first half of 2025 saw an 8.1% jump from the prior year, and a similar 8% increase is anticipated for the full year. This strength reflects a balanced mix of disciplined pricing, portfolio diversification, and selective acquisitions.

Alongside premium growth, Allstate is broadening its reach by scaling protection services and strengthening its property-liability business. Its vast policy base, trusted brand, and expanding offerings, ranging from identity protection to roadside assistance, create multiple avenues for growth. Combined with disciplined capital management, these initiatives reinforce long-term value creation for the business and its shareholders.

Looking ahead, management’s focus on rate revisions, product upgrades, and a pivot toward more profitable segments is expected to extend the momentum. Importantly, inflation-driven cost pressures are being countered through further pricing actions, ensuring that revenue expansion remains on track.

Despite steady growth, Allstate continues to face several challenges. Exposure to catastrophe-related losses and a relatively high debt burden weigh on its financials, while inflationary pressures and supply chain disruptions have pushed up claims and repair costs. The rising complexity of vehicle technology has further driven up replacement expenses. Even with reinsurance support, severe weather events have strained underwriting results, pressuring both profitability and cash flows.

In addition, the company’s elevated leverage remains a concern. Allstate’s debt-to-capital ratio stood at 25.2%, higher than the industry average of 16.1%, reflecting a comparatively leveraged balance sheet. While its times interest earned ratio of 19 is stronger than the industry’s 17, any disruption in earnings could strain debt servicing, deteriorate credit strength, and add further pressure to overall financial stability.

Overall, Allstate demonstrates solid revenue momentum, disciplined pricing, and strategic expansion into higher-growth services. However, elevated leverage, catastrophe-related exposure, and rising cost pressures temper the outlook.

Given the overvaluation, it is therefore wise to adopt a wait-and-see approach on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite