|

|

|

|

|||||

|

|

|

Google's court case will not make it divest Chrome and Android.

It is still facing a lot of competition in artificial intelligence, but is fighting back strongly.

Shares of Alphabet stock have hit all-time highs but still trade at a reasonable valuation.

The wait is finally over for Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) shareholders. In a case that had the potential to upend the entire internet, the market received its determination of remedies in the Google Search monopoly case. Even though Google was deemed a monopoly business in the search engine market, a federal court judge decided against harsh remedies in the case due to the continued surge of artificial intelligence (AI) competitors in the past year.

Alphabet will keep its Chrome internet browser and Android mobile operating system, and can still pay Apple a hefty fee to make Google Search a default choice on its hardware devices. Alphabet has to do is share data with search engine competitors, which will likely not harm the business. This is gargantuan news for Alphabet's business, with the stock up over 10% this week on the announcement. Here's what the court ruling means and whether Alphabet stock is still a buy at all-time highs today.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Dominating the search engine category came from Google's superior product, but it also came from its ecosystem of free software that it provided internet users. Two of the key products it developed and acquired -- Android was bought by Google for $50 million -- were Chrome and Android.

Billions of people around the world use both of these services. It is statistically likely that the majority of readers will access this article from one or both of these services. Alphabet develops and maintains these systems for free in order to make sure people keep using Google Search. It was and still is an ingenious idea to build an ecosystem of free products in order to keep people within the Google sphere of influence and not switch over to a competitor, such as Bing.

Losing Chrome and Android in asset sales could have been devastating for Alphabet's competitive advantage. Google Search generates over $50 billion in quarterly revenue and is still growing 12% year over year as of last quarter. Search query advertising revenue remains highly lucrative, and Google will now be able to retain its dominance by keeping Chrome, Android, and the status quo.

Image source: Getty Images.

The main concern for Alphabet investors should now shift from this monopoly case to AI competition. OpenAI and its ChatGPT services are growing rapidly, closing in on 1 billion users in what would be a record time for a consumer internet company. Not since perhaps Facebook or TikTok has a product gone so viral so quickly.

Chatbot adoption is a threat to the search market if it replaces queries from users. Alphabet is not sitting still with this competition. It released the Gemini chatbot, which rivals ChatGPT and is catching up in user adoption. With its own infrastructure and semiconductor hardware, Google can deliver more AI queries than the competition at a fraction of the cost, which will enable it to push AI products to the billions of people who use Google Search right now. This gives it an advantage over OpenAI, which has to use third-party cloud providers.

Google's cloud division is doing remarkably well at the moment. Revenue grew 32% year over year last quarter, with operating margin expanding to 20%. This is one of the key advantages for Alphabet in AI as well as a way to monetize AI spending. It now makes up close to 10% of Alphabet's consolidated earnings power, a % that will keep growing over the next five years.

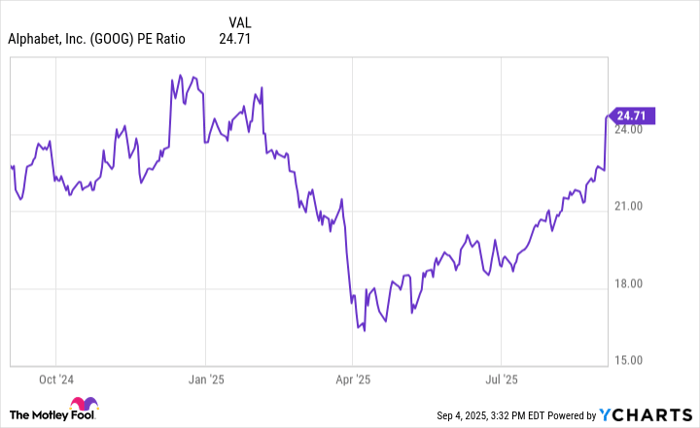

GOOG PE Ratio data by YCharts

Alphabet is facing a threat from OpenAI and other AI start-ups, but it is not taking the threat lying down. Neither will the competition kill Google's search business overnight, as you can see by the 12% year-over-year revenue growth last quarter.

This is more than just a search business, too. YouTube is a dominant video player owned by Alphabet, with advertising revenue growing 13% year over year. Android generates revenue from the Google Play Store, while there is growing subscription and hardware revenue from Pixel hardware and spending on Gemini.

There are plenty of assets in the Google ecosystem to help retain its dominance. At the same time, Alphabet is not a one-trick pony relying solely on Google Search for growth. Today, the stock trades at a price-to-earnings ratio of 25 even after hitting all-time highs, which is cheap for a company with its continued growth potential in AI and cloud computing. Buy Alphabet stock and sit tight with your gains over the long term.

When our analyst team has a stock tip, it can pay to listen. After all, Stock Advisor’s total average return is 1,052%* — a market-crushing outperformance compared to 185% for the S&P 500.

They just revealed what they believe are the 10 best stocks for investors to buy right now, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Brett Schafer has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet and Apple. The Motley Fool has a disclosure policy.

| 2 min | |

| 34 min | |

| 54 min | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite