|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Oracle ORCL delivered a milestone in the first quarter of fiscal 2026 as its Remaining Performance Obligations (RPO) soared 359% year over year to $455 billion, signaling one of the largest backlogs in the tech industry. Management highlighted that most of the next five years of growth is already “booked” and expects RPO to top $0.5 trillion with new multibillion-dollar deals, underscoring exceptional forward visibility.

The surge is fueled by the rapid adoption of Oracle’s cloud and AI offerings. This quarter alone, the company secured four multibillion-dollar contracts from OpenAI, Meta, NVIDIA and AMD, while Cloud RPO soared nearly 500% after 83% growth last year. Notably, 33% of total RPO is set to convert into revenues within the next 12 months, adding confidence in near-term performance.

Longer-term projections are even more ambitious. Oracle expects Oracle Cloud Infrastructure (OCI) revenues to climb 77% year over year to $18 billion in fiscal 2026, with a bold roadmap of $32 billion, $73 billion, $114 billion and $144 billion, respectively, over the next four years, much of which is already embedded in its backlog. To support this trajectory, Oracle is expanding aggressively with 37 new multi-cloud data centers, expanding its footprint to 71 globally. The Zacks Consensus Estimate reflects this optimism, projecting revenue growth of 16% in fiscal 2026 and nearly 19% in fiscal 2027. However, execution will be key.

With AI demand accelerating and one of the industry’s deepest revenue pipelines, Oracle’s record RPO points to durable growth ahead.

Microsoft MSFT is Oracle's toughest competitor through Azure and Microsoft Cloud, with a commercial RPO of $368 billion, up 35% year over year, and Azure revenues of $75 billion in fiscal 2025. Microsoft's massive scale, AI integration and global infrastructure reinforce its dominance, although rising costs and capacity constraints weigh on growth. While Oracle's $455 billion RPO is growing rapidly, Microsoft retains the top spot in revenues, and its robust ecosystem ensures lasting competitive strength.

Amazon AMZN maintains a strong competitive position through Amazon Web Services, with $195 billion in outstanding deposits at the end of the second quarter of 2025, including 25% growth and 17.5% revenue expansion year over year, further strengthening its position as the most mature cloud provider. Amazon's vast ecosystem, AI infrastructure and global scale are still strong, but Oracle's rapid RPO growth highlights the changing pace. While Amazon has a lead in breadth, Oracle's aggressive multi-cloud and AI deals are closing the gap.

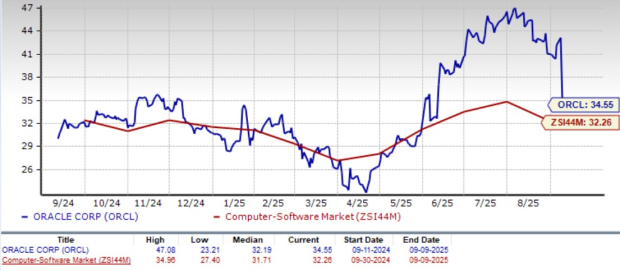

Shares of Oracle have surged 97% year to date, outperforming both the Zacks Computer and Technology sector’s return of 16.8% and the Zacks Computer - Software industry’s rise of 15.4%.

From a valuation standpoint, ORCL appears overvalued, trading at a forward 12-month Price/Earnings ratio of 34.55x, which is higher than the industry average of 32.26x. Oracle carries a Value Score of F.

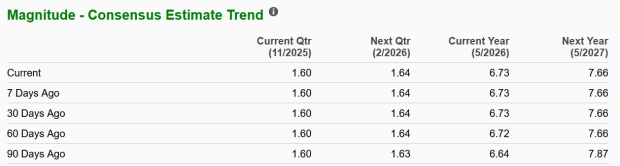

The Zacks Consensus Estimate for ORCL’s fiscal 2026 revenues is pegged at $66.60 billion, indicating 16.02% year-over-year growth. The consensus mark for ORCL’s fiscal 2026 earnings is pegged at $6.73 per share, holding steady over the past 30 days and up by a penny in the last 60 days. The earnings figure suggests 11.61% growth over the figure reported in fiscal 2025.

ORCL stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 8 min | |

| 14 min | |

| 22 min |

Stock Market Today: Nasdaq Gains As Trump Addresses Tariff Ruling; Alphabet Heads Higher (Live Coverage)

AMZN

Investor's Business Daily

|

| 1 hour |

Amazon Stock Climbs After Trump Tariff Ruling. E-Commerce Stocks Jump.

AMZN

Investor's Business Daily

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours |

Stock Market Today: Dow Turns Higher As Supreme Court Nixes Trump Tariffs (Live Coverage)

AMZN

Investor's Business Daily

|

| 2 hours |

Amazon Stock Climbs After Trump Tariff Ruling. These E-Commerce Stocks Are Up Too.

AMZN

Investor's Business Daily

|

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite