|

|

|

|

|||||

|

|

|

Alibaba's BABA aggressive push into AI has reached an inflection point in September 2025, with the Chinese tech giant unveiling groundbreaking models that challenge Western dominance in generative AI. The company's latest releases, including the ultra-efficient Qwen3-Next architecture and the trillion-parameter Qwen3-Max preview, signal a transformative shift in its cloud and AI strategy.

For growth investors evaluating whether to initiate or expand positions, the confluence of technological breakthroughs, massive infrastructure investments, and lingering geopolitical uncertainties creates a complex risk-reward equation that warrants careful consideration.

The Zacks Consensus Estimate for fiscal 2026 revenues is pegged at $144.18 billion, indicating 4.38% year-over-year growth. With the Zacks Consensus Estimate for fiscal 2026 earnings indicating decline of 10.21% year-over-year to $8.09 per share, the market appears increasingly cautious about Alibaba's growth trajectory.

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

The Sept. 12 announcement of Qwen3-Next represents more than incremental progress; it demonstrates Alibaba's ability to innovate at the architectural level. The 80-billion-parameter model that activates only 3 billion parameters during inference achieves performance comparable to much larger models while using less than 10% of traditional training costs. This efficiency breakthrough, combined with the model's native support for 256,000-token context windows extendable to one million tokens, positions Alibaba competitively against established players in enterprise AI applications where cost-effectiveness and scalability matter most.

The company's Qwen3-ASR-Flash automatic speech recognition model further illustrates its multimodal capabilities, accurately transcribing across 11 major languages and multiple Chinese dialects even in challenging acoustic environments. This breadth of linguistic coverage gives Alibaba distinct advantages in Asian markets where Western models often underperform. The preview of Qwen3-Max, exceeding one trillion parameters and ranking sixth globally in text arena benchmarks, establishes Alibaba as a legitimate contender in the large language model race previously dominated by OpenAI and Alphabet GOOGL-owned Google.

Alibaba's commitment of $52 billion over three years for AI infrastructure development reflects recognition that model innovation alone cannot drive sustainable competitive advantage. The strategic shift to self-developed AI training chips, partially replacing Nvidia hardware, addresses both cost optimization and supply chain resilience amid ongoing U.S. export restrictions. This semiconductor independence initiative, while requiring substantial upfront investment, could prove prescient as geopolitical tensions continue reshaping global technology supply chains.

The September 2025 raising of $3.2 billion in convertible notes specifically for cloud expansion demonstrates management's conviction in AI-driven growth opportunities. The integration of Qwen AI into flagship products like PolarDB database and AnalyticDB data warehouse creates synergies across Alibaba's ecosystem while providing differentiated offerings for enterprise customers. With more than 20 million downloads of open-source Qwen models on Hugging Face, the company has successfully cultivated developer mindshare crucial for platform adoption.

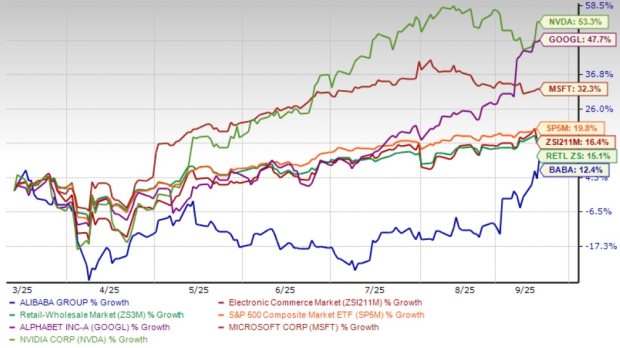

Despite these technological achievements, Alibaba's stock performance remains subdued relative to AI-focused peers and the Zacks Retail-Wholesale sector. While Nvidia NVDA has surged more than 53.3% in the past six months and Microsoft MSFT gained 32.3% on AI momentum, Alibaba shares have appreciated only 12.4%, trading at approximately 11 times forward earnings compared to the 25-30 times multiple commanded by U.S. tech giants.

Despite appearing cheap on traditional metrics, Alibaba represents a classic value trap where superficial attractiveness masks deeper structural problems. Alibaba continues to trade at a premium valuation with a Value Score of C. The market has priced in the upside of AI, while underestimating the execution risks and capital intensity required for meaningful transformation.

The stock's forward 12-month Price/Sales ratio of 2.45X compared to the Zacks Internet-Commerce industry average of 2.26X reflects persistent concerns about Chinese regulatory oversight, slowing domestic consumption, and potential technology decoupling scenarios.

The company's cloud division, where AI innovations primarily manifest, generated roughly $3.5 billion in quarterly revenues during fiscal first-quarter 2026, representing modest 6% year-over-year growth. This underwhelming expansion rate, despite AI tailwinds, suggests monetization challenges remain. Management's guidance implies acceleration in subsequent quarters as enterprise AI adoption scales, but execution risks persist given intense competition from domestic rivals like Baidu and ByteDance, both advancing their own large language models.

For growth investors, Alibaba presents a compelling yet nuanced opportunity. The company's AI capabilities have reached parity with global leaders in many dimensions while offering superior cost efficiency that could drive market share gains. The massive infrastructure investment program and architectural innovations position Alibaba to capitalize on Asia's AI adoption curve, particularly in sectors like e-commerce, logistics, and multilingual applications, where it maintains domain expertise.

However, geopolitical uncertainties, including potential further technology restrictions and cross-border data flows, could constrain international expansion. The premium valuation gap versus U.S. peers may persist until regulatory clarity improves and cloud revenue growth demonstrates sustained acceleration.

Given these dynamics, a hold recommendation appears prudent for existing shareholders, while new investors might benefit from waiting for either a more attractive entry point below current levels or clearer evidence of AI monetization momentum in upcoming quarterly results. The technological foundation is undeniably strong, but patient capital will likely be rewarded as the market awaits tangible proof that innovation translates into sustained financial outperformance. BABA stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 39 min | |

| 49 min | |

| 57 min |

SoftBank-Backed Wayve Raises $1.2 Billion From Microsoft, Nvidia, Automakers

MSFT

The Wall Street Journal

|

| 57 min |

SoftBank-Backed Wayve Raises $1.2 Billion From Microsoft, Nvidia, Automakers

NVDA

The Wall Street Journal

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite