|

|

|

|

|||||

|

|

|

Citigroup, Inc. C is in the midst of a sweeping transformation aimed at building a leaner, more efficient banking powerhouse. Pursuant to this, the company changed its operating model and the leadership structure. This resulted in a streamlined and straightforward management structure aligned with and supporting the bank's strategy of increased spans of control, and significantly reduced bureaucracy and unnecessary complexity.

In January 2024, C announced plans to cut 20,000 jobs or approximately 8% of its global staff by 2026. The bank had already made significant progress by reducing its headcount by more than 10,000 employees.

The company also continues to focus on streamlining processes and platforms and driving automation to reduce manual touchpoints. Citigroup is increasingly deploying artificial intelligence (AI) tools to support these efforts.

Citigroup’s aggressive cost-cutting and transformation initiatives may weigh on near-term profitability, but they position the bank for stronger, more sustainable returns beyond 2026. With an aggressive focus on cost-cutting, automation, and streamlined operations, the bank is positioning itself for more substantial returns in the coming years.

Management expects expenses of $53.4 billion for 2025, slightly lower than $53.9 billion in 2024. Revenues are anticipated to witness a CAGR of 4-5% by 2026. Also, the company expects to achieve $2-2.5 billion in annualized run rate savings by 2026.

Bank of America's BAC prudent expense management has supported its financials in the past. However, expenses have been rising over the past few years. Bank of America’s total non-interest expenses saw a four-year (ended 2024) CAGR of 4.9% because of continued investments in technology and people across businesses. The uptrend in costs continued in the first half of 2025. Given Bank of America’s continued investments in its franchise, overall expenses are expected to be elevated in the near term. Management expects expense growth to be flattish in the back half of 2025.

On the contrary, Wells Fargo's WFC prudent expense management initiatives support its financials. Since the third quarter of 2020, Wells Fargo has been actively engaging in cost-cutting measures, including the streamlining of its organizational structure, closure of branches, and reduction in headcount. Non-interest expenses witnessed a negative CAGR of 1.3% over the last four years (ended 2024), with the declining trend continuing in the first half of 2025. This was driven by the positive impacts of efficiency initiatives. Wells Fargo’s non-interest expenses for 2025 are expected to be $54.2 billion, whereas it reported $54.6 billion in 2024.

Shares of Citigroup have gained 44.3% year to date compared with the industry’s growth of 28.9%.

Price Performance

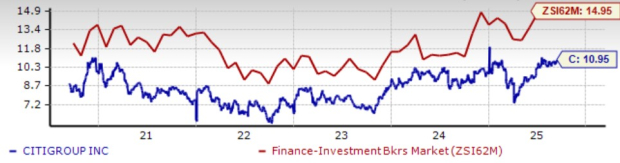

From a valuation standpoint, C trades at a forward price-to-earnings (P/E) ratio of 10.95X, below the industry’s average of 14.95X.

Price-to-Earnings F12M

The Zacks Consensus Estimate for C’s 2025 and 2026 earnings implies year-over-year rallies of 27.6% and 27.8%, respectively. The estimates for 2025 and 2026 have been revised upward over the past 30 days.

Estimates Revision Trend

Citigroup currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 39 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 9 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite