|

|

|

|

|||||

|

|

|

Falling interest rates are reshaping the outlook for major U.S. lenders, with investors looking closely at which banks stand to benefit the most. Bank of America BAC and Wells Fargo WFC, both highly sensitive to rate movements, are now under the spotlight as markets price in the next phase of monetary easing.

Though both move with the same macroeconomic tides, WFC now enjoys strategic freedom following the lifting of its asset cap in June 2025, whereas BAC is using its vast scale to deepen efficiency and broaden its growth initiatives. Let’s dig deeper and assess how rate cuts will shape the growth prospects of each bank to determine which one presents a better investment opportunity.

Bank of America, one of the most rate-sensitive banks in the country, is prioritizing organic, domestic growth through the expansion of its physical and digital presence. The company, recently, laid out an ambitious medium-term plan centered on sustainable growth, digital scale, cost discipline and capital efficiency.

Over the next three to five years, BAC aims to deliver more than 12% of earnings growth and a return on tangible common equity (ROTCE) between 16% and 18%, while maintaining a Common Equity Tier 1 ratio of 10.5%.

With the Federal Reserve starting the next rate cut cycle, Bank of America is poised to benefit from fixed-rate asset repricing, higher loan and deposit balances and a gradual fall in funding costs. As rates come down, it will boost lending activity. Also, easing regulatory capital requirements will help channel excess capital into loan growth, particularly within resilient commercial and consumer segments. Hence, the bank’s net interest income (NII) is projected to grow 5-7% in 2026, after similar growth this year.

Additionally, as part of a broader strategy to solidify customer relationships and tap into new markets, BAC plans to expand its financial center network and open more than 150 centers by 2027. This, along with the growing adoption of digital tools, will support NII growth and expand cross-sell opportunities.

Moreover, BAC’s investment banking (IB) business is well-positioned to expand as deal-making activities have regained momentum after the initial setback due to President Trump’s tariff policies. Many deals that were put on hold are resuming as there is more clarity about the direction of the economy, interest rates and tariff plans, with capital remaining available. Bank of America targets mid-single-digit CAGR in IB fees over the medium term.

Wells Fargo is moving to expand across multiple business lines now that the Fed has lifted the asset cap that limited its growth since 2018. The company’s expansion strategy is closely aligned with expectations for more rate cuts, emphasizing deposit growth, targeted loan expansion and product investment as funding costs trend downward.

The bank is positioning itself to benefit from a softer rate environment, which will likely drive increased lending activity, stabilize net interest margins (NIM) and help further market share gains across fee-generating businesses.

Wells Fargo has signaled that interest rate cuts will help stabilize funding costs, making deposit growth a central pillar of its balance sheet strategy. Lower rates typically spur loan demand, and freed from its asset cap, the bank aims to aggressively grow both consumer and corporate loan assets.

Management expects 2025 NII to be roughly stable year over year, as lower rates support a rebound in loan origination and reduce deposit pricing pressures. WFC plans to leverage its expanded balance sheet to grow fee-rich franchises (IB, trading, wealth management, payments). This diversification is essential in a rate-cutting cycle, when NIM and NII may face pressure.

Wells Fargo's approach in a declining rate environment is to prioritize organic growth, compete more aggressively for deposits and selectively increase lending while remaining cautious during periods of heightened economic uncertainty. Thus, the bank is expected to see improved profitability and margin resilience as monetary conditions ease. This will enable it to invest in expanded commercial and consumer franchises and enhance its competitive standing now that regulatory constraints are removed.

While 2025 started on a positive note, Trump’s tariff plans and geopolitical tension resulted in massive volatility, upending bullish investor sentiments. This year, shares of Bank of America and Wells Fargo have gained 18.2% and 20.4%, respectively.

In terms of investor sentiments, Wells Fargo clearly has the edge.

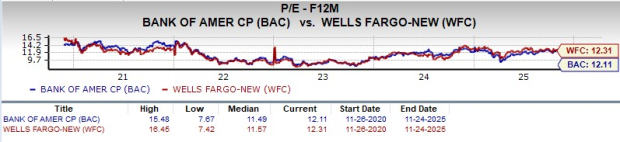

In terms of valuation, BAC is currently trading at a 12-month forward price-to-earnings (P/E) of 12.11X, while the WFC stock is currently trading at a 12-month forward P/E of 12.31X.

Further, both are trading at a discount compared with the industry average of 13.93X. So, Bank of America is inexpensive compared to WFC.

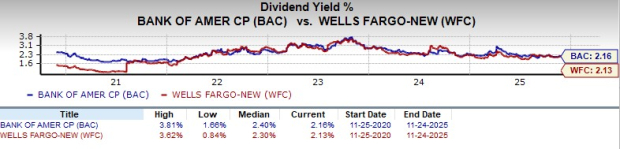

BAC’s dividend yield of 2.16% is more than Wells Fargo’s 2.13%. Nonetheless, both are higher than the S&P 500 average dividend yield of 1.52%.

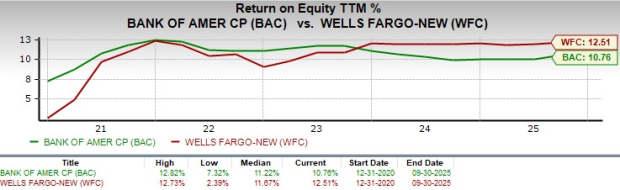

Bank of America’s return on equity (ROE) of 10.76% is below WFC’s 12.51%. Further, the industry’s ROE is 15.87%. This reflects that WFC is more efficiently using shareholder funds to generate profits.

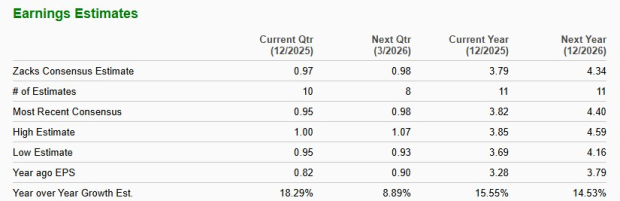

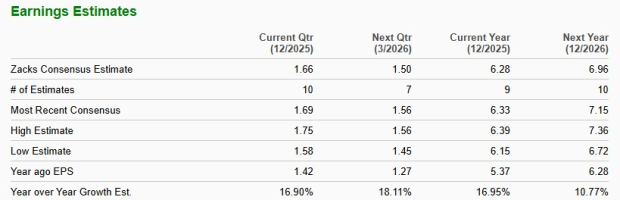

The Zacks Consensus Estimate for BAC’s 2025 and 2026 revenue implies year-over-year growth of 7.2% and 5.7%, respectively. The consensus estimate for earnings indicates a 15.6% and 14.5% rise for 2025 and 2026, respectively.

On the contrary, the Zacks Consensus Estimate for WFC’s 2025 and 2026 revenue implies year-over-year growth of just 2.1% and 5.4%, respectively. The consensus estimate for earnings indicates a 17% and 10.8% rise for 2025 and 2026, respectively.

Falling rates brighten the outlook for both banks, but Bank of America stands out. Its scale-driven efficiency, branch expansion and digital growth strategy position it to capture more lending activity as funding costs ease.

While Wells Fargo gains flexibility from the lifted asset cap, BAC’s clearer earnings trajectory, stronger NII growth prospects and medium-term ROTCE targets give it superior upside in a rate-cut cycle, making it the more compelling pick.

Currently, BAC and WFC carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 5 hours | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite