|

|

|

|

|||||

|

|

|

Opendoor Technologies Inc. OPEN is attempting its boldest pivot yet—moving from a single cash-offer product to a distributed platform that integrates agents directly into the selling journey. The strategy comes at a critical time. With persistently high mortgage rates suppressing buyer demand and clearance rates, the traditional iBuying model has faced sharp swings in volumes and margins. Opendoor’s new platform aims to stabilize performance by offering sellers a suite of options: an immediate cash offer, a traditional listing, or a hybrid “Cash Plus” model.

Early results are promising. In pilot markets, listing conversion rates were five times higher than the traditional flow, while customers reached final underwritten offers at double the prior rate. By sharing commissions with agents and reducing upfront capital exposure, Opendoor is unlocking high-margin, capital-light revenue streams. Importantly, the company reported its first-quarter adjusted EBITDA profitability in three years, highlighting the leverage potential of its evolving model.

Yet, risks remain. Management has guided to sequential revenue declines in the second half of 2025, with margins pressured by older, lower-yielding inventory. The full impact of Key Connections and Cash Plus is unlikely to materialize until 2026, creating a near-term gap between strategic progress and financial results.

Opendoor’s listing strategy offers a pathway to more durable growth and steadier earnings over the long run. While macro headwinds may weigh on results in the coming quarters, the company’s pivot could prove to be the stabilizer its volatile sales cycles have long needed.

Opendoor’s shift to a distributed listing model invites comparison with Zillow Z and Offerpad OPAD.

Zillow pivoted away from iBuying in 2021, focusing instead on Premier Agent leads and rentals. While Zillow sidestepped inventory risks, it remains tethered to housing demand cycles. Opendoor’s model now borrows from Zillow’s agent-centric approach, but enhances monetization through capital-light listing participation.

Offerpad stands as Opendoor’s most direct iBuying peer. The company continues to rely heavily on cash offers, exposing it to housing market swings. In contrast, Opendoor’s platform diversification could shield it from volatility in ways Offerpad has yet to achieve.

Shares of Opendoor have skyrocketed 1.573.5% in the past three months compared with the industry’s growth of just 8.5%.

OPEN’s 3-Month Share Price Performance

From a valuation standpoint, OPEN stock trades at a forward price-to-sales (P/S) multiple of 1.36, significantly below the industry’s average.

OPEN Stock’s Valuation

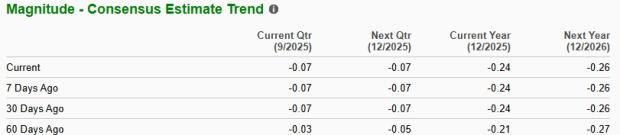

The Zacks Consensus Estimate for OPEN’s 2025 loss per share has widened to 24 cents from 21 cents over the past 60 days. Yet, the company is likely to report strong earnings, with projections indicating a narrower loss in 2025 from the year-ago loss of 37 cents per share.

OPEN stock currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-26 |

Mortgage and refinance interest rates today, Sunday, July 26, 2026: Rates up since last week

Z

Yahoo Personal Finance

|

| Jul-25 |

Mortgage and refinance interest rates today, Saturday, July 25, 2026: Highest rates this year

Z

Yahoo Personal Finance

|

| Jul-24 |

Mortgage and refinance interest rates today, Friday, July 24, 2026: Dropping below 6.5%

Z

Yahoo Personal Finance

|

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 |

Mortgage and refinance rates today, Wednesday, July 22, 2026: Interest creeps up

Z

Yahoo Personal Finance

|

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite