|

|

|

|

|||||

|

|

|

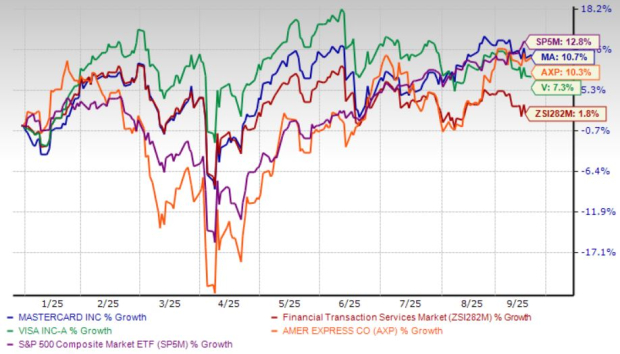

Shares of Mastercard Incorporated MA have delivered a 10.7% year-to-date gain, outperforming the broader industry and close peers Visa Inc. V and American Express Company AXP. The S&P 500 Index, however, edged ahead with a 12.8% rise over the same period. With this increase, Mastercard remains only about 3% below its 52-week high of $601.77, leaving room for debate on whether further upside lies ahead or if the stock has already priced in much of its strength.

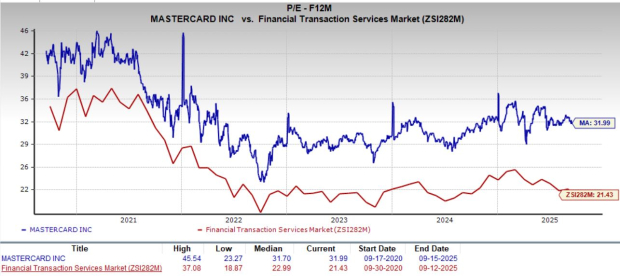

The payments giant’s valuation has become a sticking point for many investors. The stock currently trades at a forward earnings multiple of 31.99X, slightly above its five-year median of 31.70X and well above the industry average of 21.43X. It currently carries a Value Score of D. In comparison, Visa is valued at 26.52X forward earnings and American Express at 19.50X. This premium suggests that investors are already paying up for Mastercard’s strong fundamentals, though it also raises questions about how much further the stock can stretch without a pullback.

Despite valuation concerns, Mastercard’s growth story remains intact. The company has reinforced its competitive edge through deeper merchant engagement, an improved customer experience and expanding digital offerings. Tokenized transactions, which provide higher approval rates and reduced fraud, have gained traction and boosted trust across financial institutions and retailers. In the second quarter, its switched transactions grew 10% year over year to 43.5 billion, while cross-border volume surged 15%.

A major driver has been Mastercard’s Value-Added Services, which provide diversification beyond core payments. Revenues from this segment rose 17.7% in 2023, 16.8% in 2024 and an impressive 20% in the first half of 2025. The company relies on acquisitions and partnerships to strengthen cybersecurity and broaden its offerings.

Concerns over new technologies like stablecoins have not gone unnoticed by Mastercard. Rather than resisting, the company has embraced these shifts by introducing the Mastercard Multi-Token Network and Mastercard Crypto Credential, both designed to ensure security in digital asset transactions. Partnerships with Paxos, MetaMask and Crypto.com highlight its proactive approach. With regulatory frameworks like the GENIUS Act and MiCA providing clarity, Mastercard and Visa are racing to incorporate stablecoins while safeguarding their dominant networks.

Mastercard’s strong cash generation remains a major driver. The company generated $7 billion in operating cash flow in the first half of 2025, compared with $4.8 billion a year ago. This robust cash generation enabled $4.8 billion in share repurchases and $1.4 billion in dividend payments during the same period. The combination of buybacks, dividends and strategic investments signals management’s confidence in sustaining long-term growth.

Analysts remain upbeat about Mastercard’s trajectory. The Zacks Consensus Estimate for Mastercard’s EPS indicates growth of 11.8% in 2025 and 16.5% in 2026. Revenues are expected to rise 15.1% and 12.4%, respectively. The stock has seen one upward earnings estimate revision over the past week, against no movement in the opposite direction.

The company has also outperformed earnings expectations in each of the last four quarters, delivering an average earnings surprise of 3.8%.

Mastercard Incorporated price-consensus-eps-surprise-chart | Mastercard Incorporated Quote

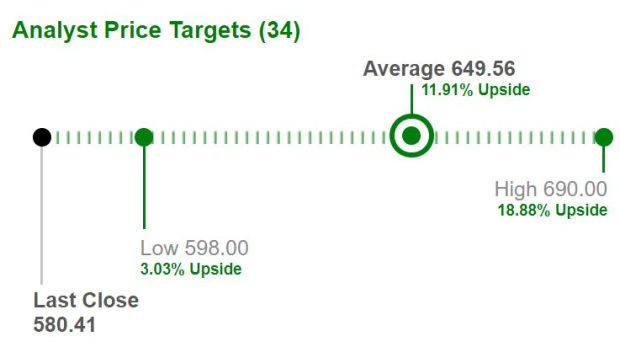

Currently, Mastercard trades below its average analyst price target of $649.56, pointing to an 11.9% potential upside from current levels. The high estimate of $690 and low of $598 highlight the range of opinions, but the overall direction suggests confidence in Mastercard’s ability to grow further.

Still, Mastercard faces hurdles, and regulatory and legal risks remain front and center. In June 2025, London’s Competition Appeal Tribunal ruled that both Mastercard and Visa’s multilateral interchange fees violated European competition law. The U.K. Payment Systems Regulator is also expected to introduce fee caps, which could dent revenue growth in the region.

In the United States, the Department of Justice earlier accused both Mastercard and Visa of using their dominance to overcharge merchants. The proposed Credit Card Competition Act could increase pricing pressure by forcing new routing options. While U.S. banks are lobbying against the bill, regulatory scrutiny is unlikely to fade. Mastercard also resolved a workplace pay bias case earlier in 2025, agreeing to implement internal audits.

Competition adds another layer of risk. The company is also fending off growing competition from agile fintechs and alternative payment rails. Big Tech companies and major retailers like Amazon and Walmart are exploring payment systems based on stablecoins, which can eventually bypass Mastercard’s rails.

Overall, Mastercard’s fundamentals remain compelling, supported by strong transaction growth, expanding Value-Added Services and steady cash generation that supports shareholder returns. Its proactive approach to digital assets and partnerships provides a forward-looking edge, while analyst estimates point to healthy earnings and revenue growth through 2026.

However, the premium valuation, ongoing regulatory challenges and mounting competition from fintechs and alternative payment rails remain key headwinds. As such, Mastercard currently carries a Zacks Rank #3 (Hold), suggesting that investors may want to wait for a more attractive entry point before building or adding to positions.You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Why investors should be 'really excited' about this form of agentic AI trading

V

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite