|

|

|

|

|||||

|

|

|

Shares of First American Financial Corporation FAF are trading at a discount compared with the Zacks Insurance - Property and Casualty industry. Its forward price-to-earnings value of 11.6X is lower than the industry average of 27.65X. It has a Value Score of A.

Shares of other insurers like Heritage Insurance Holdings, Inc. HRTG, Cincinnati Financial Corporation CINF and CNA Financial Corporation CNA are also trading at lower multiples than the industry average.

Shares of First American have gained 7.8% in the year-to-date period, outperforming its industry growth of 7.5%, while underperforming the sector and the Zacks S&P 500 Composite’s rallies of 13.3% and 14.1%, respectively.

The insurer has a market capitalization of 6.9 billion. The average volume of shares traded in the last three months was 1.03 million.

The Zacks Consensus Estimate for 2025 revenues is pegged at $7.1 billion, implying a year-over-year improvement of 15.9%. The consensus estimate for FAF’s current-year earnings is pegged at $5.11 per share, suggesting a 16.1% rise from the year-ago reported figure. The consensus estimate for 2026 earnings per share and revenues indicates increases of 18.9% and 9.1%, respectively, from 2025 estimates. It has a Growth Score of B.

The Zacks Consensus Estimate for 2025 earnings per share has moved up 2.6% in the past two months, while the same for 2026 earnings has moved up 1.2%.

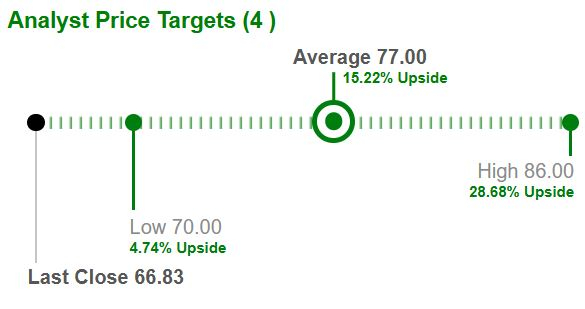

Based on short-term price targets offered by four analysts, the Zacks average price target is $77 per share. The average indicates a 15.2% upside from the last closing price.

Return on equity (ROE) for the trailing 12 months was 10.4%, comparing favorably with the industry’s 7.7%. This reflects its efficiency in utilizing shareholders’ funds.

First American is drawing strength from organic drivers like rising home prices, steady refinancing activity and a sharper focus on its title business. Expanding title plant assets and upgrading technology to improve efficiency provide support. Acquisitions, stronger distribution ties and international reach boost growth.

Continuing its growth path, First American is placing emphasis on expanding its core title insurance and settlement services, which have been the dominant contributor to its revenues. Its strength is reinforced by proprietary data extraction, growing leadership in title information and disciplined underwriting practices. Along with durable distribution relationships and an expanding international presence, these organic drivers are expected to keep the title segment on a firm trajectory.

Alongside its core operations, First American is advancing strategic initiatives aimed at sharpening competitiveness and enhancing returns. Investments in digital platforms like Endpoint and selective redeployment of capital toward high-yield areas highlight this approach. The company has also been acquiring title agencies in targeted growth regions while using proprietary data extraction to broaden its title plant base, which now reaches most of the U.S. population.

Despite these strengths, First American is being challenged by slower home sales, as high mortgage rates and affordability issues keep buyers on the sidelines. Since purchase transactions contribute more than refinancing, this weakness is a key concern. Market swings in its investment portfolio add to the pressure,while regulatory demands make it harder to stay both competitive and consistent on service.

Following the strain from housing market pressures, First American also faces challenges on the leverage front. Its debt-to-capital ratio stands at 23.11, above the industry average of 16.11. More concerning is the times interest earned of 2.62, which is far below the industry benchmark of 17.02, implying limited room to cover interest costs. Continuous servicing of this debt is vital, as any disruption may weigh on its credit profile and financial stability.

First American underscores its focus on shareholder value through prudent capital management. Dividends have been raised six times over the past five years, translating into an annualized growth rate of 3.8%, with a current payout ratio of 43. In addition, the board has authorized a $300-million share repurchase program, reflecting its commitment to rewarding investors.

Overall, First American stands on solid ground with its core title business, strong data capabilities and ongoing strategic investments supporting growth. Its VGM Score of A instils confidence. However, housing market weakness and debt-related pressures may affect its otherwise steady performance.

Ongoing headwinds limit meaningful upside for FAF. It is therefore wise to adopt a wait-and-see approach on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite