|

|

|

|

|||||

|

|

|

The Oracle of Omaha has long drawn interest from investors in his savvy stock picks.

Amazon is best known for e-commerce, but its cloud and ad businesses are key drivers now.

Visa, already the king of credit cards, will benefit from the increased adoption of digital payments.

Few, if any, people or companies command the attention of Warren Buffett and Berkshire Hathaway when it comes to investing moves. Given their decades of sustained success, it's easy to see why this is the case.

In general, the average investor shouldn't take investing moves by a billionaire and a trillion-dollar corporation as the gospel because the goals and risk tolerance aren't always aligned. However, getting inspiration from Buffett and Berkshire has proven to be a good choice for many investors.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

If you have $1,000 available to invest, the following two Berkshire stocks are great choices for long-term investors.

Image source: The Motley Fool.

Amazon (NASDAQ: AMZN) isn't one of Berkshire's largest holdings (less than 1% of its portfolio), but it's one of the most thorough companies in its portfolio. Although Amazon became a household name because of its e-commerce business, it has grown into a full-blown conglomerate covering many different industries.

E-commerce continues to be Amazon's biggest moneymaker, accounting for close to 60% of its revenue in the second quarter, but its largest growth engine is undoubtedly its cloud platform, Amazon Web Services (AWS). AWS was only 18% of its Q2 revenue, but it's the bulk of its profits.

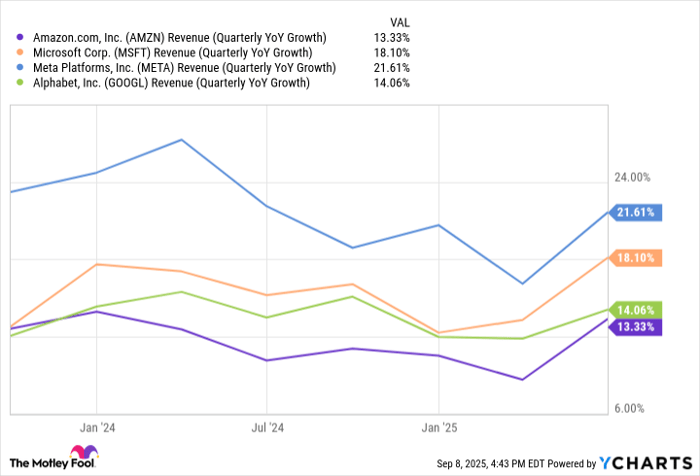

Amazon's revenue growth has been slower than that of other big tech competitors like Microsoft, Alphabet, and Meta Platforms in recent quarters, but its profits (looking at operating income) have been growing impressively. In Amazon's case, it helps to focus on its profit growth instead of revenue growth because its high-margin businesses like AWS and advertising are driving a lot of its earnings growth. These segments are also on the earlier ends of what they can grow to be.

AMZN Revenue (Quarterly YoY Growth) data by YCharts

AWS is still the leading cloud provider, but Microsoft's Azure and Alphabet's Google Cloud have been gaining ground. That said, the cloud computing industry is expected to grow to the point where AWS can organically benefit as the industry's largest player. I suspect it'll be the top player in the industry for quite a while.

As far as advertising, artificial intelligence (AI) and Amazon's growing web of businesses are unlocking new ways to monetize Amazon's technology. It has Amazon Prime, Twitch, Amazon Music, and, beginning this year, NBA broadcasting. Combined, these platforms give Amazon premium advertising opportunities across shopping, streaming, gaming, and live sports.

Amazon is a business that I feel comfortable holding on to for the long term because it's diversifying its business and solidifying itself as a major part of many different industries. That's a recipe for long-term success.

Visa (NYSE: V) is the largest payment processor in the world by a large margin, giving it a competitive moat that's built to last for quite some time. That's one of the characteristics Buffett is known for wanting before investing in any business.

Visa is accepted by over 150 million merchants worldwide, and in the 12 months leading up to March 31, it processed close to 316 billion transactions totaling around $16.1 trillion. Needless to say, Visa is an important part of the global financial ecosystem.

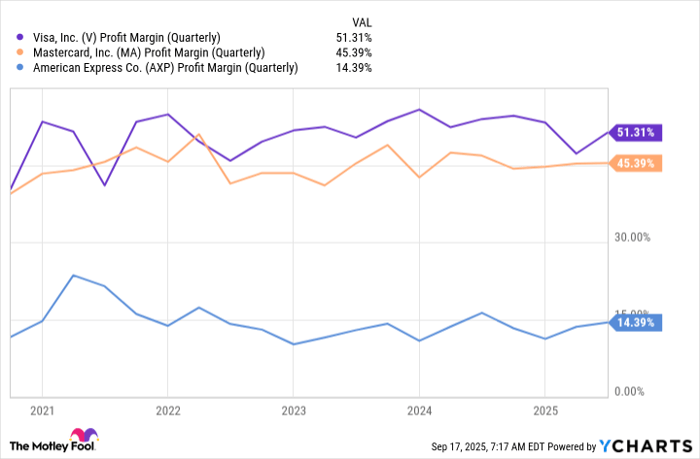

One of the best parts of Visa's business is that it's able to operate with extremely high margins because once the initial infrastructure is put in place, it can reap the benefit of increased transactions without needing to spend extra money or take on more overhead. Its profit margins are routinely the highest in the business and one of the highest you'll see from a company in most industries.

V Profit Margin (Quarterly) data by YCharts

Visa has routinely outpaced the S&P 500, especially over the past decade. It has averaged close to 17% annual returns in that span, compared to the S&P 500's 12.7% average. We can't predict if it will continue outpacing the S&P 500, but it has plenty of growth opportunities ahead of it that suggest it has a real chance at doing so.

On a broad level, Visa should be one of the biggest beneficiaries of the growth in digital payments. Many places in the world are becoming less cash-dependent and embracing card transactions (both physical and contactless). This bodes well for Visa, whose business model revolves around taking a percentage of each transaction that occurs on its network.

Given that it is the most widely held and accepted card worldwide, potential cardholders and merchants have an incentive to choose Visa. That's a large part of why I also feel comfortable holding on to Visa's stock for the long haul. It has solidified itself as a business that's too important to the global financial world to go away.

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $661,694!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,082,963!*

Now, it’s worth noting Stock Advisor’s total average return is 1,067% — a market-crushing outperformance compared to 189% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 15, 2025

Stefon Walters has positions in Microsoft and Visa. The Motley Fool has positions in and recommends Alphabet, Amazon, Berkshire Hathaway, Meta Platforms, Microsoft, and Visa. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 4 min | |

| 55 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 6 hours | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite