|

|

|

|

|||||

|

|

|

Root Inc.’s ROOT profitability is underpinned by its combined ratio, a key measure of underwriting performance. A combined ratio — defined as sum of loss ratio and expense ratio — below 100% signals underwriting profitability.

ROOT is heavily leaning on technology to improve pricing, one of the strategic pillars of growth. It is building on AI and machine learning to improve its pricing. Its business model relies heavily on acquiring and retaining low risk products while optimizing operational expenses through the use of technology. Also, ROOT focuses on geographic expansion and diversification of distribution channels. The insurer has successfully maintained its gross loss ratio below the long-term target of 60-65%, enabling selective rate cuts while sustaining the desired returns. Root’s strong business model has delivered some of the industry’s best loss ratios.

Improvements in the combined ratio directly translate to higher underwriting profits, reducing dependence on investment income or external capital to cover losses. With the Federal Reserve’s recent rate cut and anticipated further easing putting additional pressure on yields, sustained profitability depends on keeping the combined ratio below 100%.

This U.S.-based InsurTech, primarily focused on auto insurance, operates in a highly competitive, data-driven insurance landscape where underwriting efficiency is crucial for profitability. Encouragingly, ROOT has shown progress. Its net combined ratio improved to 94.2% in 2024, reflecting a 3,680-basis-point year-over-year gain, and strengthened further in the first half of 2025 with a significant 700-basis-point improvement. Root’s ability to consistently manage its combined ratio signals strong underwriting discipline, operational scalability and long-term profitability potential.

HCI Group HCI and Universal Insurance Holdings UVE have been continuously focusing on improving their combined ratios and strengthening underwriting profitability.

Both HCI Group and Universal Insurance ensure better pricing, stricter underwriting standards, geographic diversification (including expanding into less catastrophe-prone markets to reduce concentration risk), proper reinsurance, technological upgrades and digitalization (use of AI, predictive modeling, pricing analytics) and control operating costs.

These measures collectively help HCI Group and Universal Insurance deliver a lower combined ratio, thus reducing earnings volatility and supporting sustainable long-term growth.

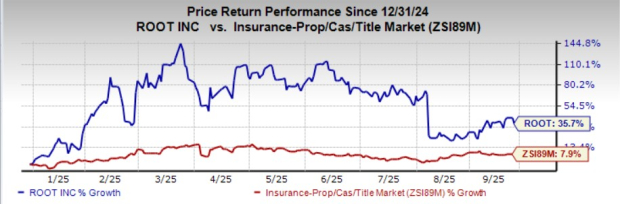

Shares of ROOT have gained 35.7% year to date, outperforming the industry.

ROOT trades at a price-to-book value ratio of 6.22, above the industry average of 1.54. It carries a Value Score of D.

The Zacks Consensus Estimate for ROOT’s full-year 2025 and 2026 EPS has moved 30.1% and 29.4% north, respectively, in the past 30 days.

The consensus estimates for ROOT’s 2025 and 2026 revenues and EPS indicate year-over-year increases.

ROOT stock currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| 6 hours | |

| 21 hours | |

| Aug-05 | |

| Aug-04 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-08 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite