|

|

|

|

|||||

|

|

|

For Progressive Corporation PGR, policy acquisition costs play a crucial role in determining its profitability. Policy acquisition costs (“PAC”) include costs incurred to acquire and underwrite new insurance policies, including agent commissions, marketing and advertising expenses, underwriting and policy issuance costs.

Progressive’s policy acquisition costs act as both a growth driver and a profitability tool. The leading auto insurer deploys data analytics, prudent pricing and telematics programs like Snapshot to target profitable customer segments and optimize acquisition spending. Costs incurred for policy acquisitions directly fuel top-line growth by expanding the total number of active insurance policies across its various business segments. Policies in force have been exhibiting steady growth over the years.

PAC also influences margins and combined ratios. Higher acquisition spending can pressure underwriting margins. Underwriting expense ratio, which includes the impact of PAC, has increased in 2024, up 240 basis points. Nonetheless, PGR tries to maintain an underwriting expense ratio below 20%.

Digitization has become an important tool in managing these expenses efficiently. Progressive continues to invest in generative AI tools with a vision to improve policy pricing, find new business opportunities, and create data-driven, personalized content variations to optimize messaging and enhance audience engagement.

Over the past years, policy acquisition costs have increased in line with higher business volumes, and their share of revenues has also risen, highlighting their growing importance in driving Progressive’s growth and sustaining underwriting profitability.

Policy acquisition costs are vital for both HCI Group HCI and Universal Insurance Holdings UVE, aiding both these insurers in expanding into new geographies while maintaining competitive pricing.

Managing these costs efficiently aids HCI Group and Universal Insurance in improving their expense ratio and thus underwriting profitability. Also, these efforts well poise both HCI Group and Universal Insurance to maintain solid margins across its personal and commercial insurance operations.

Shares of PGR have lost 8.7% year to date, underperforming the industry.

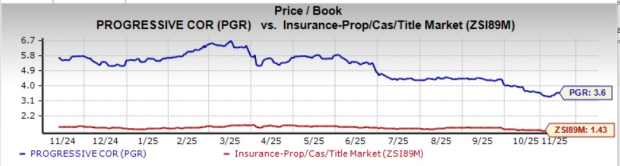

PGR trades at a price-to-book value ratio of 3.6, above the industry average of 1.43. But it carries a Value Score of B.

The Zacks Consensus Estimate for PGR’s fourth-quarter 2025 EPS has moved 6.5% north, while that for first-quarter 2026 has moved down

1.1% over the past 30 days. The same for full-year 2025 and 2026 has moved 4.2% and 0.1% down, respectively, in the same time frame.

The consensus estimates for PGR’s 2025 revenues and EPS indicate year-over-year increases. The consensus estimate for 2026 revenues indicates a year-over-year increase but the same for EPS indicates a year-over-year decline.

PGR stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-04 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite